Technology stocks have delivered outstanding gains to investors since the beginning of 2023, with a 69% jump in the value of the Nasdaq-100 Technology Sector index over this period. Artificial intelligence (AI) has played a central role in this tremendous rally.

Technology companies, big and small, have been benefiting from the adoption of AI. Super Micro Computer (NASDAQ: SMCI) and Taiwan Semiconductor Manufacturing (NYSE: TSM) have both received a nice lift thanks to the proliferation of AI.

However, the red-hot rally in technology stocks has recently come to a halt. The Nasdaq-100 Technology Sector is down 11% in the past month thanks to a number of factors such as rising concerns about a recession in the U.S. following a weak jobs report and fears that AI won’t eventually live up to the hype.

But the recent quarterly results from the companies mentioned above suggest otherwise. These tech players indicate that AI-related infrastructure spending continues to remain solid, so it may be a good idea to buy shares of these AI companies in the wake of the recent market sell-off. Let’s look at the reasons why.

TSMC stock is too attractive to miss out on right now

AI has given the semiconductor industry a big boost. The market for AI chips is expected to clock an annual growth rate of 38% over the next decade, generating annual revenue of $514 billion in 2033. Taiwan Semiconductor Manufacturing, popularly known as TSMC, is one of the best ways for investors to capitalize on this opportunity.

TSMC is a foundry that manufactures chips for fabless semiconductor companies such as Nvidia and AMD. It also makes chips for device manufacturers such as Apple, and even Intel has been tapping TSMC to manufacture advanced chips despite having its own production lines. So, TSMC stands to gain from the proliferation of AI in multiple markets such as data centers, smartphones, and personal computers.

TSMC’s growth has been accelerating thanks to the robust demand for its advanced chips from the customers mentioned above. The Taiwan-based foundry giant reported a 33% year-over-year increase in revenue for the second quarter of 2024 to $20.8 billion. That marked a significant acceleration over the 13% year-over-year growth TSMC reported in Q1.

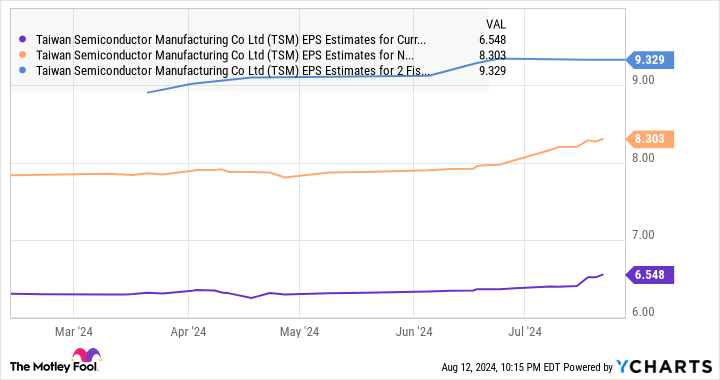

For the third quarter, TSMC is forecasting revenue of $22.8 billion at the midpoint of its guidance range. That would translate to year-over-year growth of almost 32%, suggesting that the demand for the company’s chips is set to remain healthy. As such, the 15% pullback in TSMC stock in the past month presents a smart buying opportunity for investors, especially considering that analysts have raised their earnings growth expectations from TSMC lately.

Also, TSMC is currently trading at 29 times trailing earnings, which is a slight discount to the Nasdaq-100 index’s average earnings multiple of 31 (using the index as a proxy for tech stocks). Buying this AI stock right now looks like a no-brainer considering its terrific growth and attractive valuation.

AI server demand is driving stunning growth for Supermicro

The chips manufactured by TSMC that are deployed in data centers to tackle AI workloads need to be mounted on server racks — resulting in tremendous demand for Supermicro’s offerings in the past year.

Supermicro manufactures server and storage solutions, and the company has been gaining ground in the AI server market thanks to its modular offerings that allow data center operators to reduce energy costs. Its revenue in the recently concluded fiscal year 2024 more than doubled year over year to $14.9 billion from $7.1 billion in the previous year.

However, Supermicro stock fell 20% in a single session following its results after it missed Wall Street’s earnings expectations on account of its narrowing margins. The company has been investing aggressively to raise its production capacity to meet the booming demand for AI servers, and that’s precisely why its non-GAAP gross margin was down to 14.2% in fiscal 2024 from 18.1% in the preceding year.

The company has been expanding its manufacturing capacity at several locations around the globe as it aims to ramp up the production capacity of liquid-cooled servers, which are gaining traction in AI data centers to reduce electricity consumption and increase performance. Mordor Intelligence estimates that liquid-cooled data centers could achieve annual growth of 23% through 2029.

So, Supermicro is doing the right thing by focusing on capacity expansion right now as it should be able to capture a bigger share of this fast-growing opportunity. What’s more, the overall AI server market is expected to clock 30% annual growth through 2033, and Supermicro is growing at a much faster pace than this space.

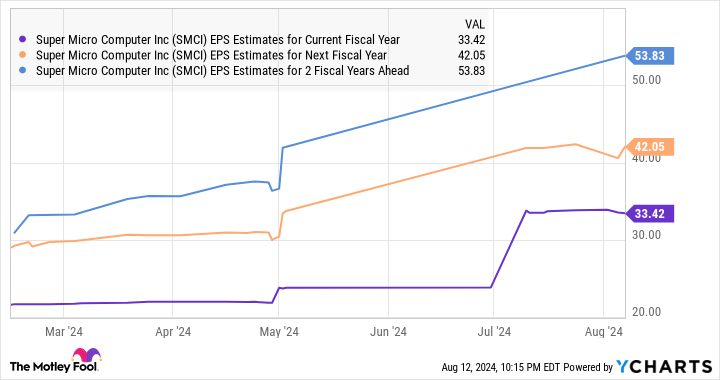

This suggests that the company is gaining market share in AI servers, and that’s why sacrificing margins in the short term looks like the right thing to do considering the long-term opportunity at hand. Supermicro management believes that its margins will return to the normal range by the end of fiscal 2025. Analysts remain bullish about its bottom-line growth prospects following fiscal 2024’s earnings jump of 87% to $22.09 per share.

Most importantly, Supermicro is now trading at just 24 times trailing earnings and 13 times forward earnings — a nice discount to the Nasdaq-100 index. Investors should consider adding this fast-growing company to their portfolios while it remains beaten down.

Should you invest $1,000 in Taiwan Semiconductor Manufacturing right now?

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $763,374!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of August 12, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel and short August 2024 $35 calls on Intel. The Motley Fool has a disclosure policy.

Stock Market Sell-Off: The Best Artificial Intelligence (AI) Growth Stocks to Buy Right Now was originally published by The Motley Fool

Credit: Source link