The one thing that you can be certain of on Wall Street is that bull markets will eventually be followed by bear markets (and vice versa). It’s kind of like a pendulum, though, with extreme highs and extreme lows being driven by the emotional swings of investors.

I don’t play that game and neither should you. Which is why I own high-yield Enbridge (NYSE: ENB). Here’s why you might want to buy this stock too.

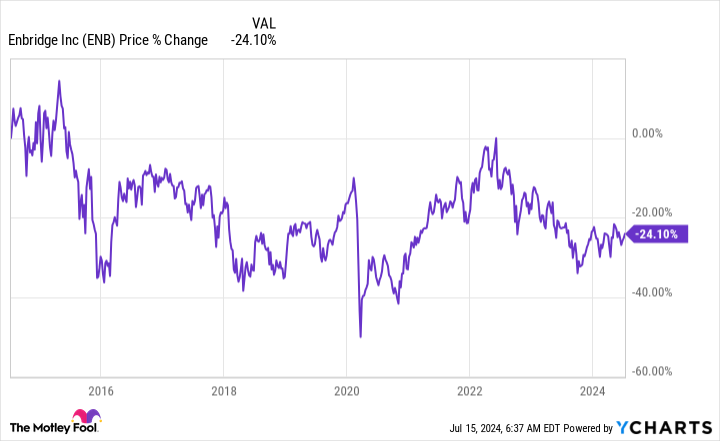

What does Enbridge’s return look like?

If you look at Enbridge’s stock price you probably won’t be impressed. The stock is down around 25% over the past decade. However, that’s pushed the dividend yield up to 7.4%. That gets you nearly three-quarters of the way to the average 10% return that most investors expect from the stock market.

Now add in dividend growth, which has been in the low single digits of late. The last increase, for example, was just over 3%. That pushes the return to 10%, given that stocks normally increase after a dividend hike to keep the dividend yield constant. Sure, the yield is going to make up the lion’s share of that return, but if you are looking to live off of the income your portfolio generates that won’t be a big deal.

If your outlook is longer and you don’t need the income, meanwhile, you can just reinvest those dividends and allow that big yield to compound over time. That’s what I’m doing, as I work toward retirement when I will switch off dividend reinvestment and start to use the income stream. But until that point, I’m expecting to lock in near-market-like returns with just the dividend. I’m sleeping very well at night even with the market near all-time highs, at least partly thanks to Enbridge’s 29-year streak of annual dividend increases.

There’s more to the Enbridge story than yield

That said, I don’t just buy a stock because of its yield. The company’s business is just as important and Enbridge has a really good story to tell on that front. For starters, it has an investment-grade-rated balance sheet and the distributable-cash-flow payout ratio is comfortably within the company’s target payout range of 60% to 70%. Basically, the dividend looks like it is on solid financial ground.

Then there’s the actual business. Enbridge operates in the midstream sector, with the bulk of its revenue derived from oil and natural gas energy infrastructure. It charges fees for the use of what are basically irreplaceable and vital energy assets. That means that its cash flows tend to be fairly consistent over time in this segment. On top of that, the company owns regulated natural gas utilities, which also produce highly predictable cash flows. Then there’s the small but growing investment in clean energy, driven by reliable contract-derived cash flows.

There are actually two takeaways here. First, everything Enbridge owns produces reliable cash flows. That’s something vital to the company’s ethos because it knows that the dividend is important to investors. Second, the company is slowly transitioning away from oil and more toward natural gas. The most recent move was to buy three natural gas utilities from Dominion Energy, which will drop oil to around 50% of the business and increase natural gas to 47% (the rest in renewable power).

So, not only am I collecting a big and growing yield, but I also own a company that is cognizant of the world’s transition toward clean energy. And it is working to ensure it is shifting along with the world. I worry about every stock I own, but Enbridge is one that I’m comfortable only checking on quarterly. And I don’t really worry about the market’s gyrations when I check in, just that the company continues to execute at a high level on its long-term plans.

The market is important, but it’s not the only important thing

While my wealth depends on the market to a large degree, I don’t look at the stock price of my investments nearly as closely as I look at the businesses the stocks I own represent. So long as companies like Enbridge keep doing what they say they will do I don’t worry too much about the market’s often fickle pricing.

It is hard to get too upset by a huge 7%-plus yield backed by a strong company and a growing dividend. In fact, a stock price decline, given my dividend reinvestment, is really just an opportunity for me to compound my Enbridge investment at even better prices.

Should you invest $1,000 in Enbridge right now?

Before you buy stock in Enbridge, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Enbridge wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $774,281!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of July 15, 2024

Reuben Gregg Brewer has positions in Dominion Energy and Enbridge. The Motley Fool has positions in and recommends Enbridge. The Motley Fool recommends Dominion Energy. The Motley Fool has a disclosure policy.

Is the Stock Market Going to Crash? I Don’t Know. That’s Why I Own This High-Yield Stock. was originally published by The Motley Fool

Credit: Source link