Most investors interested in Energy Transfer (NYSE: ET) are attracted to its high yield, which currently sits around 7.9%. The company currently pays a $0.32 quarterly distribution and is looking to increase that by between 3% to 5% a year moving forward.

That is attractive in and of itself, but I also think the pipeline operator’s stock could nearly double over the next five years.

This would happen through a combination of growth projects, as well as modest multiple expansion, which is when investors assign a higher valuation metric to a stock.

Let’s look at why I think Energy Transfer’s stock can more than double in the next five years.

Growth opportunities

Energy Transfer is one of the largest midstream companies in the U.S., with an expansive integrated system that traverses the country. It’s involved in nearly all aspects of the midstream sector, transporting, storing, and processing various hydrocarbons across its systems. The size and breadth of its systems give it many expansion project opportunities.

This year, the company plans to spend between $3 billion to $3.2 billion in growth capital expenditures (capex) on new projects. Moving forward, spending between $2.5 billion to $3.5 billion in growth capex a year would allow it to pay its distribution while having money left over from its cash flow to pay down debt and/or buy back stock.

Given this, and the early opportunities that Energy Transfer is seeing in power generation due to increased power needs from data centers stemming from the rise in artificial intelligence (AI), it’s probably safe to say that the company could spend about $3 billion in growth capex a year over the next five years.

Most companies in the midstream space are looking for at least 8x build multiples on new projects. This means that the projects would pay for themselves in about eight years. For example, a $100 million project with an 8x multiple would generate an average return of $12.5 million in EBITDA (earnings before interest, taxes, depreciation, and amortization) a year.

Based on that type of return on growth projects, Energy Transfer should be about able to see its adjusted EBITDA rise from $15.5 billion in 2024 to about $17.4 billion in 2029 if it continues to spend $3 billion a year on growth projects.

Multiple expansion opportunities

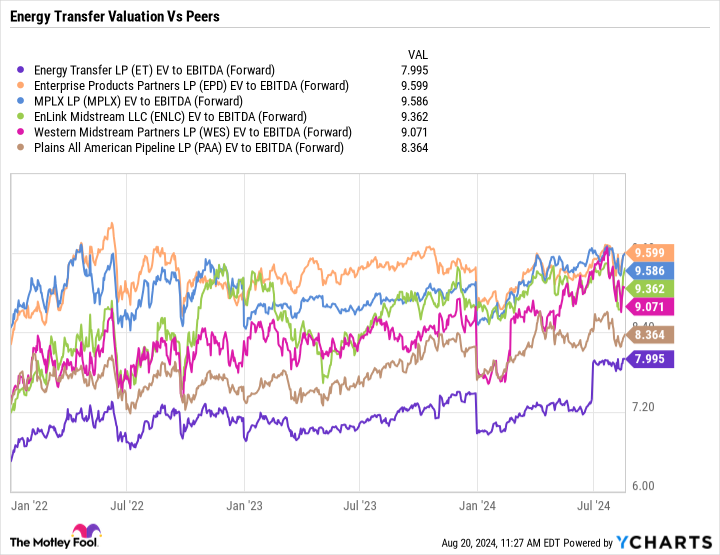

From a valuation perspective, Energy Transfer is the cheapest stock among its master limited partnership (MLP) midstream peers, trading at 8x on a forward enterprise value-to-adjusted EBITDA basis. This metric takes into consideration a company’s net debt while taking out non-cash items and is the most widely used way to value midstream companies. At the same time, it trades at a much lower valuation than it has historically.

MLP midstream stocks averaged a 13.7x EV/EBITDA multiple between 2011 and 2016, so the industry as a whole has seen its multiple come down. However, with demand for natural gas on the rise due to AI and electric vehicle demand waning, the transition to renewables looks like it may take much longer than expected. If this is the case, these stocks should be able to command a higher multiple than they currently do, as this reduces the fear that hydrocarbon demand will start to materially decline in the years ahead.

How Energy Transfer stock nearly doubles

If Energy Transfer grows its EBITDA as expected, the stock could reach $30 in 2029 if it can command a 10x EV/EBITDA multiple. That is up from the 8x forward and 8.7x trailing multiple it currently commands, but it’s still well below where the MLP midstream space has traded in the past.

| 2024 | 2025 | 2026 | 2027 | 2028 | 2029 |

|---|---|---|---|---|---|---|

Adjusted EBITDA | $15.5 billion | $15.88 billion | $16.25 billion | $16.63 billion | $17.0 billion | $17.38 billion |

Price at 8x multiple |

| $17 | $18 | $19 | $20 | $21 |

Price at 9x multiple |

| $21.50 | $22.50 | $23.50 | $24.50 | $25.50 |

Price at 10x multiple |

| $26 | $27 | $28 | $29 | $30 |

* Enterprise value is based on 3.42 billion shares outstanding, $57.6 billion in debt, $3.9 billion in preferred equity, $3.9 billion in investments in unconsolidated affiliates and cash, and $11.6 billion in minority interest.

However, Energy Transfer and several other midstream companies appear to be very well positioned to be stealth AI winners due to increasing natural gas power demand. Power companies and data centers have already been approaching Energy Transfer about natural gas transmission projects, and there could be a natural gas volume boom coming. Given this growth opportunity, together with the company’s strengthened balance sheet and consistent distribution growth, I could see Energy Transfer’s multiple expand modestly over the next five years and the stock nearly doubling.

However, even if its multiple doesn’t expand, investors can still get a very solid return on their investment through a combination of distributions (currently $0.32 per unit a quarter) and more modest price appreciation. With no multiple expansion and over $7 in distributions between now and the end of 2029 (assuming a 4% increase a year), the stock would still generate an over 75% return during that stretch.

Should you invest $1,000 in Energy Transfer right now?

Before you buy stock in Energy Transfer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Energy Transfer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $792,725!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of August 22, 2024

Geoffrey Seiler has positions in Energy Transfer, Enterprise Products Partners, and Western Midstream Partners. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.

Prediction: Energy Transfer Stock Will Nearly Double in 5 Years was originally published by The Motley Fool

Credit: Source link