Super Micro Computer (NASDAQ: SMCI) and Intel (NASDAQ: INTC) have been in the limelight over the past year or so thanks to the ability of both companies to capitalize on the booming demand for artificial intelligence (AI) chips. But a closer look at the stock price performance of both companies tells us that investors are heavily favoring one of them over the other.

While share prices of Super Micro Computer (doing business as Supermicro) have jumped a stunning 776% in the past year, Intel has recorded relatively modest but solid gains of 71%, outpacing the PHLX Semiconductor Sector index’s 57% gains. Supermicro stock’s outstanding surge has brought its market cap from $5 billion a year ago to more than $48 billion as of this writing.

Intel’s market cap, on the other hand, has increased from $104 billion a year ago to $181 billion as of this writing. Supermicro, therefore, has enjoyed a much bigger surge in its market cap in the past year. But can it continue to outpace Intel on the stock market and become a bigger company in terms of market cap by 2027? Let’s find out.

Super Micro Computer expects to grow at a faster pace than Intel

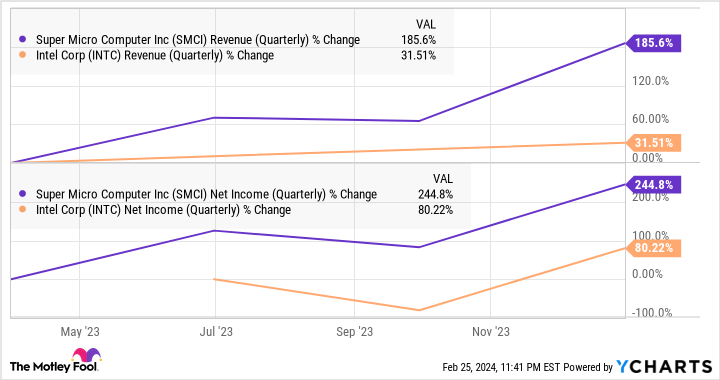

A big reason why the market has rewarded Supermicro stock with eye-popping gains is because of the terrific growth in the company’s revenue and earnings. A closer look at the chart below shows that Supermicro significantly outpaced Intel’s top- and bottom-line performance.

A closer look at the latest financial results of both companies shows why investors have been piling into Supermicro stock. The booming demand for AI chips turned out to be a bigger tailwind for Supermicro when compared to Intel. That’s because Supermicro’s server rack solutions allow data center operators to economically deploy AI accelerators in a way that they can reduce cooling and electricity costs while keeping performance at optimal levels.

It is worth noting that Supermicro’s AI server solutions are used for mounting AI chips from Intel, Nvidia, and Advanced Micro Devices. So, it doesn’t matter which of these chipmakers is selling more AI chips because data center operators are quite likely to turn to Supermicro for its modular server solutions. The company therefore sees robust growth in its revenue but also must aggressively invest in capacity expansion.

Supermicro’s revenue in the second quarter of fiscal 2024 (ended on Dec. 31, 2023) more than doubled on a year-over-year basis to $3.66 billion. The company anticipates $3.9 billion in revenue in the current quarter at the midpoint of its guidance range, which would be three times its revenue from a year ago.

So, Supermicro’s growth is all set to step on the gas in the current quarter. Additionally, the company expects to finish the year with $14.5 billion in revenue as compared to revenue of $7.1 billion in fiscal 2023. That would be a significant increase over the $7.1 billion in revenue it generated in the previous fiscal year.

Intel, on the other hand, hasn’t been able to capitalize on the AI chip boom yet because this market is currently being dominated by Nvidia. Intel’s revenue in the fourth quarter of 2023 was up 10% year over year to $15.4 billion, while its full-year revenue fell 14% to $54.2 billion thanks to the weakness in the personal computer (PC) market.

It is worth noting that Intel’s AI-related revenue pipeline stands at over $2 billion, according to management’s comments on the January earnings conference call. Supermicro, meanwhile, gets more than half its revenue from selling AI server solutions. So, AI is driving growth in a more meaningful way for Supermicro, and its business is growing at a much faster pace as a result.

More importantly, Supermicro is increasing its manufacturing capacity and believes that its efforts could help increase its annual revenue capacity to $25 billion. That would be nearly double the company’s revenue forecast in the current fiscal year. It won’t be surprising to see Supermicro hitting that target over the next three years as the demand for AI servers is expected to increase fivefold between 2023 and 2027.

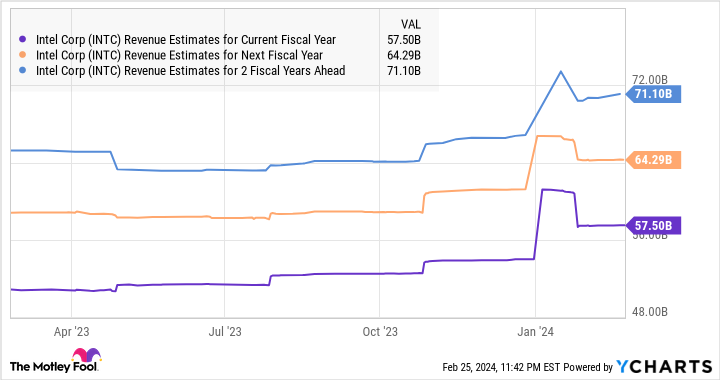

Assuming Supermicro achieves $25 billion in revenue in fiscal 2026, its three-year revenue compound annual growth rate (CAGR) would stand at 52%, using the fiscal 2023 revenue of $7.1 billion as the base. Intel’s revenue, on the other hand, is anticipated to increase at a much slower pace of 6% in the current fiscal year to $57 billion, followed by double-digit increases in 2025 and 2026.

However, will Supermicro’s faster growth help it become a bigger company than Intel?

Can Chipzilla be overtaken by Supermicro?

Assuming Supermicro indeed generates $25 billion in annual revenue within the next three years and maintains its current price-to-sales ratio of 5.4 at that time, its market cap could increase to $135 billion. That would be almost three times the company’s current market cap. Intel, meanwhile, is currently trading at 3.4 times sales. A similar sales multiple after three years would bring its market cap to $242 billion, a jump of 33% from current levels.

So, Intel is likely to remain the bigger company after three years, but it is worth noting that Supermicro has the potential to deliver a much stronger upside to investors. Supermicro isn’t all that expensive when compared to Intel as far as the sales multiple is concerned, especially considering the eye-popping growth it is delivering. So it may be a good idea for investors to buy Supermicro because it has the potential to sustain its rally and remain a red-hot growth stock.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

See the 10 stocks

*Stock Advisor returns as of February 26, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices and Nvidia. The Motley Fool recommends Intel and Super Micro Computer and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, and short February 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

Will Super Micro Computer Be Worth More Than Intel by 2027? was originally published by The Motley Fool

Credit: Source link