- The yield on the benchmark 10-year Treasury note, a key barometer for mortgage rates, auto loans and student debt, hit 5% for the first time since 2007 on Thursday.

- Borrowing costs could head even higher as a result.

- One group that stands to benefit from higher rates: savers.

The yield on the benchmark 10-year Treasury crossed 5% for the first time in 16 years on Thursday, causing a ripple effect that could raise rates on mortgages, student debt, auto loans and more.

After Federal Reserve Chair Jerome Powell said “inflation is still too high,” expectations that the U.S. central bank could continue to tighten monetary policy sent the 10-year yield over the key psychological level for the first time since July 2007.

“That has real impacts on the economy, ultimately affecting every individual in the U.S.,” said Mark Hamrick, Bankrate.com’s senior economic analyst.

The yield on the 10-year note is a barometer for mortgage rates and other types of loans.

“When the 10-year yield goes up, it will have a knock-on effect for almost everything,” according to Columbia Business School economics professor Brett House.

Even though many of these consumer loans are fixed, anyone taking out a new loan will likely pay more in interest, he said.

Why Treasury yields have jumped

A bond’s yield is the total annual return investors get from bond payments. There are many factors driving the recent spike in Treasury yields, economists said.

For one, yields tend to rise and fall according to the Federal Reserve’s interest rate policy and investors’ inflation expectations.

In this case, the central bank has hiked its benchmark rate aggressively since early 2022 to tame historically high inflation, pushing up bond yields. Inflation has fallen significantly since then. However, Fed officials and recent strong U.S. economic data suggest interest rates will likely have to stay higher for a longer time than many expected to finish the job. Higher oil prices have also fed into inflation fears.

But interest rates are just part of the story.

Most of the recent jump in Treasury yields is due to a so-called “term premium,” said Andrew Hunter, deputy chief U.S. economist at Capital Economics.

Basically, investors are demanding a higher return to lend their money to the U.S. government — in this case, for 10 years. One reason: Investors seem skittish about rising U.S. government debt, Hunter said. Generally, investors demand a higher return if they perceive a greater risk of the government’s inability to pay back debt in the future.

Mortgage rates will stay high

Most Americans’ largest liability is their home mortgage. Currently, the average 30-year fixed rate is up to 8%, according to Freddie Mac.

“For those who are planning to buy a home, this is really bad news,” said Eugenio Aleman, chief economist at Raymond James.

“Mortgage rates will probably continue to go up and that will push affordability farther away.”

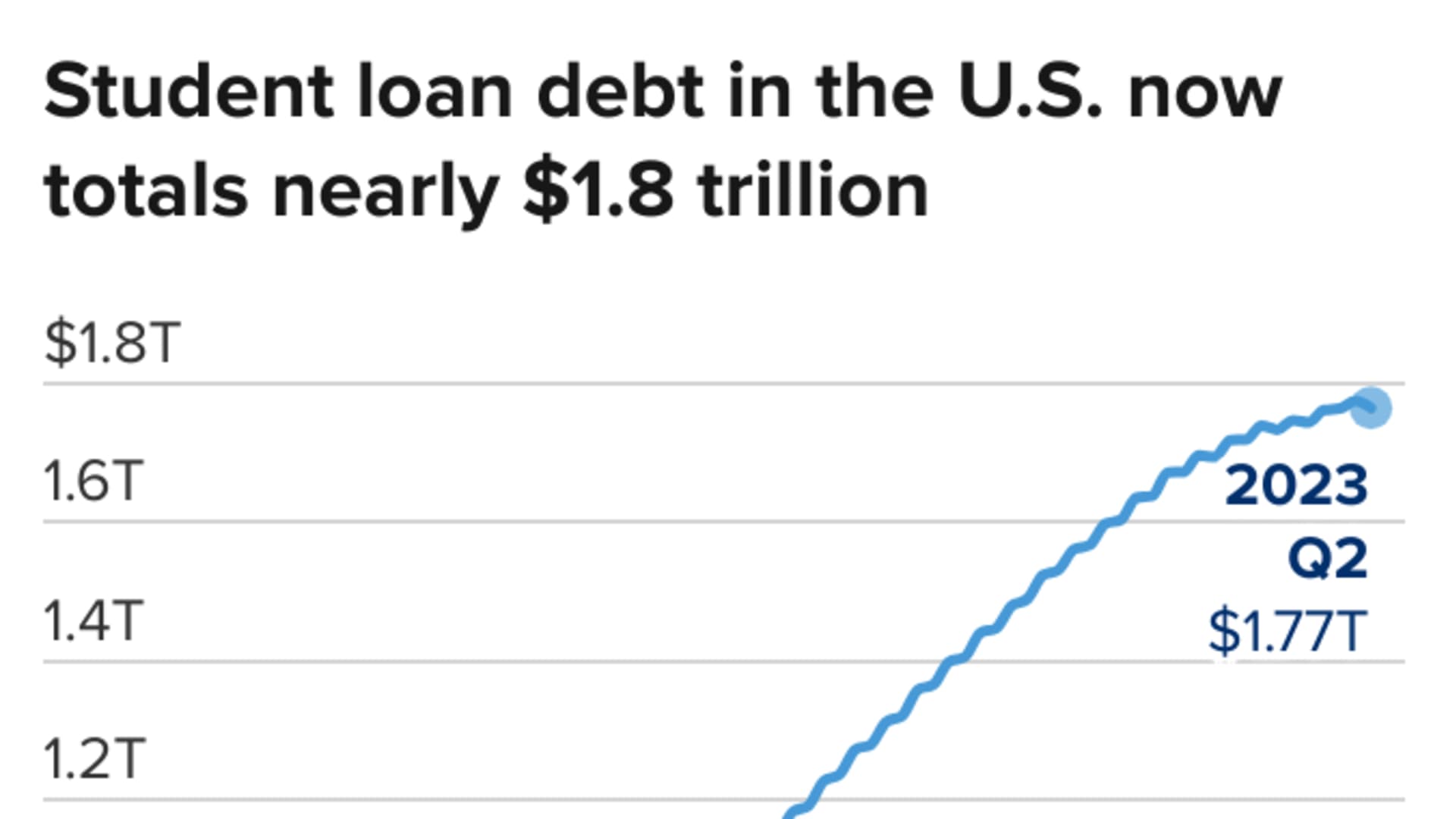

Student loans could get pricier

There is also a correlation between Treasury yields and student loans.

A college education is the second-largest expense an individual is likely to face in a lifetime, right after purchasing a home. To cover that cost, more than half of families borrow.

Undergraduate students who take out new direct federal student loans for the 2023-24 academic year are now paying 5.50% — up from 4.99% in the 2022-23 academic year and 3.73% in 2021-22.

The government sets the annual rates on those loans once a year, based on the 10-year Treasury.

If the 10-year yield stays above 5%, federal student loan interest rates could increase again when they reset in the spring, costing student borrowers even more in interest.

Car loans are getting more expensive

There is also a loose correlation between Treasury yields and auto loans. The average rate on a five-year new car loan is currently 7.62%, the highest in 16 years, according to Bankrate. Now, more consumers face monthly payments that they likely cannot afford.

“There are only so many people who can carve out an $800 to $1,000 car payment,” Bankrate’s Hamrick said.

More from Personal Finance:

The inflation breakdown for September 2023 — in one chart

Social Security cost-of-living adjustment will be 3.2% in 2024

Lawmakers take aim at credit card debt, interest rates, fees

While other types of borrowing, including credit cards, small business loans and home equity lines of credit, are predominantly pegged to the federal funds rate and rise or fall in step with Fed rate moves, those rates could head higher, too, according Aleman.

“Everything from business loans to consumer loans is going to be affected,” he said.

Savers can benefit

One group that does stand to benefit from higher yields is savers.

“For many years, we’ve been bemoaning the plight of savers,” Hamrick said. But because yields tend to be correlated to changes in the target federal funds rate, deposit rates are finally higher.

High-yield savings accounts, certificates of deposits and money market accounts are now paying over 5%, according to Bankrate, which is the most savers have been able to earn in more than 15 years.

“This is the rare time in recent history when cash looks pretty good,” Hamrick said.

Subscribe to CNBC on YouTube.

Don’t miss these CNBC PRO stories:

Credit: Source link