Do you love dividends? Of course you do — and rightly so!

In a recent study conducted by Mike Wilson, Chief Investment Officer at Morgan Stanley, the analysis focused on the performance of dividend-paying stocks compared to non-dividend-paying stocks since the year 2000. The historical data underscores a compelling trend: dividend-paying stocks consistently outperform non-dividend stocks over the medium to long term.

That outperformance has even been more pronounced in times of uncertainty and market retreats. “Specifically,” Wilson noted, “the majority of outperformance comes during large market pullbacks such as 2000, 2008, 2015, and 2020.”

With uncertainty currently prevailing, Wilson believes it might be the right time to seriously consider loading up on these classic defensive plays.

Against this backdrop, the analysts at Morgan Stanley have pinpointed an opportunity in a pair of dividend stocks with enticing attributes: a high dividend yield to outpace the current inflation rate, an attractive valuation, and the potential for future share price growth.

In fact, it’s not only Morgan Stanley who favors these names. Using the TipRanks database, we found that both are also rated as ‘Strong Buys’ by the analyst consensus. Let’s take a closer look.

Philip Morris International (PM)

We’ll start with one of the best-known names in the ‘sin sector,’ Philip Morris International. This is a leader in the tobacco industry, and the owner, with full production and marketing rights, of the Marlboro cigarette brand’s international footprint. Some of the company’s other brand names include L&M, Chesterfield, and Next, along with – you guessed it – Philip Morris. The company has a presence in over 175 global markets, and can boast that, in most of them, it holds the first- or second-place market share for cigarettes and other tobacco products.

Those leading market shares are solid assets, because even with the growing social pressures against smoking, the tobacco industry totaled some $867 billion in 2022 – and by the end of this decade, the industry is expected to hit a value of $1.05 trillion.

One of the chief effects of anti-smoking pressure, be they social or political, has been to push Philip Morris toward increased diversification of its product lines. The company is a leader not just in cigarettes but also in the expanding market for smokeless tobacco products. Over the past few years, PM has invested over $10.5 billion into such products, and the company has seen smokeless non-nicotine products increase their share of total revenue from 29.1% in 2021 to nearly 35% in 2022. The company is targeting 50% of revenues from smoke-free products by 2025. PM’s portfolio of smokeless products includes the growing line of iQOS heated tobacco products, multiple e-vape products, and a range of oral smokeless tobaccos.

Philip Morris will release its financial results for 3Q23 later this month, but we can look back at Q2 and get an idea of just where the company stands. The second quarter top-line came in at a hair under $9 billion, growing 14.5% year-over-year and beating the forecast by more than $259 million. The firm’s bottom line figure, a non-GAAP EPS of $1.60, was 12 cents per share better than had been anticipated.

Looking ahead, the Street expects to see revenues of $9.31 billion and a non-GAAP EPS of $1.61 when PM releases its Q3 results on October 19.

Rising revenues and earnings are supporting a solid dividend, which PM raised in its last declaration. The announcement, on Sept 13, set the common share quarterly dividend at $1.30 per share, for a 2.4% increase from the previous payout. The annualized rate of $5.20 gives a yield of 5.6%, well above the last reported annualized inflation rate, of 3.67% in August.

Covering this stock for Morgan Stanley, analyst Pamela Kaufman focuses on the company’s shift from cigarettes to smokeless tobacco as the key point for investors to consider going forward. She writes, “PM is our Top Pick as its peer-leading growth outlook is supported by its successful transition to smoke-free products and reflects: 1) accelerating HTU (heated tobacco units) share from IQOS ILUMA rollout; 2) continued rapid Zyn growth in the US; 3) a large and attractive US growth opportunity for IQOS with moderate investment needs; and 4) opportunity for EBIT margin expansion. We believe valuation at 11x 2024 EV/EBITDA is attractive.”

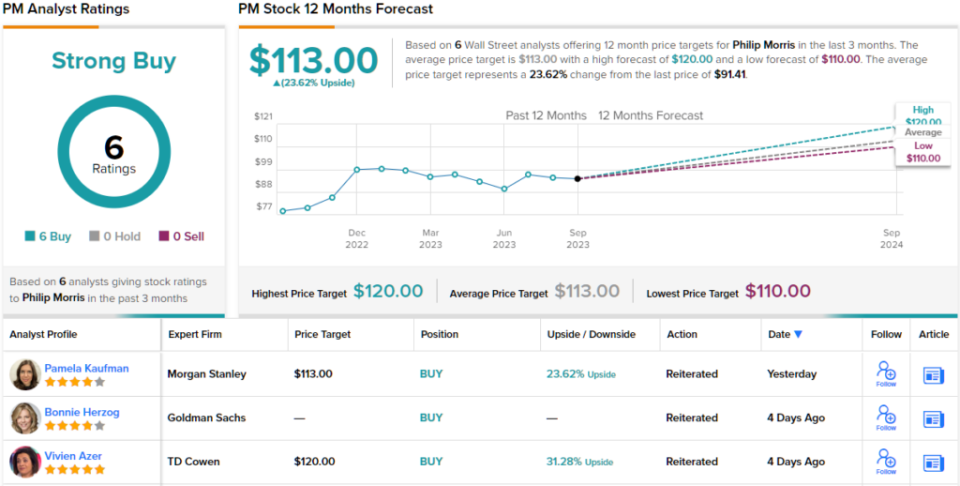

Kaufman’s bullish stance supports her Overweight (i.e. Buy) rating on the stock, while her $113 price target indicates her confidence in ~24% one-year upside potential for the shares. Adding in the dividend, and the total return on this stock is ~29% for the year ahead. (To watch Kaufman’s track record, click here)

Overall, all 6 of the recent analyst reviews on this tobacco company are positive, making for a unanimous Strong Buy consensus rating. PM shares are priced at $91.41, and their $113 average price target implies ~24% upside heading out to the one-year horizon. (See PM stock forecast)

Bridge Investment Group (BRDG)

Next up, Bridge Investment Group, is a real estate investment trust, or REIT, a class of companies long known as ‘dividend champs.’ Bridge is a vertically integrated real estate manager, and its portfolio contains a wide range of financial instruments and properties. These include real-estate-backed credit, along with residential properties, offices spaces, logistics properties, and industrial-use net leased real estate.

Not only is Bridge’s portfolio diverse in its broad categories, but the company also works hard to develop diversified holdings within each category. The logistic properties, for example, include warehouses and transport hubs, and the company’s developments include EV charging, LED lighting, and solar power installations whenever feasible. Bridge’s residential properties include single-family rentals, senior housing, and multi-family apartments. And in the credit space, Bridge uses a variety of strategies to assemble a diverse set of MBS assets.

At the bottom line, all of this added up to distributable earnings of 20 cents per share in the company’s 2Q23 financial release, based on a net total of $35 million. This was in-line with expectations. Dividend investors should note that Bridge has a history of adjusting its payout to keep it in-line with distributable earnings. The current dividend, of 17 cents per share, annualizes to 68 cents per common share, and gives a yield of 7.4%, more than enough to ensure a real rate of return in today’s environment.

This company’s dividend is attractive, but Morgan Stanley’s Michael Cyprys takes a closer look at Bridge’s exposure to commercial real estate (CRE). This is a serious concern, as CRE is flashing danger signs in multiple important urban areas, but Cyprys sees reason to believe that Bridge can weather this storm and continue to deliver returns to investors. He writes, “Private markets real estate manager trading at depressed valuation due to blanket negativity that stems from rising CRE risks around debt refi and valuations. We think the market should be more discerning given BRDG has limited principal & redemption risk and instead earns fees on locked-up, committed 3rd party capital. While growth slows near-term (slower fundraising and transactional activity), we still expect mid-teens growth in assets and FRE. Fed pause could catalyze pickup in activity later in ’23/into ’24, particularly if rates volatility is dampened.”

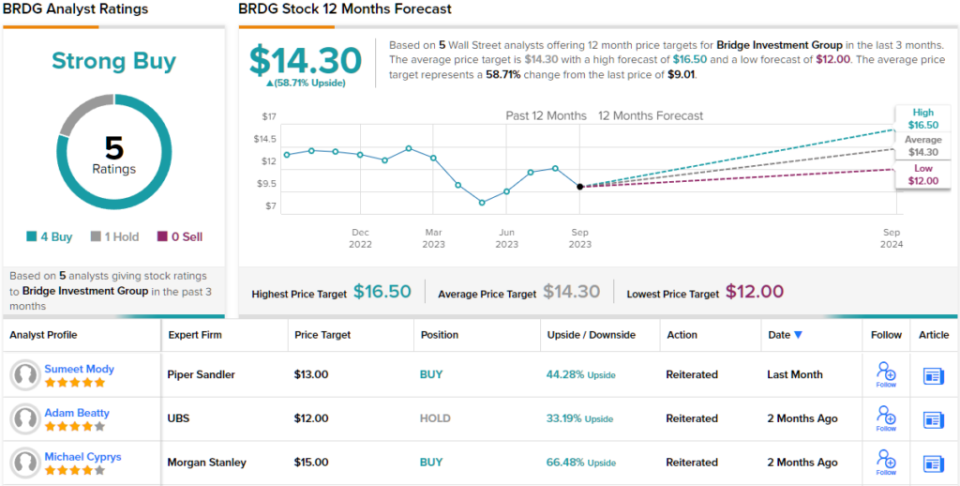

These comments back up Cyprys’ Overweight (i.e. Buy) rating on the stock with his $15 price target suggesting a gain of ~66% in the year ahead. (To watch Cyprys’ track record, click here)

Overall, this stock gets a Strong Buy consensus rating, based on 5 reviews that include 4 to Buy and 1 to Hold. Shares are trading for $9.01 with an average target price of $14.30 to imply ~59% one-year upside potential. (See BRDG stock forecast)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Credit: Source link