The launch of generative artificial intelligence (AI) application ChatGPT whipped Wall Street into a frenzy in late 2022. While the generative AI revolution is still in its early stages, chipmaker Nvidia (NASDAQ: NVDA) has already been a big winner.

Nvidia was the best-performing stock in the S&P 500 last year, primarily because interest in AI drove unprecedented demand for its graphics processing units (GPUs). Shares have now advanced 510% since the beginning of 2023, but there’s a possible inflection point on the horizon.

Nvidia will announce first-quarter financial results after market close on Wednesday, May 22, at 5 p.m. ET. For context, the stock surged 16% following its exceptional fourth-quarter financial report, and shareholders are undoubtedly hoping for an encore performance. However, Wall Street analysts have particularly high expectations this time around.

Should you buy Nvidia stock before May 22?

Nvidia impressed Wall Street with triple-digit growth in the fourth quarter

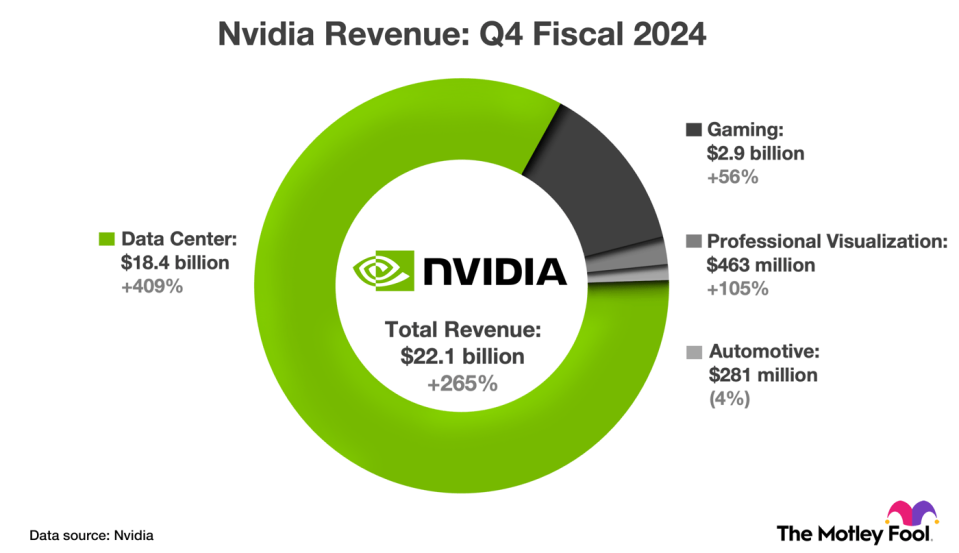

Nvidia crushed expectations with its fourth-quarter financial report. Revenue increased 265% to $22.1 billion on particularly strong momentum in the data center product category, due in large part to demand for artificial intelligence systems and software. And non-GAAP net income soared 491% to $12.8 billion.

The chart below shows Nvidia’s fourth-quarter revenue growth across its four primary product categories.

On the earnings call, CEO Jensen Huang attributed strong fourth-quarter results to two platform shifts. Data centers are moving from general purpose to accelerated computing and evolving into generative AI factories that turn massive amounts of raw information into digital intelligence. “Nvidia AI supercomputers are essentially AI generation factories of this industrial revolution,” Huang told analysts.

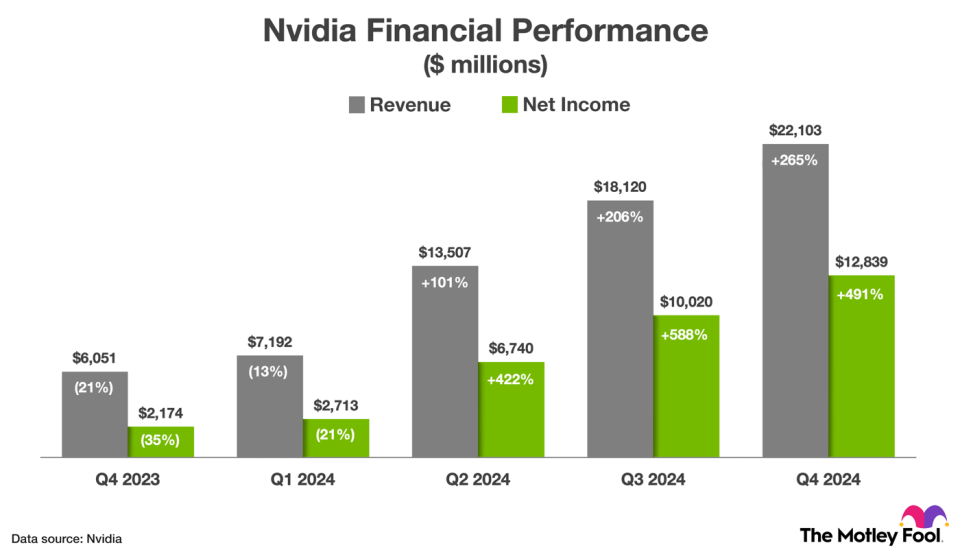

Glancing back, Nvidia has now achieved triple-digit revenue and non-GAAP net income growth for three consecutive quarters, as shown in the chart below.

Wall Street expects a phenomenal first-quarter report from Nvidia

In the first quarter, Nvidia expects revenue to increase 234% to $24 billion. Management also provided guidance for its non-GAAP gross margin, operating margin, and tax rate, such that non-GAAP net income is forecast to increase by about 416% to $5.62 per diluted share.

By comparison, the Wall Street consensus calls for first-quarter revenue to increase 240% to $24.5 billion, and non-GAAP net income to increase 409% to $5.55 per diluted share. Analysts also expect second-quarter revenue to increase 96% to $26.5 billion, with non-GAAP net income increasing 119% to $5.91 per diluted share.

Nvidia reported better-than-expected results in each of the last four quarters, and the company also provided guidance that meaningfully exceeded the Wall Street consensus in the fourth quarter. Anything less this time around could sink the stock. Alternatively, shares could soar if Nvidia beats expectations and guides above the consensus.

Nvidia has a strong presence in several parts of the AI economy

The bull case for Nvidia builds on its unique position in the AI economy. Its graphics processing units (GPUs) are the gold standard in accelerating complex data center workloads like AI applications. Nvidia holds between 80% and 95% market share in AI chips, according to analysts. But the company is also gaining ground in other product categories.

For instance, Nvidia recently introduced a data center central processing unit (CPU). In the third quarter, CEO Jensen Huang told analysts, “We are on a very, very fast ramp with our first data center CPU to a multibillion-dollar product line.” Additionally, high-performance networking equipment has become a $10 billion business for Nvidia, and its nascent software and services offering achieved an annual revenue run rate of $1 billion in the fourth quarter.

In short, Nvidia is a one-stop shop for artificial intelligence, and Goldman Sachs analyst Toshiya Hari sees that as a key differentiator. As he wrote in a recent note to clients:

We believe Nvidia will remain the de facto industry standard for the foreseeable future given its competitive advantage that spans hardware and software capabilities. Nvidia’s annual introduction of new products and platforms sets a pace of innovation that keeps it at the forefront of the industry.

Nvidia stock looks pricey, so investors should be cautious

The graphics processor market is projected to grow by 28% annually through 2030, and AI spending across hardware, software, and services is forecast to increase at 37% annually during the same period. That gives Nvidia a good shot at annual earnings growth of around 30% through the end of the decade.

Wall Street expects the company to grow earnings per share at 35% annually over the next three to five years. In that context, the stock’s current valuation at 74 times earnings looks pricey.

Personally, I would wait for a cheaper multiple, but investors intent on buying the stock today should start with a very small position. Expectations surrounding first-quarter earnings are sky-high, so there’s a very real possibility that shares plunge following the report.

If that happens, patient investors should consider buying a bigger position in Nvidia at that time. If it doesn’t happen, plenty of other companies are well-positioned to benefit from the AI boom.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $553,959!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of May 6, 2024

Trevor Jennewine has positions in Nvidia. The Motley Fool has positions in and recommends Goldman Sachs Group and Nvidia. The Motley Fool has a disclosure policy.

Should You Buy Nvidia Stock Before the AI Chipmaker Reports Earnings on May 22? was originally published by The Motley Fool

Credit: Source link