(Bloomberg) — Forget the artificial-intelligence frenzy — the most-exciting trade on Wall Street right now might just be betting on boring.

Most Read from Bloomberg

As winners of the AI boom like Nvidia Corp. power benchmark stock gauges to record after record, a less remarked-upon phenomenon has been unfolding at the heart of the US market: Investors are sinking vast sums into strategies whose performance hinges on enduring equity calm.

Known as short-volatility bets, they were a key factor in the stock plunge of early 2018 when they wiped out in epic fashion. Now they’re back in a different guise — and at a much, much bigger scale.

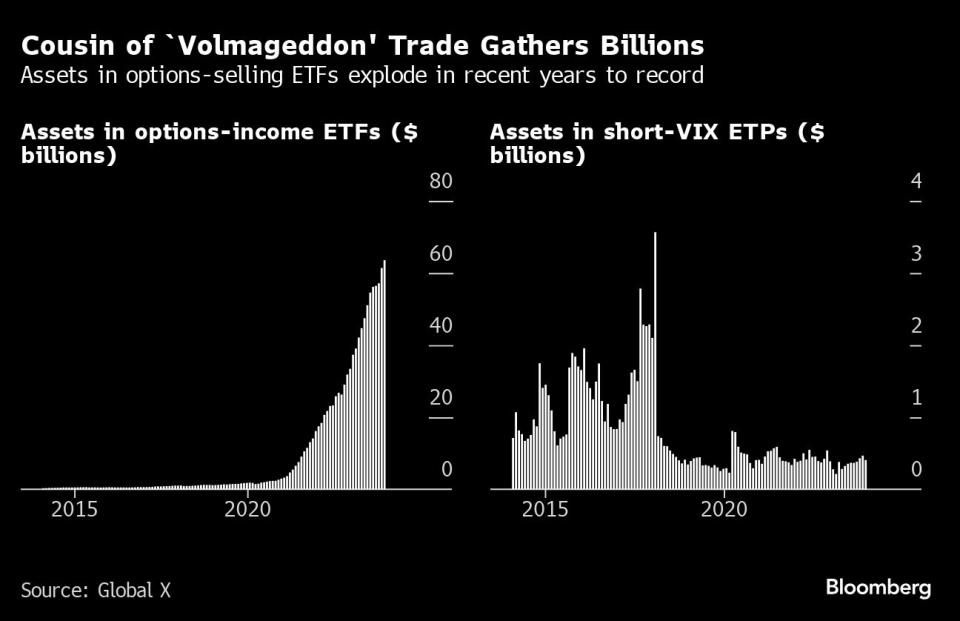

Their new form largely takes the shape of ETFs that sell options on stocks or indexes in order to juice returns. Assets in such products have almost quadrupled in two years to a record $64 billion, data compiled by Global X ETFs show. Their 2018 short-vol counterparts — a small group of funds making direct bets on expected volatility — had only about $2.1 billion before they imploded.

Shorting volatility is an investing approach that can mint reliable profits, provided the market stays tranquil. But with the trade sucking up assets and major event risks like the US presidential election on the horizon, some investors are starting to get nervous.

“The short-vol trade and its impact is the most consistent question we have gotten this year,” said Chris Murphy, co-head of derivatives strategy at Susquehanna International Group. “Clients want to know how much of an impact it’s having on markets so they can structure their trades better. But we have seen cycles in the past like 2018 and 2020 where the short volatility trade grows until a big shock blows it up.”

The good news for worrywarts is that the structural difference of the new funds changes the calculus — the income ETFs are generally using options on top of a long stock position, meaning that $64 billion isn’t all wagering against equity swings. There’s also likely a higher bar for broad contagion than in 2018, since the US market has doubled from six years ago.

The bad news is that the positions — alongside a stack of less visible short-vol trades by institutional players — are suspected of suppressing stock swings, which invites yet more bets for calm in a feedback loop that could one day reverse. The strategies are also part of an explosive wider growth in derivatives that is introducing new unpredictability to the market.

‘Somebody Has to Sell’

The trading volume of US equity options surged to a record last year, propelled by a boom in transactions involving contracts that have zero days until expiration, known as 0DTE. That has enlarged the volatility market, because each derivative amounts to a bet on future price activity.

“There basically is a natural increased demand for options because retail is speculating using the short-dated lottery-ticket type of options,” said Vineer Bhansali, founder of volatility hedge fund LongTail Alpha LLC. “Somebody has to sell those options.”

That’s where many income ETFs come in. Rather than deliberately betting on market serenity like their short-vol predecessors, the strategies take advantage of the derivative demand, selling calls or puts to earn extra cash on an underlying equity portfolio. It usually means capping a fund’s potential upside, but assuming stocks stay calm the contracts expire worthless and the ETF walks away with a profit.

Industry growth in recent years has been remarkable, and it has mostly been driven by ETFs. At the end of 2019, there was about $7 billion in the category of derivative income funds, according to data compiled by Morningstar Direct, three-quarters of which was in mutual funds. By the end of last year there was $75 billion, almost 83% of it in ETFs.

But while the money involved looks bigger, derivatives specialists and volatility fund managers are so far brushing off the risk of another “Volmageddon,” as the 2018 selloff came to be known.

John Marshall, Goldman Sachs Group Inc.’s head of derivatives research, said the strategy tends to come under pressure only when the market rises sharply. Most of the cash is in so-called buy-write ETFs, which take a long stock position and sell call options for income. A big rally increases the chances those contracts will be in the money, obliging the seller to deliver the underlying security below the current trading price.

“It’s generally a strategy that is not under pressure when the market sells off,” Marshall said. “It’s less of a worry for a volatility spike.”

Before the 2018 blowup, Bhansali at LongTail correctly foresaw the threat from the growing short-vol trade. He reckons there’s little danger of a repeat because this boom is powered by canny traders simply meeting retail-investor demand for options, rather than making leveraged bets on volatility falling.

In other words, the short-vol exposure itself is not a destabilizing force, even if such bets are vulnerable to turmoil themselves.

“Yes, there’s potential of instability if there’s a big market move for sure,” Bhansali said. But “somebody selling those options doesn’t necessarily mean that there’s a massive unhedged short base,” he said.

Nonetheless, quantifying any potential risk is difficult because even knowing the exact size of the short-vol trade is a challenge. Strategies can take on various shapes beyond the relatively simple income funds, and many transactions occur on Wall Street trading desks where information is not available to the public.

To many, the income ETF boom is a tell-tale sign of something bigger taking place below the surface.

“When you’re seeing something going on publicly, there’s probably five to 10 times that going on privately that you don’t see directly,” said Steve Richey, a portfolio manager at QVR Advisors, a volatility hedge fund.

Dispersion Doubts

Those unseen bets include a significant chunk of quantitative investment strategies — structured products sold by banks that mimic quant trades.

According to PremiaLab, which tracks QIS offerings across 18 banks, equity short-vol trades returned 8.9% in the US last year and wound up accounting for roughly 28% of new strategies added to the platform over the past 12 months. Their notional value is unknown, but consultancy Albourne Partners estimated last year that QIS trades overall command about $370 billion.

Hedge funds gaming relative volatility are also feeding the boom. One of the most notorious short-vol bets is an exotic options strategy known as the dispersion trade. Employing various complex options overlays, it amounts to being long volatility in a basket of stocks while wagering against the swings of an index like the S&P 500. To work, it needs the broader market to stay subdued, or at least experience less turbulence than the individual shares.

With the S&P 500 steadily going up while stock returns diverged widely in recent years, the strategy has flourished. Once again it’s difficult to measure the size of the trade, but it’s popular enough that Cboe Global Markets plans to list a futures product tied to the Cboe S&P 500 Dispersion Index this year.

That rising popularity, combined with leverage and a lack of transparency, has prompted Kevin Muir of the MacroTourist blog to warn that a market selloff could upset the trade, forcing an unwinding of positions that could further exacerbate the rout.

“It worries me because the dispersion trade has all the hallmarks of a crisis-in-the-making,” Muir wrote. It’s “exactly the sort of sophisticated, highly levered trade where everyone assumes ‘those guys are math whizzes – we don’t need to worry about them blowing up because they are hedged,’” he said.

To get an idea of how much short-vol exposure is out there, market players can often be found adding up what’s known as vega. That’s a measure of how sensitive an option is to changes in volatility.

At Ambrus Group, another volatility hedge fund, an internal measure of vega aggregates options activity for the S&P 500 Index, the Cboe Volatility Index — a gauge of implied price swings in the US equity benchmark also known as the VIX — and the SPDR S&P 500 ETF Trust (SPY). Kris Sidial, co-chief investment officer, said in January the net short vega exposure was two times larger than in the run-up to the 2018 rout.

That means a 1-point increase in volatility could incur notional losses double those experienced six years ago. The big worry: Panicked investors unwinding positions as their losses mount could fuel more volatility, which causes more losses and more selling.

Such a scenario raises the risk of introducing another downside accelerant in the shape of the dealers and market makers who are usually on the other side of derivatives transactions. They don’t have their own directional view, so aim to maintain a neutral stance by buying and selling stocks, futures or options that offset each other.

In a big market decline — when dealers suddenly find themselves selling high quantities of options that protect or benefit from the rout — it tends to put them in what’s called “short gamma.” The dynamics are complex, but the upshot is that to neutralize their exposure dealers would have to sell into the downdraft, compounding the drop.

For now, the short-vol trade’s proliferation has been proposed as one reason why the VIX has stayed eerily low in the past year despite two ongoing major geopolitical conflicts and the Federal Reserve’s most aggressive monetary tightening in decades. That’s because in current conditions, dealers are in a “long gamma” position that generally sees them buying when stocks go down and selling when they go up — dampening swings.

In its latest quarterly review published last week, the Bank for International Settlements said that dynamic was the likely reason behind the compression of volatility given the boom in strategies that eke out income from selling options. “The meteoric rise of yield-enhancing structured products linked to the S&P 500 over the last two years has gone hand in hand with the drop of VIX over the same period,” researchers wrote.

There are good alternative reasons for the calm. The stock market has steadily ground higher as neither the Fed nor the US economy delivered any major shocks over the past year. It’s also possible that, with so many bets now placed using short-dated options, the VIX no longer captures all the action since it is calculated using contracts about one month out.

Yet QVR Advisors also sees the footprints of the boom in vol-selling. The degree of swings priced into S&P 500 options — so-called implied volatility — has drifted lower over the years versus how much the index actually moves around, its data show. The theory is that money managers flooding the market with contracts to generate income are putting a lid on implied volatility — which after all is effectively a gauge of the cost of options. The hedge fund has recently launched a strategy seeking to take advantage of cheap derivatives that benefit from large swings in the S&P 500, whether up or down.

“Post pandemic, we have seen fundamental and technical reasons for volatility suppression,” said Amy Wu Silverman, head of derivatives strategy at RBC Capital Markets. “While I think that continues, it becomes more and more difficult to be short volatility from here.”

Plenty of macro factors exist with the potential to disrupt the stock market’s steady march higher, including the ongoing wars in Ukraine and Gaza, lingering inflation and the American elections. And while vol-selling strategies have provided investors with gains historically, they have a reputation for their role in compounding routs.

The most famous episode took place in February 2018, when a downturn in the S&P 500 sparked a surge in the VIX, wiping out billions of dollars in trades betting against volatility that had built up during years of relative calm. Among the biggest casualties was the VelocityShares Daily Inverse VIX Short-Term note (XIV), whose assets shrank from $1.9 billion to $63 million in a single session.

A catalyst has yet to emerge to trigger a repeat. Even when the Israel-Hamas war broke out in October or the US reported hotter-than-expected inflation for January, the market remained serene. The VIX has stayed below its historic average of 20 for almost five months, a stretch of dormancy that was exceeded only two times since 2018.

To Tobias Hekster, co-chief investment officer at volatility hedge fund True Partner Capital, that enduring period of calm offers little reassurance.

“You are assuming a risk — the fact that that risk hasn’t materialized over the past one and a half years doesn’t mean it doesn’t exist,” Hekster said. “If something trips up the market, the longer the volatility has been suppressed, the more violent the reaction.”

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Credit: Source link