Stocks are on an unstoppable hot streak right now, with eight straight sessions in the green for the S&P 500 (SPX), the longest win streak since last November. Undoubtedly, Technology stocks are leading the path higher, just weeks after many investors thought the markets would tank and that less-loved mid-cap and value plays would lead us higher. With Tech stocks in the driver’s seat again, it may be time for many to revisit the drawing board for value from the latest swoon.

In this piece, we’ll check in with TipRanks’ Comparison Tool to gauge which trio of tech titans — SQ, INTU, and AMZN — has the most year-ahead upside, according to Wall Street analysts.

Block, formerly known as Square, is a financial technology company (it owns Cash App and other services) whose shares have been choppily consolidating in a wide range in recent years. Indeed, the stock has broken the hearts of many investors, but the tides may be about to change.

Recently, Bank of America (BAC) pounded the table on SQ stock, noting “undervaluation” and “underappreciation.” With potentially overlooked catalysts (think the major corporate restructure) on the horizon, I’m staying bullish on the stock.

Now down close to 9% in the past two years and 13.5% year-to-date, SQ stock seems like a Tech sector dud. Despite beating handsomely on earnings for the past two quarters, the stock seems to lack the excitement factor it once had. Whether it’s a lack of blockchain innovations or operating challenges that led CEO and “Block Head” Jack Dorsey to reorganize his entire company, investors are demanding more from the firm in the AI age. Whether last month’s corporate reshuffling helps Block regain its competitive spirit again remains to be seen.

Regardless, the company has plans to get back on the high road. Specifically, the company’s “Rule of 40” by 2026 plan sets a pretty high (but realistic) bar, with gross profit and adjusted operating income targets set at 15% and 25% (a sum of 40%), respectively.

Bank of America analyst Jason Kupferberg, who has a Buy rating on the stock and an $82.00 per share price target entailing more than 22% upside, praised Block for already “demonstrating nice progress” on its Rule of 40. As Block pushes for greater efficiency, the firm must introduce new innovations to jolt sales. Introducing new financial services in the Cash App ecosystem (like Cash App Borrow) is worth banking on.

What Is the Price Target for SQ Stock?

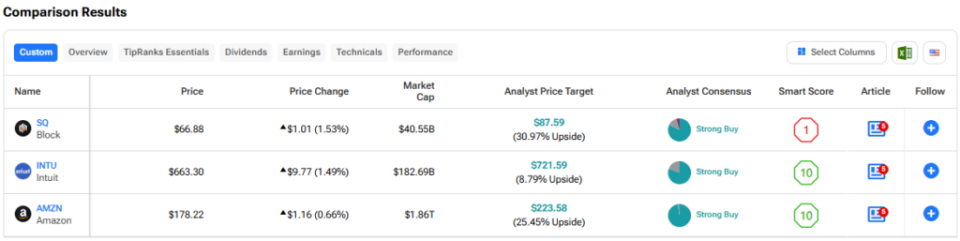

SQ stock is a Strong Buy, according to analysts, with 24 Buys, six Holds, and one Sell assigned in the past three months. The average SQ stock price target of $88.90 implies 32.9% upside potential.

See more SQ analyst ratings

Shares of financial technology software firm Intuit (mostly known for its tax-filing software, TurboTax) are flirting with new highs again, now down just over 5% from all-time highs and 2% away from 52-week highs. Undoubtedly, the $670 ceiling of resistance has proven challenging to break through over the past six months. As the company looks to lay off and rehire with AI in mind, perhaps investors seeking “AI monetization” plays will have more to love from the name from a longer-term perspective. Though the valuation multiple has expanded considerably in recent weeks, I’m inclined to stay bullish on INTU stock.

Intuit is serious about AI-driven growth. But unlike many other firms that are more than willing to overinvest than underinvest (think Alphabet (GOOGL)), Intuit is also serious about keeping its balance sheet in great shape while emphasizing driving operating efficiencies. As more investors reward return on AI investment rather than the ambition of AI narratives and the size of spending budgets, Intuit may just be one of the firms that starts standing out from the pack, if it hasn’t already.

Intuit’s AI offering, Intuit Assist, is an innovative tool designed to enhance productivity in financial software by providing AI-driven assistance and insights. Over time, it could become highly monetizable, similar to how Microsoft (MSFT) has successfully monetized Copilot. Whether Intuit can achieve the same success remains to be seen, but it is clear that financial software is a sector poised for significant AI-driven disruption, and Intuit is positioned well to ride that wave.

Indeed, Intuit stands to add immense value for users by sprinkling generative AI across QuickBooks, TurboTax, Credit Karma, and Mailchimp to improve the user experience. With value creation comes the opportunity to charge higher prices. At the end of the day, users will likely be more than willing to open their wallets wider if there’s more value, whether that’s in the form of time savings or increased accuracy.

At 34.7 times forward price-to-earnings, INTU stock is on the pricier side of its past-year historical range. Given its realistic opportunity to monetize AI and the generative AI operating system (GenOS) it’s built from the ground up, I’d argue the premium is worth paying.

What Is the Price Target for INTU Stock?

INTU stock is a Strong Buy, according to analysts, with 18 Buys and four Holds assigned in the past three months. The average INTU stock price target of $722.61 implies 8.9% upside potential.

See more INTU analyst ratings

Shares of e-commerce and cloud behemoth Amazon cratered in July and earlier this month as the market sell-off dragged the Nasdaq 100 (NDX) into correction territory. Undoubtedly, it wasn’t just investors turning against tech that caused AMZN stock to crumble nearly 25% from peak to trough. The company’s latest quarter left a lot to be desired.

In any case, AMZN stock has an opportunity to take its relief rally into high gear as investors focus on the road ahead and growth drivers that could help the firm level up. As one of the more magnificent buy-the-dip opportunities today, I’m inclined to stay bullish on the stock.

Up ahead, look for Amazon to reveal more specifics on how it intends to take on Chinese e-commerce rivals like PDD Holdings’ (PDD) Temu at the very low end of the cost spectrum.

Undoubtedly, Amazon has a lot of market share to take on the low end of e-commerce, and I think Amazon has more than enough tools to get the job done and done well. The Magnificent Seven behemoth certainly does logistics better than most. However, the big question remains whether it can minimize costs and shipping times on goods coming from China.

As Amazon’s low-cost marketplace goes live this fall, perhaps some of the enthusiasm propelling PDD stock can spread over to AMZN. As the early reviews release, we’ll gain a glimpse of what could be one of Amazon’s next big growth avenues. At 42.4 times trailing P/E, AMZN is still pricier than most of its Magnificent Seven peers. However, given the opportunity to steal Temu’s lunch and continued advancements on the AI front (Amazon just bought another AI firm, Perceive, a few days ago), such a premium is well-earned.

What Is the Price Target for AMZN Stock?

AMZN stock is a Strong Buy, according to analysts, with 41 Buys and one Hold assigned in the past three months. The average AMZN stock price target of $223.58 implies 25.5% upside potential.

See more AMZN analyst ratings

The Takeaway

There are plenty of underappreciated Tech stocks that have room to soar even higher as the market rebound endures. Whether we’re talking about Block and progress on its “Rule of 40,” Intuit and its enviable AI monetization opportunity, or Amazon and the potential of its coming Temu rival, the following trio have the catalysts they need to ascend. Of the trio, Wall Street sees the most upside (33%) in SQ stock. I’m inclined to agree with analysts. If Jack Dorsey can right the ship, SQ stock’s comeback could be pronounced.

Disclosure

Credit: Source link