Eoneren

By James Knightley

US inflation concerns linger

After a couple of benign core CPI prints, we have a modest upside surprise in the August report while surging gasoline prices boosted headline inflation. The Fed will still keep rates on hold in September, but it means officials will almost certainly keep one final hike in their official forecasts, even though we don’t think they will carry through with it.

3.7% Annual US inflation rate |

The August inflation data from the US shows headline CPI came in at 0.6% month-on-month with core (ex-food and energy) prices increasing 0.3% MoM as we suspected, but the market had been expecting 0.6% and 0.2%. This leaves the year-on-year rate at 3.7% for headline inflation (up from 3.2%) while annual core inflation slows to 4.3% from 4.7%. When measured to three decimal places, the 0.278% core print doesn’t look so bad. It is not a terrible miss, but markets will likely interpret it as showing the Fed can’t completely relax, especially with the potential for higher energy costs to be passed through to other components and potential strike action leading to worries about vehicle prices, given their heavy weighting within the CPI basket. So while September’s FOMC will be a non-event in itself – markets are barely pricing 2bp of a full 25bp rate hike – today’s report should ensure that officials keep one further hike in their dot plot forecast for the end of this year.

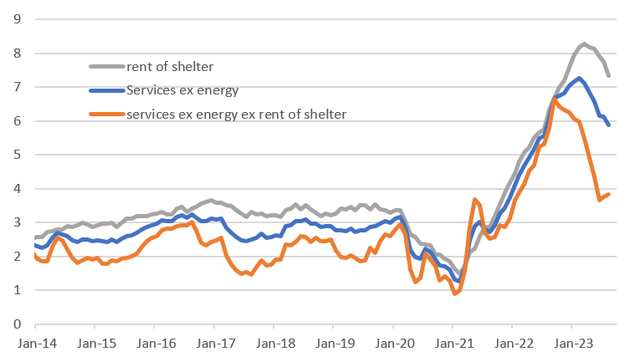

US service sector inflation measures (YoY%)

Macrobond, ING

The details show a 10% jump in gasoline was the primary driver of higher headline inflation, while airline fares and medical care rebounded after particularly soft July prints. Higher insurance costs were also an important upside driver, as we have suspected. Encouragingly, we are seeing recreation prices remain benign, while there is more evidence of housing inflation slowing, which we think will increasingly help to keep core prices in check over coming months. The core services ex-housing, which the Fed has been emphasising did tick higher to around 0.3% MoM and 3.8% YoY, but we see this as a slight blip on a slowing trend based on corporate pricing series such as within the NFIB report.

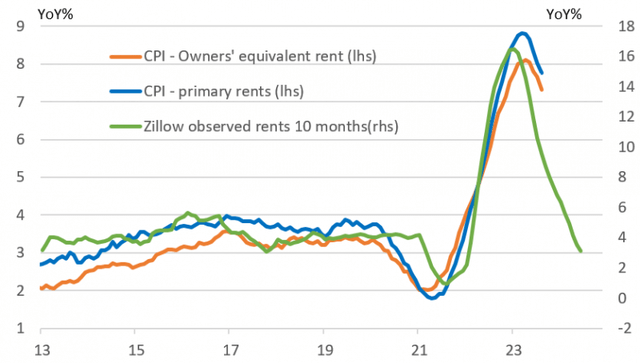

Housing CPI set to slow sharply (YoY%)

Macrobond, ING

Housing to slow core inflation to 3% in early 2024

We are currently penciling in a 0.3% MoM headline print for August CPI and 0.2% for core, which would bring the respective YoY rates down to 3.6% and 4%. For core, we think the rate of slowdown will remain strong given the housing rent dynamics, and look for annual core CPI to end the year at 3.3% with sub-3% achievable in the first quarter. Given this backdrop and the caution on the economic outlook that we have – exhaustion of pandemic-era savings, reduced credit availability, resumption of student loan repayments, rising delinquencies on credit cards and auto loans – we remain of the view that the Fed will not hike again in this cycle.

Fuel and strike action to keep markets nervous

There are obviously risks to this in both directions, and one of the most notable is the pickup in energy prices, but there is also potential strike action from the United Auto Workers union, which could see over 140,000 workers walk out from Ford, GM and Stellantis tomorrow. There is an argument that prolonged strike action would hurt supply and put upward pressure on vehicle prices – note new vehicles have a 4.3% weighting in CPI while used cars are at 2.8%. However, there does appear to be evidence of inventory building in recent months, so assuming a deal can be resolved within a couple of weeks it shouldn’t be too impactful on vehicle pricing. Nonetheless, it would also be painful for economic activity, especially in the Midwest. There would be knock-on effects for suppliers, and consumer spending would be hit hard, as household finances are already being squeezed.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Credit: Source link