Costco Wholesale (NASDAQ: COST) has captured the spotlight with its $15 special dividend, which will be paid to shareholders as of record at the close of business on Dec. 28. At first glance, a $15 per share special dividend seems like a lot. After all, that’s more than the stock price of some companies.

But at the time of this writing, Costco is a $661 stock. And even if we assume Costco slightly raises its ordinary dividend next year, it is still likely to pay less than $20 or even $19 per share in dividends — good for a forward yield under 3%.

Meanwhile, rival retailer Target (NYSE: TGT) has raised its dividend every year for over 50 years. It doesn’t pay special dividends. But its ordinary dividend alone has a forward yield of 3.2% — better than Costco without even relying on special dividends.

Here’s why Target is a better all-around buy than Costco right now — and a far better dividend stock for 2024.

Different approaches to dividend payments

Target is a traditional dividend-paying stock. It uses free cash flow (FCF) to support dividend growth. And even during downturns, when it doesn’t have the FCF to support dividends, it can lean on cash reserves or the strength of its balance sheet to pay dividends and fulfill its promise to investors.

Like Target, Costco pays an ordinary dividend. But it’s only $1.02 per share. Granted, Costco has raised its ordinary dividend substantially over the years (it has nearly doubled in the last five years). But even so, Costco’s yield from its ordinary dividend alone is just 0.6%.

Once Costco’s cash reaches an “excessive” level on its balance sheet, it tends to pay out a special dividend. This has happened four times over the past decade.

In the chart, you can see Costco’s four special dividends over the last decade, which coincide with a high point in the cash position, except for the special dividend in 2017 (which was more a result of intended growth).

Special dividends are overrated

On the surface, Costco’s strategy makes a lot of sense. When there’s room to pay a special dividend, it makes sense to reward your shareholders by directly putting money in their pockets. Special dividends have the “plop factor” that an ordinary divined simply can’t compete with in the same way.

But I’d argue that special dividends are overrated. The value of a quality dividend-paying company isn’t to hand out money to shareholders when times are good, but to continuously pay a growing quarterly payout no matter what the economy or the business is doing. That’s what makes a Dividend King like Target so valuable. It consistently raises its dividend even if the business faces challenges, which has certainly been the case lately.

In the case of Costco, the business has been doing extremely well, and the stock has been a juggernaut. So returning $6.7 billion to shareholders in the form of a special dividend isn’t really a good use of capital. A better use would be to reinvest in the business to support future growth.

Valuation matters

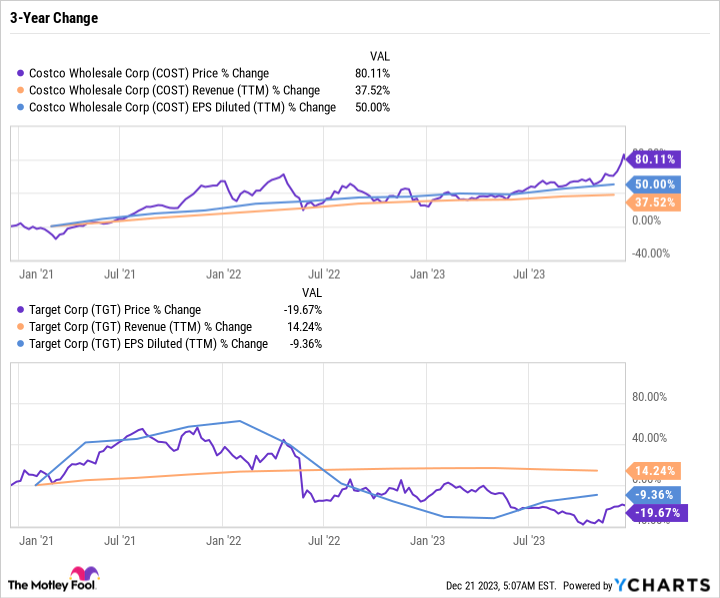

Costco’s stock price has outpaced the earnings and revenue growth.

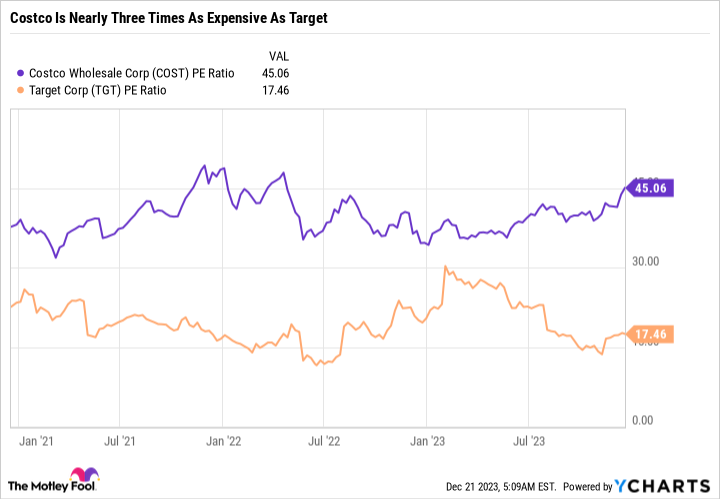

As you can see in the chart, Costco stock is up 80% over the last three years, while Target is down nearly 20%. Costco, as a business, has performed much better than Target, so the stock deserves to have outperformed. But to the extent that it has leaves room for danger. In fact, Costco’s price-to-earnings ratio is now 45.1 compared to just 17.5 for Target.

That’s an expensive price for a wholesale retailer. In investing, you typically don’t want to buy one stock over the other just because it is cheaper. Or as Warren Buffett famously said, “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

But in the case of Costco and Target, we have two great businesses where one is far cheaper than the other. Granted, Costco will probably continue growing faster than Target. But not to the point where it should trade at that much of a premium.

The case for Target

The (very abridged) version of why Target has lagged the market in recent years has to do with its mismanagement of consumer demand, poor inventory forecasting, and poor supply chain management. As a retailer, the worst thing you can do is over-order, and then have to discount items to move products off the shelves. That’s a recipe for margin compression, exactly what happened to Target.

The good news is the worst is over. Target has worked on a lot of its inventory headaches. It is now keeping a far leaner inventory, even during the holiday season. Target remains an excellent brand that has what it takes to grow over time, with its Target Circle rewards program, expansion of online ordering and curbside pickup, and engagement with its app.

The reliability of Target’s dividend, paired with its upside potential and inexpensive valuation, makes it a stock worth owning for the long term.

Don’t swoon over special dividends

Costco’s special dividend is basically a 2.2% boost to the stock price — which is what can happen any day in the market. Only it costs the company billions of dollars and isn’t the result of the market bidding up the company’s value.

I view dividends as an anchor of an investment thesis — something you can count on no matter what is happening in the market. They also serve as a useful financial planning tool for building passive income and retirement savings. On the other hand, capital gains, or the growth in value of a company, should result from the company’s improvements being recognized by the market.

A special dividend is like forced capital gains, if that makes sense. If I were a Costco shareholder, I would either want to see a higher ordinary dividend and the elimination of special dividends, or I would want to see Costco reinvest the money it would have spent on special dividends back into the business.

The stock is very expensive and will have to justify the valuation with earnings growth. That $6.7 billion could have gone a long way toward driving future growth. Instead, it will be distributed and taxed to investors as a one-time payment that means very little in the long run.

Should you invest $1,000 in Costco Wholesale right now?

Before you buy stock in Costco Wholesale, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Costco Wholesale wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

See the 10 stocks

*Stock Advisor returns as of December 18, 2023

Daniel Foelber has positions in Target and has the following options: long November 2024 $130 calls on Target and short November 2024 $135 calls on Target. The Motley Fool has positions in and recommends Costco Wholesale and Target. The Motley Fool has a disclosure policy.

Even With Its $15 Special Dividend, Costco Still Won’t Yield as Much as This Dividend King in 2024 was originally published by The Motley Fool

Credit: Source link