What’s the purpose of a business? For a long time, the textbook answer to that question has been purely “to make as much money as possible for its shareholders”. But business leaders – who often themselves get huge payouts from this model – are beginning to challenge this orthodoxy.

Or so it seems. The influential Business Roundtable association of top US business leaders, which includes CEOs of Apple, Boeing, Walmart and JP Morgan, made a landmark statement in August. They committed “to lead their companies for the benefit of all stakeholders – customers, employees, suppliers, communities and shareholders”. Maximising profits, they said, would no longer be their primary goal.

For many, it was seen as an historic moment for business. Markets, however, greeted the news with a yawn. Both the Dow Jones and the S&P500 in the US increased marginally on the day of the announcement.

Perhaps they recognised that there is unlikely to be a tectonic shift in the way that businesses behave. Certainly, it’s not the first time that businesses have changed their minds on this issue. The history of what – and who – businesses serve reveals that this is an age-old debate, which has raged since the dawn of modern day capitalism. Often, the real focus of the debate has been on how best to serve the bottom line.

Today, CEOs would be foolish to ignore issues like rising inequality, populism and a backlash against elites that would be bad news for their profits. As the Business Roundtable stated in its press release:

If companies fail to recognise that the success of our system is dependent on inclusive long-term growth, many will raise legitimate questions about the role of large employers in our society.

So we should not see this redefinition of company purpose as altruistic. Far from it. Businesses and CEOs are simply reacting to the changes in their environment, as they should. A cynic could also see this simply as a move to stave off regulations that will force them into making these kinds of changes. But, really, businesses would be better served by being more modest and focusing on what they do best – which is serving stakeholders as well as shareholders – instead of grandiose statements.

First, stakeholders were first

Back in January 1914, Henry Ford famously more than doubled the wages of his assembly workers from US$2.25 a day to US$5 a day. In later years this move took on mythic proportions, with claims that Ford wanted to pay his workers a fair wage so that they could afford to buy the very cars being churned out in his assembly line.

Kyle Harris / flickr, CC BY

The real rationale was more prosaic. The Ford motor factory was beset with chronic absenteeism and high worker turnover. A high wage, especially relative to wages available elsewhere, would reduce turnover, elicit greater effort, and help attract and retain better and more reliable workers. Economists refer to this as the efficiency wage hypothesis – that firms can increase their profits by paying above-market wages.

Henry Ford himself claimed that “There was no charity in any way involved … we wanted to pay these wages so that business would be on a lasting foundation … The payment of five dollars a day for an eight-hour day was one of the finest cost-cutting moves we ever made.”

Ford also wanted to cut prices to sell more cars, and reinvest the company’s US$60m capital surplus (the equivalent of US$1.4 billion today), instead of returning this to shareholders in the form of dividends. Shareholders baulked. Two brothers, John Dodge and Horace Dodge, who owned 10% of the company, sued Henry Ford in the Michigan State Supreme Court. The court ruled that Ford had to operate his company in the interest of shareholders and not of consumers and employees – profits should be the primary concern for the company.

Despite Ford being checked by the courts, the idea gained favour that corporations should be community minded, pay fair wages, take responsibility for the retirement of their workers via generous defined benefit plans, deliver value to customers and engage in charitable giving. The conglomerate Johnson & Johnson published its “Credo” in 1943, describing its responsibilities to multiple stakeholders. Shareholders were last in line and deserving only of a “fair” return.

When benefits accrued to a broad set of stakeholders, this also advanced the interests of the business and therefore the interests of shareholders. It was a popular strand of thinking up until the 1980s and was referred to as managerialism. Today, this kind of approach has a number of different monikers: “doing well by doing good”, adhering to a “double bottom line”, “profit with purpose” and creating “shared value”.

When greed became good

Most accounts in the popular press of the switch to the shareholder focus feature the arrival of economist Milton Friedman and the Chicago school of economics. An influential article by Milton Friedman for The New York Times magazine contended that “the social responsibility of business is to increase its profits”. It was this, apparently, that swayed academic, business, political and eventually public opinion to see the folly of managerialism.

The key ingredient of Friedman’s critique was that corporate executives are employees and must act in the interest of the ultimate owners, the shareholders, while conforming to existing laws and ethical norms. To the extent such executives identify with a social cause they should do so on their own time, using their own resources. Doing otherwise was equivalent to taxing the company, a task better left to civil servants and politicians who are selected by and accountable to the public at large.

Similarly, Friedman argued that socially conscious shareholders whose objectives divert from narrow profit maximising, should pursue these objectives in the private realm. They are free to devote their shareholder dividends to charitable causes as they see fit.

A confluence of events made this the intellectual foundation for the shareholder revolution in the 1980s. By the 1970s, US companies had become fat, bloated, overly diversified and unprofitable. Managers and CEOs lacked accountability. Some had developed a messianic complex using their companies for empire building.

US companies that had been hitherto unchallenged since World War II faced rising competition from European and Japanese rivals, who had started to peck away at their monopolistic and oligopolistic positions, eroding their profit potential. Oil price shocks triggered a period of stagflation, recession and pessimism.

By the 1980s, these US companies came increasingly under threat from corporate raiders and buyout funds, who identified inefficiencies, acquired controlling stakes, ruthlessly cut costs, stripped assets and aligned payment of executives to stock market performance.

Friedman’s thesis also found a ready political audience in US president Ronald Reagan and UK prime minister Margaret Thatcher. “Greed is good” became the new mantra. Then the collapse of the Soviet Union and a dawning realisation of the weakness of state-led development models led to the belief that “there is no alternative”. This was Thatcher’s slogan – that the path for societies to advance themselves was by embracing free markets, free trade and free movement of capital.

Wikimedia

This doctrine of unfettered capitalism (promoted under the banner of Friedmanism, Reaganomics, Thatcherism, take your pick), eventually morphed into a conviction in the benevolence of markets and deregulation, a deep distrust of government, and a near religious faith in the profit motive. Work by Friedman’s acolytes reshaped the theory and practice of corporate governance, reimagining companies as maximising the return on investment of shareholders.

These beliefs were then transmitted via business schools, economics departments, public policy institutes and think tanks to the next generation of business leaders. Via international financial institutions, including the World Bank, the International Monetary Fund and the World Trade Organisation, these ideas were also conveyed globally. In 1997, the Business Roundtable (yes, the very same) changed their mission statement and said: “The paramount duty of management and of boards of directors is to the corporations’ stockholders.”

Returning to stakeholders

Economist Adam Smith, the patron saint of the shareholder model of capitalism, would have protested such a grandiose interpretation. Smith emphasised not just self-interest but also the values of empathy, trust and high morals in commercial interactions. He lamented excessive risk taking in search of profits, especially in financial markets.

Smith recognised the power of the markets to efficiently allocate resources but also defended the role of the state in addressing market failures. He wondered at the power of markets to create value but was also deeply concerned about poverty, illiteracy and relative deprivation.

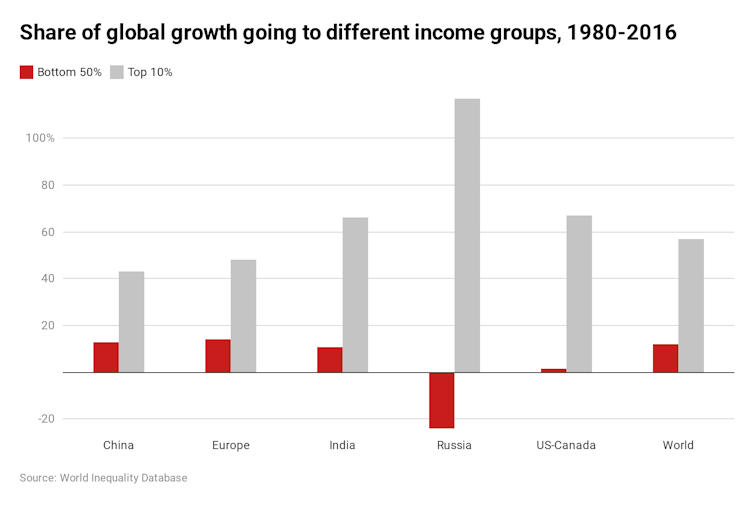

The shift towards the shareholder model of business in the 1980s coincided with a tremendous rise in income and wealth inequality, especially in Anglo-Saxon countries. Middle class wages stagnated, while most of the growth in income accrued to the richest 10% (see below). Wealth disparities rose dramatically, while inter-generational mobility in both relative and absolute terms declined sharply. Accompanying this was a rise in depression, suicides and opioid addiction, and a spike in mortality rates.

CC BY-ND

While the 2007-08 global financial crisis temporarily halted this increase in inequality, bailouts for banks and aggressive monetary policies resulting in a boom in asset prices, again exacerbated inequality. In the meantime, unemployment rates spiked across advanced countries, while mistaken notions of austerity in both the US and Europe meant that the recovery was painfully slow for the bottom 90% of the population.

The notion that the system was broken sunk deep into the consciousness of voters, who punished centrist parties as guardians of the status quo. Political entrepreneurs and populist parties took advantage of this deep cynicism by channelling voter disenchantment towards globalisation, immigration, elites and supranational institutions as a path to power.

With this shift in political winds, a siege mentality took hold among business leaders and “Davos decision makers”. Nine out of ten confessed to a rising anxiety about “populist and nativist agendas” and “public anger against elites”. The recent Business Roundtable pledge should be seen as a response to this fear and angst that the status quo seems increasingly untenable.

On the one hand, we could slip into a world of protectionism and nationalism held together by identity politics. On the other, we could see a surge in support for intrusive regulations, higher tax rates on corporations, estates and wealth, a crackdown on tax havens, the breakup of large corporations and even a return to state-owned capitalism. Ironically, the pledge if it mitigates such risks, will end up benefiting who else but the shareholders.

A modest approach

This brief history has us lurching back and forth between the ideas of shareholder versus stakeholder primacy that have waxed and waned over the decades. Are we doomed to pontificate on this endlessly?

As a way forward, I would advocate for a modest approach to end this interminable debate. A Hippocratic oath for corporations, based on seven principles:

1. Do no evil. Examples of evil include having your workers take bathroom breaks in bottles, selling browsing data of children, peddling opioids to patients, facilitating interference in national elections, creating fake bank accounts, cheating on emission tests, enabling money laundering for criminals, paying bribes, forming cartels and tolerating unsafe workplaces.

2. Pay taxes and adhere to laws and regulations. If laws are murky, implementation is discretionary and compliance is optional. See principle 1, above.

3. Avoid interfering in politics. Stop lobbying for preferential treatment and, if impossible, disclose all political donations.

4. Do not deny science. And do not run misinformation campaigns that undermine science in order to benefit your bottom line.

5. Focus on core competencies and embrace competition. Making billions of dollars does not necessarily mean you can fix education or be an effective president. Lobbying to reduce competition and boost profits is not a sign of confidence in the business’s core competency.

6. If invested in the stakeholder model, ensure that stakeholders are represented in your governance structures. Germany’s post-war model of Mitbestimmung or “co-determination” offers one example of how best to do this. This refers to the unique way that German companies give workers the right to participate in the way they are managed by electing their own representatives to company boards.

7. If concerned about inequality, start at home. Disclose wages, bonuses and pay ratios, by skill level and by gender in your organisation.

This approach can help restore faith in corporations, protect their brands and reputation, and avoid accusations of hypocrisy, while focusing their attention on what they truly do best – producing goods or services. To paraphrase the writer Anand Giridharadas: “Avoid virtue signalling and virtuous side projects; do your day jobs more honourably.”

And to quote Milton Friedman, business “should engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception or fraud”.

Credit: Source link