Nio (NYSE: NIO) has taken investors on a wild ride since its public debut. The Chinese electric vehicle (EV) maker went public at $6.28 per American depositary share (ADS) on Sept. 12, 2018, and its shares rallied to an all-time high of $62.84 on Feb. 9, 2021. At its peak, Nio’s enterprise value reached $91.4 billion, or 16 times the sales it would generate in 2021.

But as of this writing, Nio trades at about $6 per share with an enterprise value of $12.1 billion — which is just over 1 times the sales it’s expected to generate in 2024. Let’s see why this hot EV stock took a roundtrip back to its IPO price, if it’s a bargain at these levels, and if it has a shot at becoming a trillion-dollar EV maker over the next few decades.

Nio’s biggest challenges

Nio sells a wide range of electric sedans and SUVs, and its cheapest models start at around $46,000. It started delivering its first vehicles in 2018, and its deliveries have grown at an impressive rate over the following five years.

Metric | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

|---|---|---|---|---|---|---|

Deliveries | 11,348 | 20,565 | 43,728 | 91,429 | 122,486 | 160,038 |

Growth | –* | 81% | 113% | 109% | 34% | 31% |

Data source: Nio. *Deliveries started in 2018.

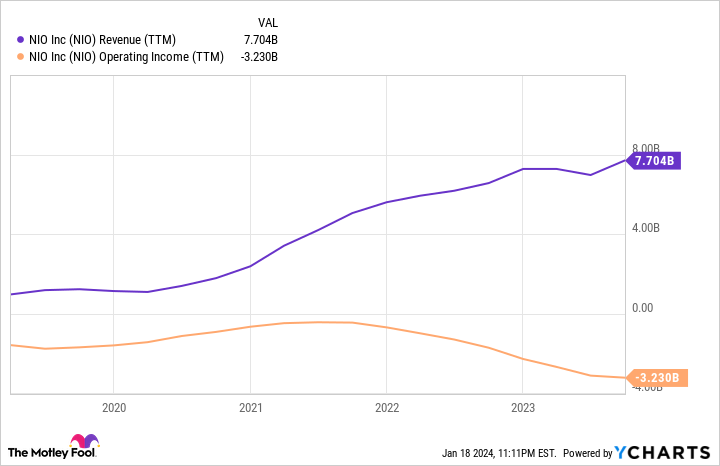

However, Nio’s deliveries decelerated in 2022 and 2023 as it grappled with supply chain constraints, macro headwinds, and the ongoing pricing war in China’s EV market — which was exacerbated by Tesla‘s steep price cuts. That pressure also reduced its vehicle margins from a peak of 20.1% to just 11% in the third quarter of 2023.

As Nio’s vehicle margins shrank, it continued to expand its network of battery-swapping stations, which enable its drivers to swap out their depleted batteries for fully charged ones. That unique design differentiates Nio’s vehicles from its competitors, but the high costs of building its battery-swapping networks caused it to rack up steep operating losses.

From 2018 to 2021, Nio’s operating margin improved from negative 180.1% to negative 12.4%, fueling hopes that it would eventually break even. Unfortunately, that figure dropped to negative 27.1% in 2022 — and analysts anticipate a negative operating margin of 35.2% in 2023 when it posts its full-year earnings in late February or early March.

For the full year, analysts expect Nio’s revenue to rise 13% to 55.6 billion yuan ($7.8 billion) as its net loss widens from 14.6 billion yuan ($2.1 billion) to 18.6 billion yuan ($2.6 billion).

That’s a grim outlook for a company that ended its latest quarter with a high debt-to-equity ratio of 5.2. By comparison, Tesla — which is firmly profitable — ended its latest quarter with a much lower debt-to-equity ratio of 0.7. That red ink and high leverage could limit Nio’s gains as long as interest rates stay elevated.

The mathematical path toward $1 trillion

In a best-case scenario, Nio could gradually stabilize its deliveries and margins as economies of scale kick in. Warmer relations between the U.S. and China could also drive the bulls back toward U.S.-listed Chinese stocks, and it could successfully expand into Europe and other overseas markets.

If that happens, I believe the market could value Nio more closely to Tesla, which currently trades at 6 times its 2024 sales. If Nio trades at 6 times sales and steadily grows its revenue at a compound annual growth rate (CAGR) of 12% from $7.8 billion in 2023 to $166.7 billion in 2050, it could be worth $1 trillion by the final year.

However, that’s a pretty tall order because it would make Nio larger than today’s Tesla — which is expected to generate $117 billion in revenue in 2024. It also assumes Nio can stand out and keep growing in its saturated market.

If Nio survives all those tests, it might have a shot at joining the 12-zero club — but it’s far too early to tell with over 200 EV makers (including the smartphone giants Xiaomi and Huawei) carving up China’s fragmented market. That rapid commoditization could flush out unprofitable underdogs like Nio.

Look beyond Nio’s market cap

Nio’s downside might be limited at these levels, but its stock could remain near its IPO price until it accelerates its deliveries and narrows its operating losses again. So instead of focusing on Nio’s ability to become a trillion-dollar EV giant, investors should look for those green shoots to see if it can generate meaningful gains over the next few years.

Should you invest $1,000 in Nio right now?

Before you buy stock in Nio, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nio wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

See the 10 stocks

*Stock Advisor returns as of January 16, 2024

Leo Sun has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nio and Tesla. The Motley Fool has a disclosure policy.

Will Nio Be a Trillion-Dollar Stock by 2050? was originally published by The Motley Fool

Credit: Source link