Low inflation in the decades before the COVID-19 pandemic has often been attributed to globalization, so it would be natural to think the oppositethat less international trade, particularly with China, might lead to higher inflation. However, our latest Megatrends researchOpens in a new tab suggests that the impact of slowing globalization on inflation will be modest.

It’s a compelling narrative: The low inflation that we’ve seen for most of the past 30 years has been a consequence of lowered trade barriers thanks to the ratification of the North American Free Trade Agreement (NAFTA) in 1993 and China joining the World Trade Organization (WTO) in 2001. The ready availability of cheap imports from China has largely driven the narrative.

Given today’s geopolitical tensions and rising trade barriers, it’s understandable if some might think that globalization is in full reverse and that inflation might again rise to the alarming levels we saw post-pandemic or in the 1980s before globalization’s rapid rise.

Indeed, as we observed in 2021Opens in a new tab, the glory days of globalization are likely behind us. But the worst-case inflation scenario is not likely, particularly in the U.S. To understand why, we need to look back over decades.

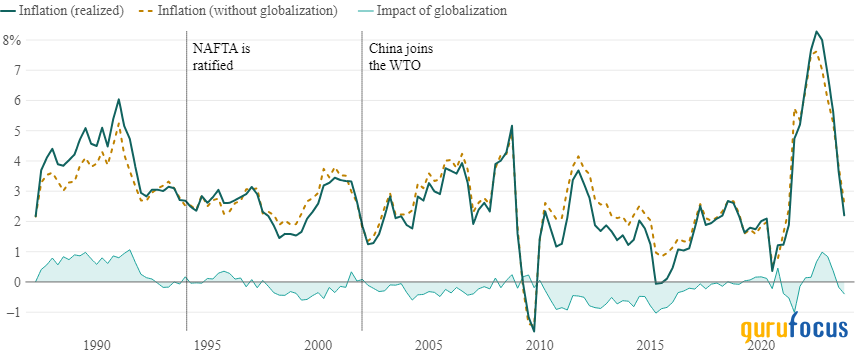

First, contrary to popular belief, globalization has had only a modest impact on inflation historically. The chart below illustrates this point.

Globalization has mildly lowered inflation, but slowbalization is not to be feared

Notes: Figure shows year-over-year inflation from March 31, 1987, through September 30, 2023, and hypothetical inflation, assuming that the globalization driver neither added to nor subtracted from inflation during that period. The shaded area represents the difference between the two lines. A negative value indicates that realized inflation was lower because of the impact of the changes in globalization. NAFTA stands for the North American Free Trade Agreement, and WTO stands for the World Trade Organization.

Source: Vanguard’s Megatrends paper, AI, Demographics, and the U.S. Economy: Quantifying the Coming Tug-of-WarOpens in a new tab, June 2024.

The chart covers 1987 through late 2023, a period that included cycles of both accelerating and slowing globalization. While globalization helped contain inflation in the 1990s and 2000s, the magnitude of its impact was modestfar less than that of monetary policy, according to our research. Even as globalization has slowed over the last 15 years (a trend we sometimes call slowbalization), its impact on inflation has, again, been very modest. The reason? It’s the makeup of the U.S. economy.

The U.S. economy is more self-sufficient than some may realize, with almost 90% of its goods and services produced within its bordersa much higher proportion compared with most other countries.

Take personal consumption as an example. By dollar value, only about 10% of goods and services consumed in the U.S. are imported. This may seem surprising if much of your wardrobe was made in China or Vietnam, but imported nondurable goods like clothing and footwear make up just around 4% of the consumption basket.

Almost 70% of total U.S. consumption is in serviceshealth care, education, housing, and so onthe vast majority of which takes place in the U.S. This is yet another reason why globalization during its heyday in the ’90s and 2000s had only a modest impact on inflation. And it’s why we expect slowbalization to have little impact on the U.S. economy and inflation going forward.

Notes: The figure shows the composition of U.S. personal consumption expenditures (PCE) by category (durable goods, nondurable goods, and services) and by source (imported or domestic). We used data as of 2019, as disruptions from COVID-19 and its aftermath in the early 2020s caused consumption patterns to deviate significantly from the long-term trend.

Source: Vanguard calculations based on data as of January 31, 2019, from the San Francisco Federal Reserve Bank.

Finally, we should not underestimate countries’ abilities to adapt. Since the 2008 global financial crisis, for instance, economies have been doing more nearshoring or friendshoringshifting trade to countries that are closer geographically or geopolitically to reduce the risk of shocks like supply-chain disruptions. As a result, the labels in your closet are more likely to say Made in Vietnam or Made in Mexico instead of the once-ubiquitous Made in China. Long before the latest trade disputes and pandemic-related supply shocks, these shifts have mitigated inflationary pressures stemming from any one region.

Given these forcesa domestic production base, service-based consumption, and adaptive strategies such as friendshoringwe believe the U.S. economy is well-positioned to adjust to shifting global trade dynamics. Globalization has slowed, and it may slow even further, but in the U.S., any resulting inflationary pressures should remain marginal.

Special thanks to Grant Feng, Vanguard senior economist, for his contributions to this commentary.

Note:

This article first appeared on GuruFocus.

Credit: Source link