Josep Lago / AFP / Getty Images

Key Takeaways

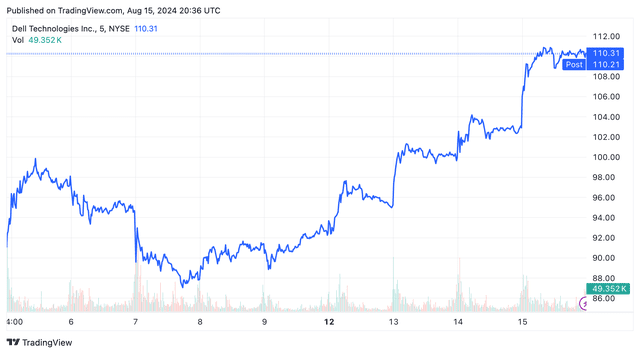

Dell Technologies shares jumped Thursday, adding to recent gains as analysts highlighted the legacy computing company’s opportunity to gain from surging demand for artificial intelligence (AI).

More than three-quarters of analysts tracked by Visible Alpha gave the stock a “buy” rating, with the consensus target price representing over 38% upside.

Investors will likely focus on the company’s margins and AI potential after the Dell’s fiscal first-quarter earnings report sent the stock tumbling.

Analysts said there could be long-term AI gains for Dell, though they noted that the company would need to show margin improvement.

Dell Technologies (DELL) shares jumped Thursday, adding to recent gains after J.P. Morgan analysts added the stock to an “Analyst Focus List” highlighting the legacy computing company’s opportunity for long-term artificial intelligence (AI) gains.

Shares finished 7% higher at $110.21 Thursday, contributing to the stock’s 25% jump over the past week and 44% gain since the start of the year. Over three-quarters of analysts tracked by Visible Alpha gave the stock a “buy” rating, with a consensus target price of $152.44, representing over 38% upside from Thursday’s closing price.

J.P. Morgan analysts, who lifted their price target for Dell stock to $160 from $155 on Thursday, said the stock could be poised for AI-related gains and offers an “attractive entry point from a valuation perspective after the recent pull-back.”

Dell shares had plummeted in May after the company’s first-quarter results showed a double-digit decline in operating income, despite strong demand for AI servers, raising worries about margin pressures and competition in the AI server market.

The analysts indicated that while some concerns about margins and competition persist, they said it’s still the “early innings” of the AI server market, with Dell positioned for AI-related revenue growth.

The company’s AI server offerings for enterprise customers could drive long-term, AI-driven growth, the analysts said, though they noted Dell will face pressure to show margin improvement.

Melius analysts said that the first half of the fiscal 2025 “needs to be the trough” for margins, with margin improvement in the second half.

Dell could tell investors it’s accelerating cost-cutting in an effort to improve margins, similar to legacy peers like Intel (INTC) and Cisco (CSCO). Dell is set to report second-quarter earnings on Aug. 29.

Read the original article on Investopedia.

Credit: Source link