[A version of this article was previously published on TKer.co.]

Stocks made new record highs, with the S&P 500 reaching a closing high of 5,029.73 on Thursday and an intraday high of 5,038.70 on Friday. For the week, the S&P shed 0.4%. The index is now up 4.9% year to date and up 39.9% from its October 12, 2022 closing low of 3,577.03.

The strength of the stock market seems in conflict with the plethora of news headlines on companies announcing layoffs. Here are a few from just the past week:

There’s no question that this is unfortunate. It can be particularly distressing to the individuals who are directly affected.

But if you’re thinking about what these headlines mean for the economy as a whole, you need a lot more context before you prematurely jump to conclusions.

For starters, it’s important to understand what’s typical for layoffs across the economy.

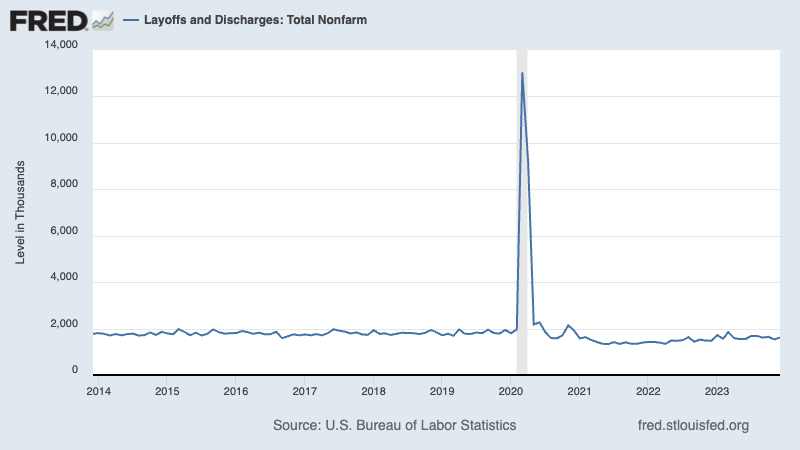

According to the most recent monthly Job Openings & Labor Turnover Survey from the BLS, employers laid off 1.6 million people in December.

That’s a large number. But as the chart below shows, monthly layoffs during much of the current economic recovery have bounced around between 1.3 million and 1.8 million. During the prepandemic economic expansion, this figure trended between 1.6 million and 2 million.

There’s a lot to be said about all this. Here are a few points:

To get to 1.6 million layoffs, a lot of companies have to make a lot of layoffs. For example, 1,600 companies announcing 1,000 layoffs gets you to 1.6 million. That is to say, the layoffs reported in the news may just reflect an ongoing phenomenon in the economy.

The 1.6 million layoffs represent just 1.0% of total employment. This layoff rate has ranged from 0.9% and 1.2% for most of the current recovery. During the prepandemic economic expansion, this figure trended between 1.1% and 1.4%.

Many people who get laid off return to work pretty quickly. This is confirmed by the fact that employers hired 5.9 million people in December (This includes people who were hired after quitting jobs). Furthermore, according to BLS data, the U.S. economy has experienced net job creation for 37 consecutive months through January.

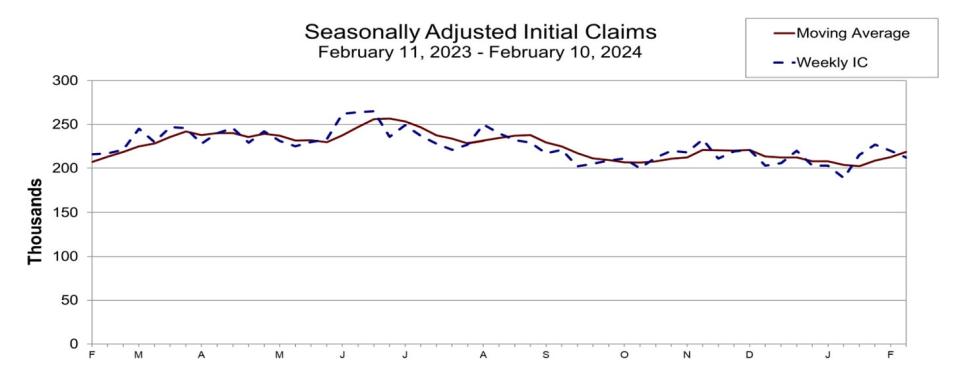

The national layoff data is a bit stale as it comes on a two month lag. However, the Labor Department’s weekly tally of initial claims for unemployment insurance benefits is very timely. During the week ending February 10, initial claims fell to 212,000, down from 220,000 the week prior. While this is above the September 2022 low of 182,000, it continues to trend at levels historically associated with economic growth.

As I noted in the Feb. 14 newsletter to paid subscribers, while mentions of layoffs in quarterly earnings transcripts have risen recently, they’re below last year’s levels. And last year’s flood of layoff headlines did not come with a significant move in the aggregate, hard labor market data.

To be clear, this is not to say there’s no chance this is a sign of trouble for the economy. Many economic metrics, including many labor market metrics, have cooled noticeably from very hot levels. There’s certainly a case to be made that we’re closer to the end of this economic expansion than we are at the beginning. (Read more about cooling economic metrics below in TKer’s weekly review of the macro crosscurrents.)

That said, it’s premature to conclude that the layoffs we’re currently reading about in the news is anything outside of what would be ordinary in an economic boom.

A quick note about the stock market

As TKer Stock Market Truth No. 10 reminds us, the stock market and the economy are not the same thing. (More here, here, and here.)

And so we shouldn’t assume that the metrics that define the U.S. economy will always move hand-in-hand with the stock market, which tends to be driven by earnings.

As BofA’s Savita Subramanian observed in November, there have been numerous years when GDP growth decelerated when S&P 500 earnings growth accelerated.

That is to say, it wouldn’t be crazy if we were to learn that stocks were climbing as the labor market was deteriorating. This topic may warrant a deeper discussion in a future newsletter. Stay tuned…

Goldman raises its target for the S&P 500

On Friday, Goldman Sachs’ David Kostin raised his year-end target for the S&P 500. From his note:

…Our target upgrade today reflects an improved earnings outlook. We continue to expect the S&P 500 forward P/E multiple will end the year at roughly 19.5x, a slight contraction from today’s 20x multiple.We raise our top-down S&P 500 EPS forecasts to $241 in 2024 and $256 in 2025, from $237 and $250 previously. … Earnings growth this year will be driven by a combination of 6% sales growth and 39 bp of net profit margin expansion to 11.5%. In 2025, we expect sales will grow by 4% and margins will expand by 24 bp to 11.7%…Our earnings revisions reflect upgraded outlooks for US economic growth and mega-cap profit margins… Our economists’ recently upgraded their 4Q/4Q 2024 real US GDP growth forecast to 2.4%, driven by sustained strength in consumer spending and residential investment. Our earnings model also takes into consideration variables such as world GDP growth, inflation, interest rates, oil prices, and the US dollar. We expect strong world GDP growth and a slightly weaker dollar will support EPS, while lower rates and lower oil prices will be a slight drag…

This is Kostin’s second revision from his initial target.

RBC, UBS, and CFRA are among firms who’ve already raised their targets.

Don’t be surprised to see more of these revisions as the S&P 500’s performance, so far, has exceeded many strategists’ expectations.

Reviewing the macro crosscurrents

There were a few notable data points and macroeconomic developments from last week to consider:

Consumer spending cools. Retail sales decreased 0.8% in January to $700.3 billion.

Categories driving weakness included building materials, cars and parts, gas stations, health and personal care, and online retailing. Furniture, restaurants and bars, grocery, and department stores saw gains.

It’s more evidence that the economy has gone from very hot to pretty good.

“The retail sales report this month supports our view that the economy is strong but cooling,” Morgan Stanley’s Ellen Zenter said.

For more, read: Economic growth: Slowdown, recession, or something else?

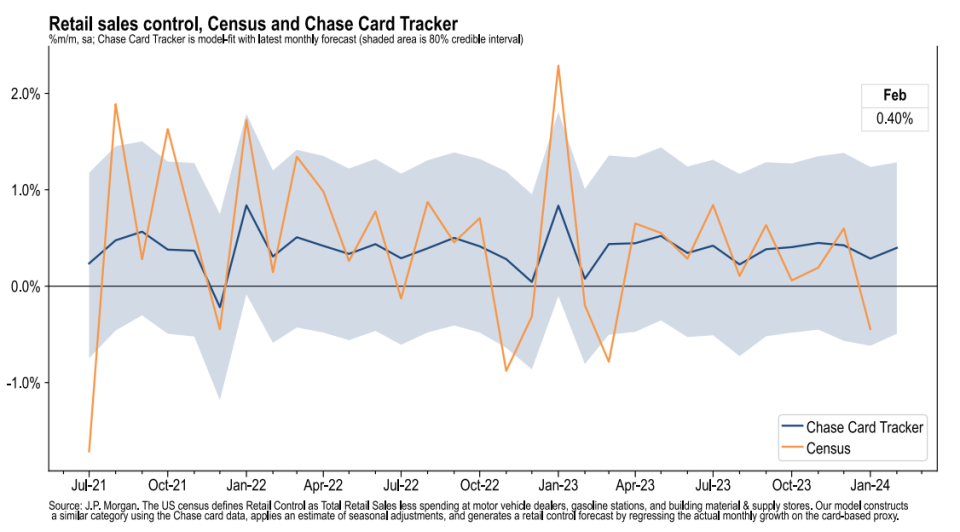

Card data suggests spending is holding up. From JPMorgan: “As of 08 Feb 2024, our Chase Consumer Card spending data (unadjusted) was 0.6% above the same day last year. Based on the Chase Consumer Card data through 08 Feb 2024, our estimate of the US Census February control measure of retail sales m/m is 0.40%.”

For more on consumer finances, read: People have money

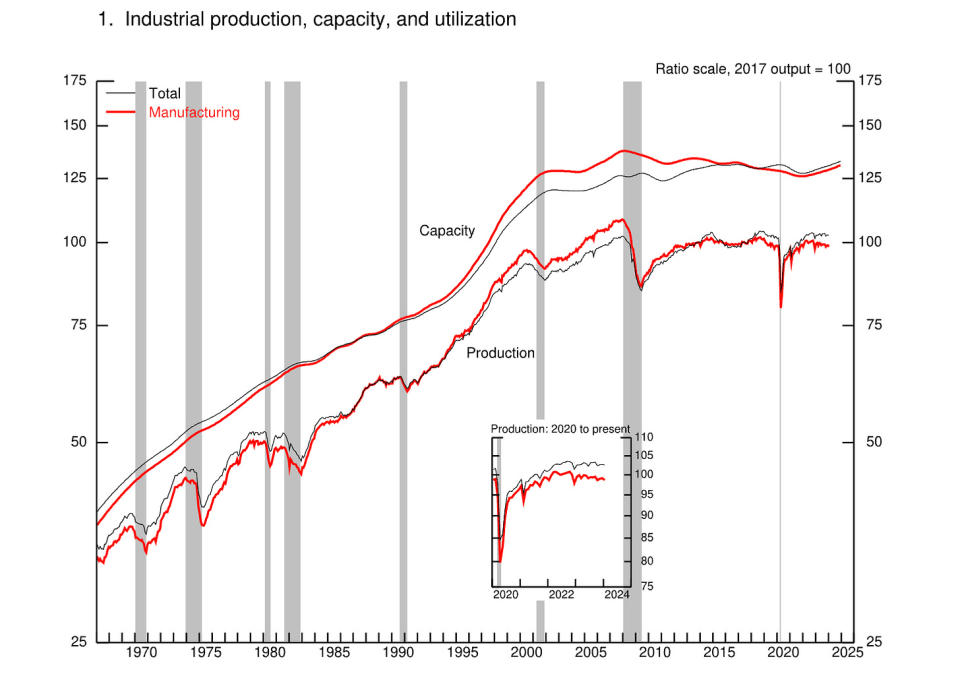

Industrial activity cools. Industrial production activity in December declined 0.1% from November levels, with manufacturing output falling 0.5%.

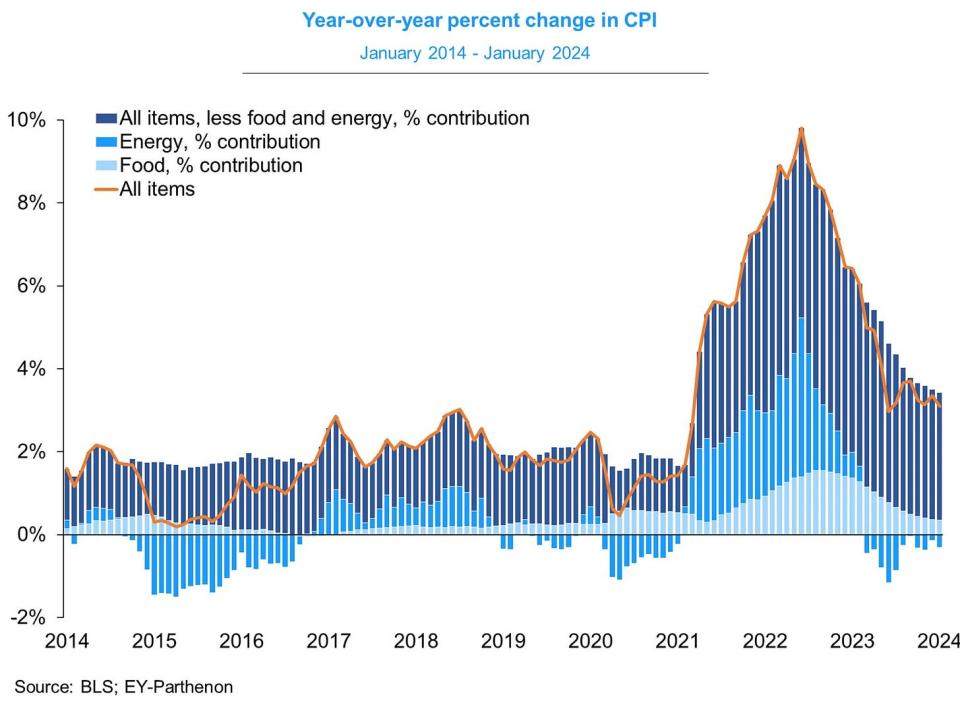

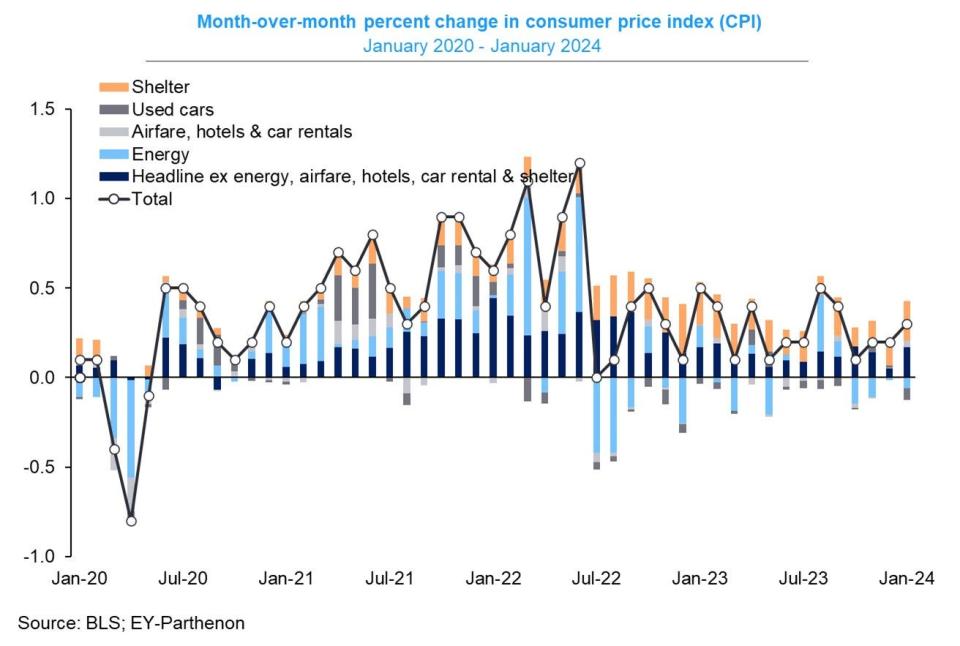

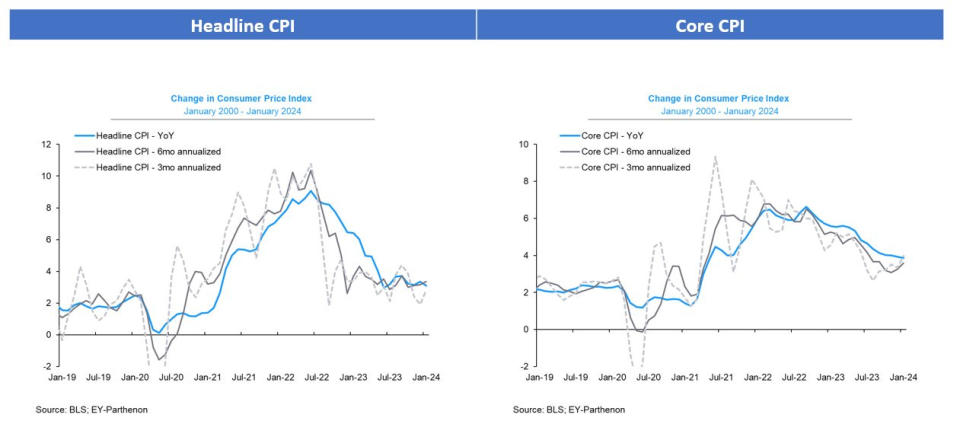

Inflation is cool-ish. The Consumer Price Index (CPI) in January was up 3.1% from a year ago. This was down from the 3.4% rate in December. Adjusted for food and energy prices, core CPI was up 3.9%, matching the prior month’s print, which was the lowest since May 2021.

On a month-over-month basis, CPI was up just 0.3%. Core CPI was up 0.4%.

If you annualize the three-month trend in the monthly figures — a reflection of the short-term trend in prices — CPI was rising at a 2.8% rate and core CPI was climbing at a 4% rate.

While many broad measures of inflation continue to hover above the Fed’s target rate of 2%, they are way down from peak levels in the summer of 2022.

For more, read: Inflation: Is the worst behind us?

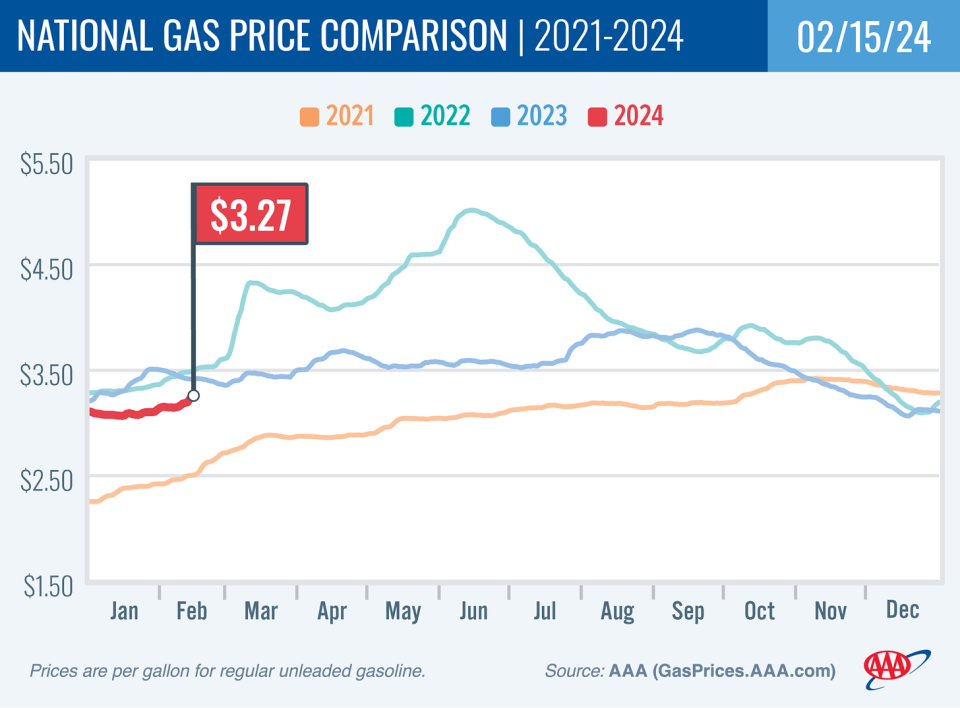

Gas prices rise. From AAA: “After months of barely budging more than a few cents, the national average for pump prices moved into the fast lane, surging 12 cents since last week to $3.27. A significant contributor is a shutdown at the large BP-Whiting refinery in Indiana, which has been offline for more than two weeks due to a power outage. The refinery processes 435,000 barrels of crude per day, and the shutdown has caused prices throughout the Midwest to climb, pushing the national average higher as well.”

For more on energy prices, read: The other side of the oil price story

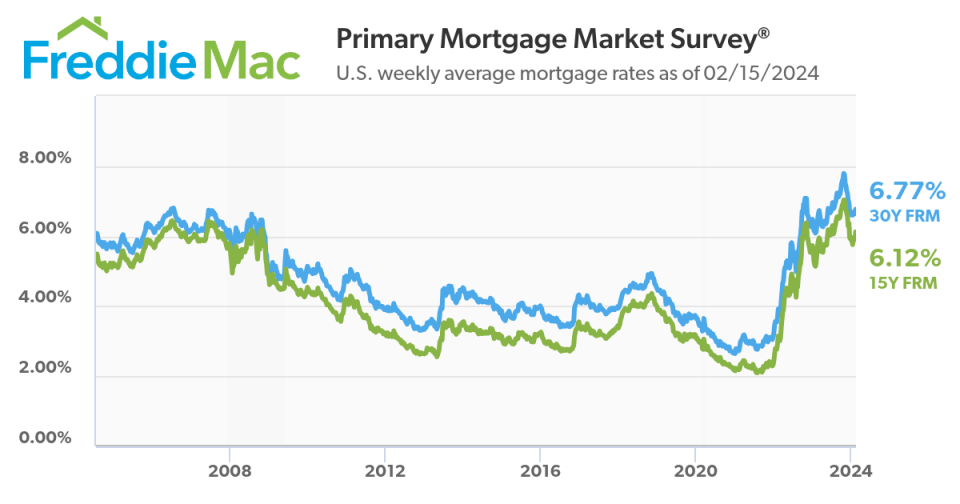

Mortgage rates tick up. According to Freddie Mac, the average 30-year fixed-rate mortgage rose to 6.77% from 6.64% the week prior. From Freddie Mac: “On the heels of consumer prices rising more than expected, mortgage rates increased this week. The economy has been performing well so far this year and rates may stay higher for longer, potentially slowing the spring homebuying season. According to Freddie Mac data, mortgage applications to buy a home so far in 2024 are down in more than half of all states compared to a year earlier.”

For more on mortgages and home prices, read: Why home prices and rents are creating all sorts of confusion about inflation

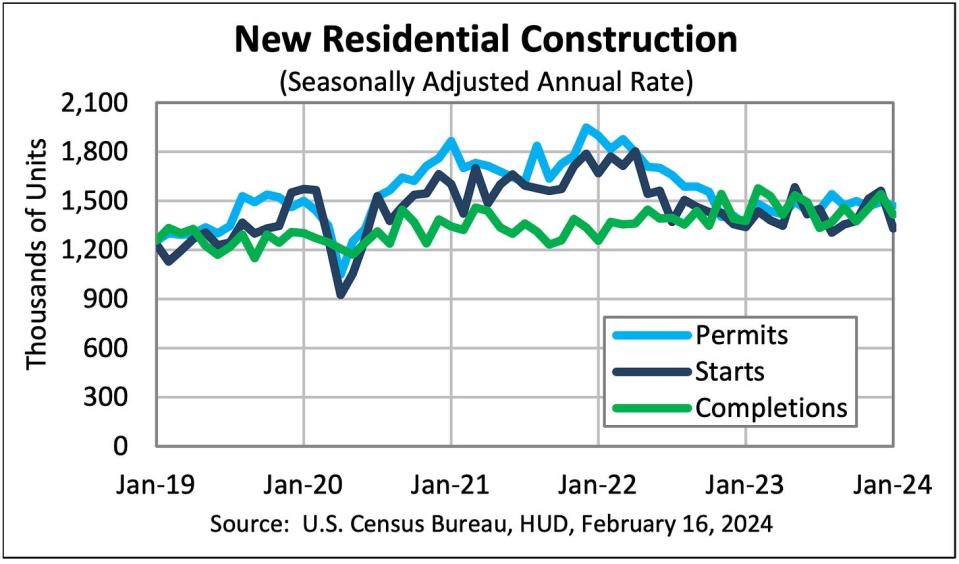

New home construction falls. Housing starts fell 14.8% in January to an annualized rate of 1.33 million units, according to the Census Bureau. Building permits fell 1.5% to an annualized rate of 1.47 million units.

For more on housing, read: The U.S. housing market has gone cold

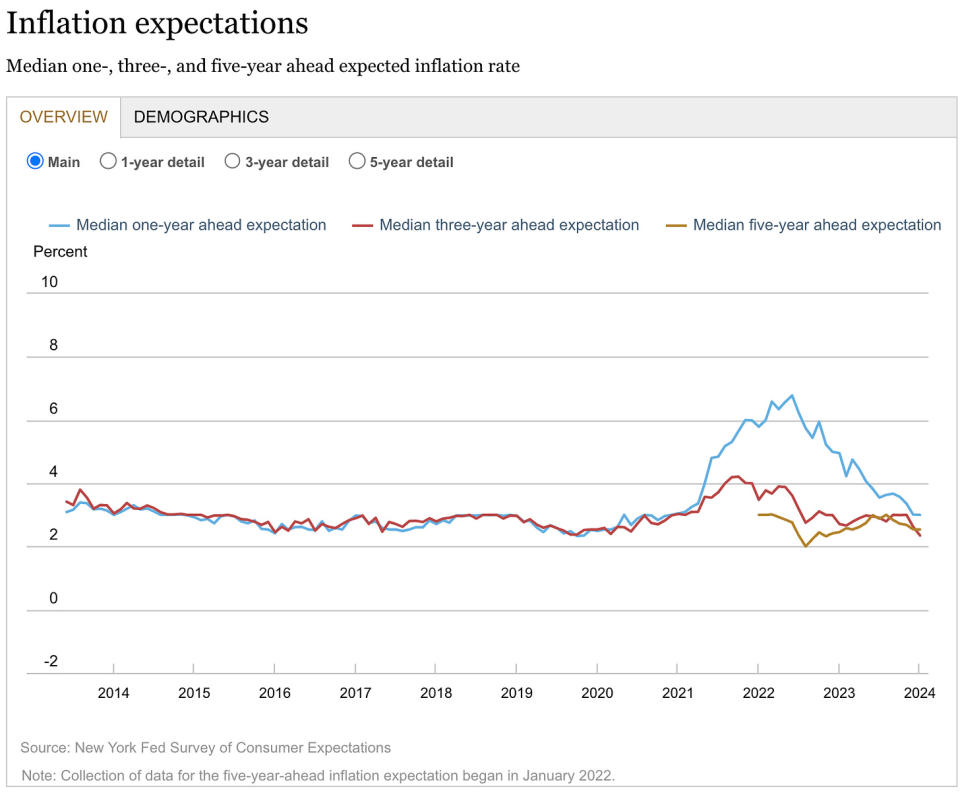

Inflation expectations improve. From the New York Fed’s January Survey of Consumer Expectations: “Median inflation expectations remained unchanged at the one- and five-year ahead horizons in January, at 3.0% and 2.5%, respectively. Median inflation expectations at the three-year ahead horizon declined to 2.4% from 2.6%.”

For more, read: The end of the inflation crisis

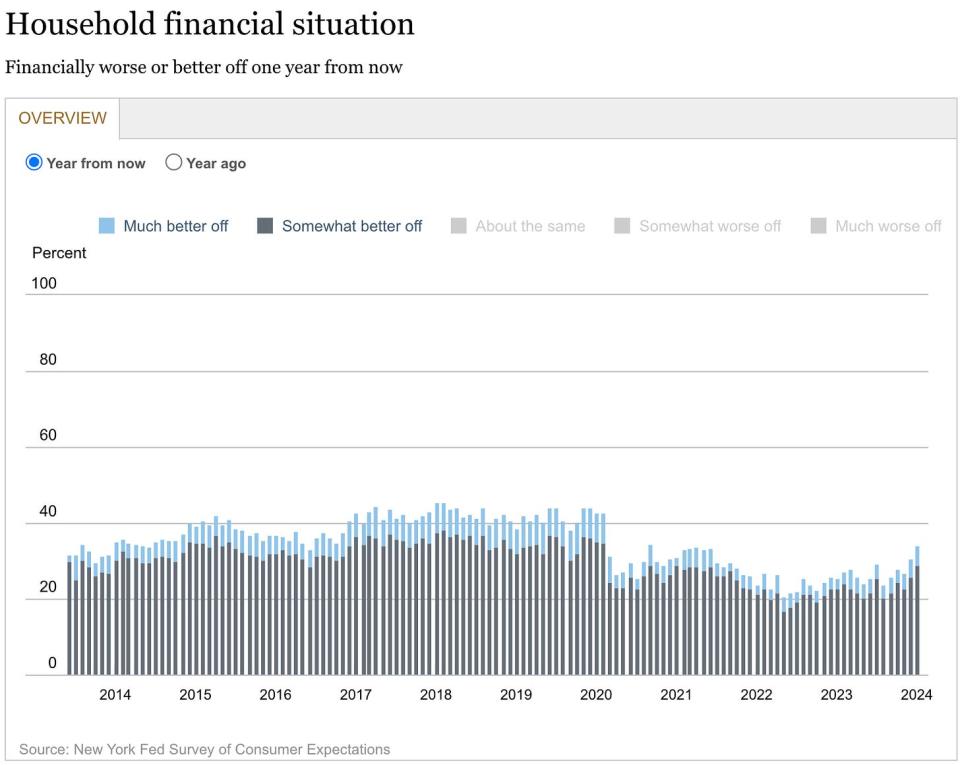

Consumers feel better about their financial situation. From the New York Fed’s January Survey of Consumer Expectations: “Perceptions about households’ current financial situations improved in January with more respondents reporting being better off than a year ago and fewer respondents reporting being worse off. Year-ahead expectations also improved with a smaller share of respondents expecting to be worse off and a larger share of respondents expecting to be better off a year from now. The percentage of respondents expecting to be financially the same or better off 12 months from now is 76.5%, its highest level since September 2021.”

For more on consumer finances, read: People have money

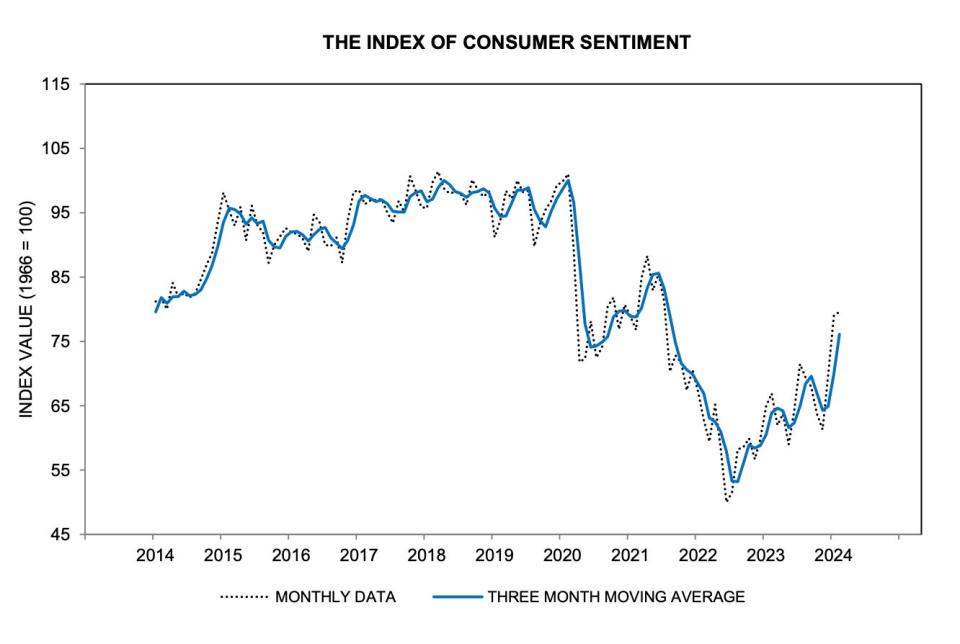

Consumer sentiment continues to improve. The University of Michigan’s consumer sentiment index inched higher in February, the third straight month of gains. From the survey: “Consumer sentiment was essentially unchanged from January, rising 0.6 index points this month and solidifying the large gains from the past two months. The fact that sentiment lost no ground this month suggests that consumers continue to feel more assured about the economy, confirming the considerable improvements in December and January across various aspects of the economy. Consumers continued to express confidence that the slowdown in inflation and strength in labor markets would continue.”

For more on improving sentiment, read: The economic vibes are healing

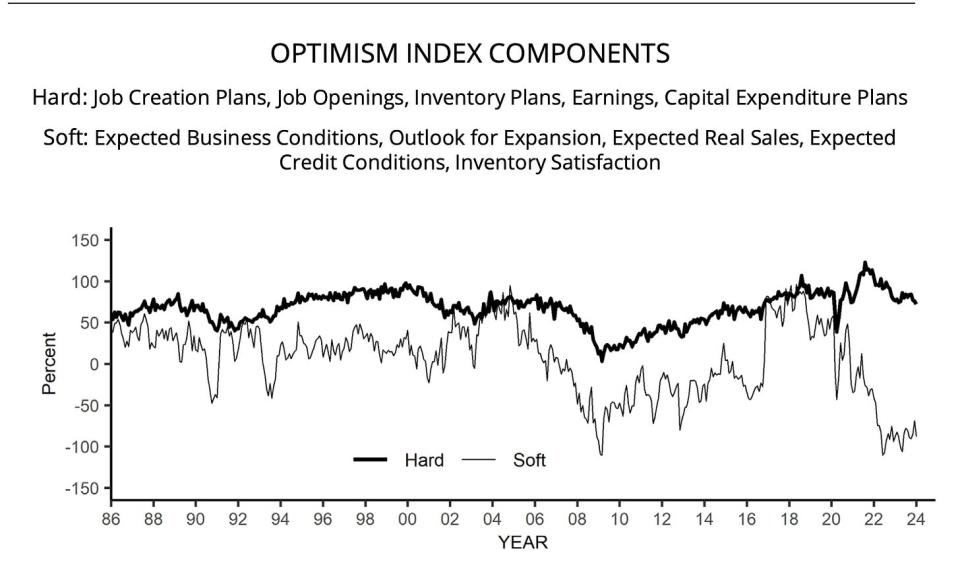

Small business optimism deteriorates. The NFIB’s Small Business Optimism Index ticked lower in January.

Importantly, the more tangible “hard” components of the index continue to hold up much better than the more sentiment-oriented “soft” components.

Keep in mind that during times of perceived stress, soft data tends to be more exaggerated than actual hard data.

For more on this, read: What businesses do > what businesses say and Sentiment: Finally a vibe-spansion?

Unemployment claims fall. Initial claims for unemployment benefits fell to 212,000 during the week ending February 10, down from 220,000 the week prior. While this is above the September 2022 low of 182,000, it continues to trend at levels historically associated with economic growth.

For more on the labor market, read: The hot but cooling labor market in 16 charts

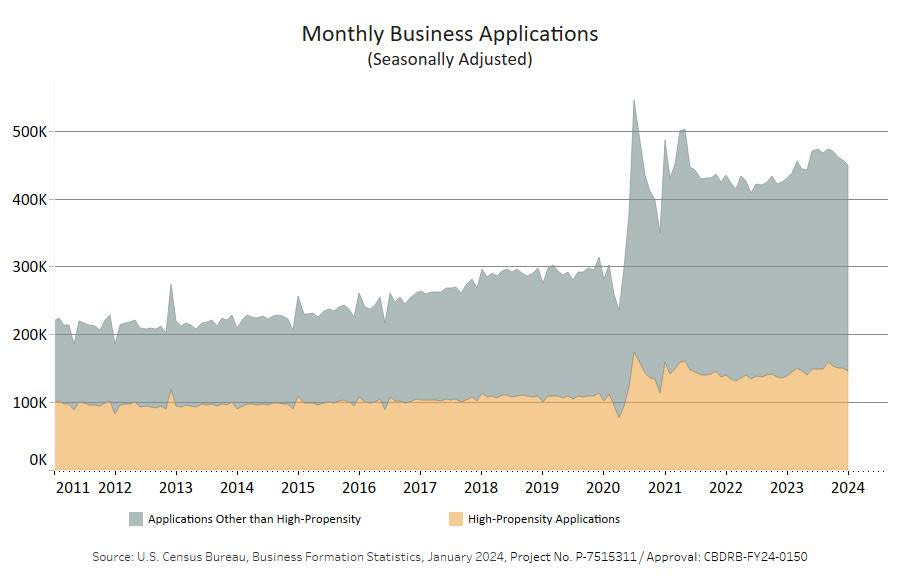

The entrepreneurial spirit is alive. Small business applications, while down slightly from the previous month, remain well above prepandemic levels. From the Census Bureau: “January 2024 Business Applications were 450,078, down 1.3% (seasonally adjusted) from December. Of those, 146,038 were High-Propensity Business Applications.“

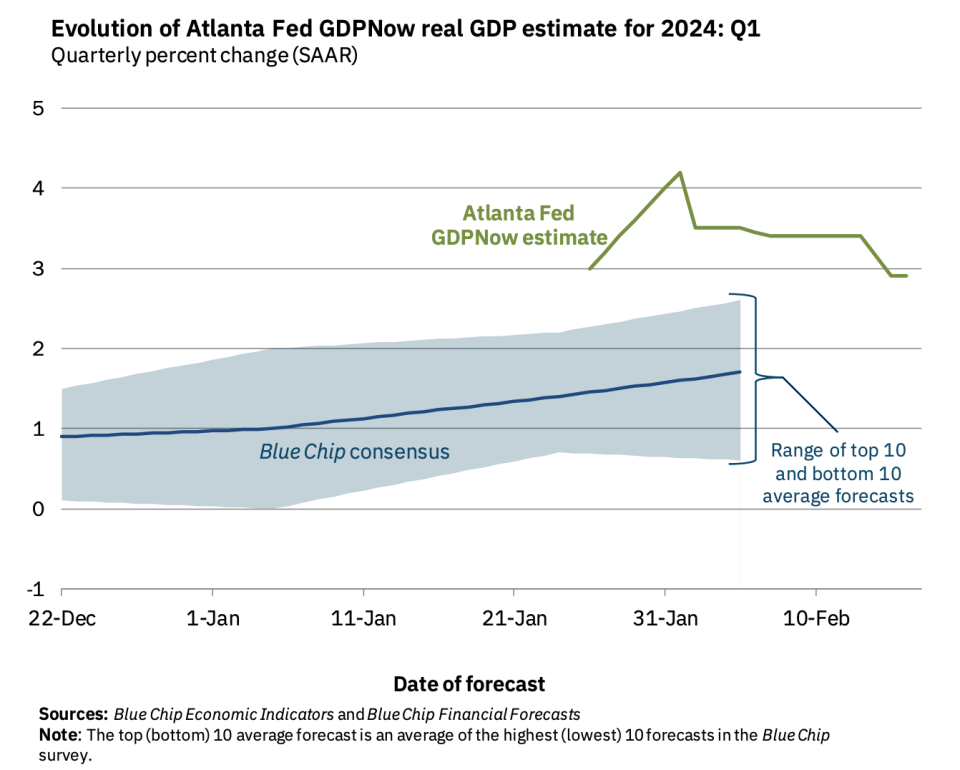

Near-term GDP growth estimates look good. The Atlanta Fed’s GDPNow model sees real GDP growth climbing at a 2.9% rate in Q1.

For more on economic growth, read: Economic growth: Slowdown, recession, or something else?

Putting it all together

We continue to get evidence that we are experiencing a bullish “Goldilocks” soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession.

This comes as the Federal Reserve continues to employ very tight monetary policy in its ongoing effort to get inflation under control. While it’s true that the Fed has taken a less hawkish tone in 2023 and 2024 than in 2022, and that most economists agree that the final interest rate hike of the cycle has either already happened, inflation still has to stay cool for a little while before the central bank is comfortable with price stability.

So we should expect the central bank to keep monetary policy tight, which means we should be prepared for relatively tight financial conditions (e.g., higher interest rates, tighter lending standards, and lower stock valuations) to linger. All this means monetary policy will be unfriendly to markets for the time being, and the risk the economy slips into a recession will be relatively elevated.

At the same time, we also know that stocks are discounting mechanisms — meaning that prices will have bottomed before the Fed signals a major dovish turn in monetary policy.

Also, it’s important to remember that while recession risks may be elevated, consumers are coming from a very strong financial position. Unemployed people are getting jobs, and those with jobs are getting raises.

Similarly, business finances are healthy as many corporations locked in low interest rates on their debt in recent years. Even as the threat of higher debt servicing costs looms, elevated profit margins give corporations room to absorb higher costs.

At this point, any downturn is unlikely to turn into economic calamity given that the financial health of consumers and businesses remains very strong.

And as always, long-term investors should remember that recessions and bear markets are just part of the deal when you enter the stock market with the aim of generating long-term returns. While markets have had a pretty rough couple of years, the long-run outlook for stocks remains positive.

[A version of this article was previously published on TKer.co.]

Credit: Source link