Energy Transfer (NYSE: ET) is offering investors an ultra-high 8% distribution yield. Enterprise Products Partners (NYSE: EPD) has a yield of 7.2%. Although both hail from the midstream energy sector, they are not interchangeable investments. Here’s why lower-yielding Enterprise is worth buying hand over fist and most will probably be better off avoiding Energy Transfer.

The problem with Energy Transfer

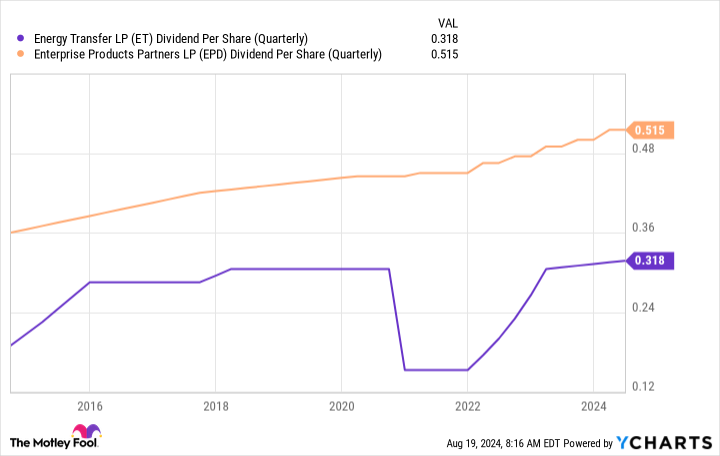

When energy prices plunged early in the coronavirus pandemic, Energy Transfer cut its distribution 50%. That 2020 distribution cut was, perhaps, justified by the uncertainty the world faced at the time, but it certainly was not the distribution outcome the investors were hoping for. And while the master limited partnership’s (MLP) distribution has started to rise again and is actually higher than it was before the cut, investors that care about income consistency shouldn’t ignore the choice that management made in 2020. It opens up the very real risk that the next energy industry downturn will lead to the same outcome.

Still, a distribution cut in the face of energy industry adversity is understandable. What’s harder to explain with Energy Transfer is the failed 2016 agreement to buy Williams Companies. Energy Transfer initiated the deal, but an energy downturn resulted in the MLP getting cold feet. Energy Transfer then worked to scuttle the deal, claiming that consummating it would require taking on too much debt, cutting the dividend, or both. The effort to get out of the agreement included issuing convertible securities, which is where the real problem comes in.

The CEO bought a large portion of the convertible securities at the time. The security would have effectively protected the CEO from the impact of a dividend cut if the deal went through as planned while leaving unitholders to feel the full brunt of a cut. It was a complicated affair, but that’s a top-level, and unsettling, view. That CEO, Kelcy Warren, is now “just” the chairman of the board, so there’s still good reason to be worried about what happened nearly a decade ago.

Overall, if you are looking for a reliable income stream, Energy Transfer is probably not the place to look.

Enterprise Products Partners continues to put unitholders first

Enterprise Products Partners is another large North American midstream MLP. But it doesn’t have the same distribution negatives hanging over it. For starters, it’s increased its distribution annually for 26 consecutive years. Secondly, it has managed to make regular acquisitions without resorting to aggressive tactics in an effort to end a transaction before it has been completed.

But what’s interesting here is that Enterprise isn’t immune to the impact of energy downturns. While its business is largely fee-based, 2016 was a relatively tough year, and so was 2020. The business kept on chugging along despite temporary weakness, and the distribution was raised despite that weakness. A key factor there is the conservative nature of Enterprise’s management, with the distribution backed by an investment-grade balance sheet and a strong distribution coverage ratio (currently distributable cash flow covers the distribution by 1.7 times).

There’s also a long history of unitholder-friendly decisions to consider. For example, in 2002 Enterprise reduced its incentive distribution rights by 50%, freeing up more cash to pay unitholders at the expense of the general partner. In 2007, management slowed distribution growth so it could invest more heavily in business expansion to increase long-term returns. In 2011, the MLP eliminated incentive distributions and bought its general partner, effectively becoming a self-governing entity. And in 2018 Enterprise worked to become a self-funding business so it wouldn’t have to issue as many dilutive units in the future.

Stick to the one you can trust

It isn’t an exciting investment, but Enterprise has clearly looked out for unitholders in a way that Energy Transfer hasn’t. If you are trying to live off of the income your portfolio generates, reliable Enterprise, despite a slightly lower yield, is likely to be the better option than Energy Transfer over the long haul.

Should you invest $1,000 in Energy Transfer right now?

Before you buy stock in Energy Transfer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Energy Transfer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $792,725!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of August 26, 2024

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.

1 Ultra-High-Yield Energy Stock to Buy Hand Over Fist and 1 to Avoid was originally published by The Motley Fool

Credit: Source link