It’s a new month and another great opportunity to add dividend income to your portfolio. Even as the S&P 500 sits near all-time highs, there are always deals in the market. This month, the energy sector strikes me as particularly appealing.

Let’s face it: High-yield dividend stocks are often red flags. Trustworthy stocks that yield 6%, 7%, and 8% are difficult to come by. High yields frequently mean the market has sniffed out trouble and is demanding more income to compensate for those risks.

But there are exceptions. Two high-yield pipeline stocks jumped out as table-pounding buys for July. Here is why you can trust them to deliver the goods.

A dividend gusher at a fair price

Energy Transfer (NYSE: ET) is crucial to North America’s energy picture. The company operates an extensive network of storage facilities and over 125,000 miles of pipelines that transport oil, natural gas, and refined products throughout the country.

It connects crucial exploration regions, such as the Permian Basin, to ports that send commodities to over 80 countries. Pipelines are like toll roads: They make money based on the volume of materials flowing through their pipes.

Roughly 90% of Energy Transfer’s earnings come from fee-based contracts, so the business is more predictable than upstream oil and gas companies that depend on commodity prices.

Most companies pay corporate income tax before paying dividends to their shareholders. Then, shareholders must pay taxes on their dividends, which essentially means the company’s profits are taxed twice.

Energy Transfer is a master limited partnership (MLP), a business structure that doesn’t pay corporate income tax. MLPs are pass-through entities; they distribute their profits (MLP for dividend) to unitholders (MLP for shareholder), who pay taxes according to the number of units they own and their individual income tax rate. That makes Energy Transfer more tax efficient, while the larger distributions help compensate unitholders for carrying the tax burden.

Energy Transfer’s distribution yields 7.8% and is sustainable because it only costs just over half its cash flow.

It’s become more challenging to call the stock cheap after it has appreciated nearly 30% over the past year. Yet, despite the run, the stock’s valuation is only slightly above its long-term average. Management is targeting 3% to 5% annual distribution growth, which signals that the business will grow similarly.

A mid-single-digit multiple on its operating cash flow is reasonable for a company growing at that pace. Toss in the nearly 8% yield, and investors could see annual total returns between 10% and 13%. That makes Energy Transfer a potential buy.

This pipeline giant is on sale.

Enbridge (NYSE: ENB) is equally important to North America’s energy industry. The company’s assets transfer oil, gas, and other products throughout Canada and the United States. It helps connect the Canadian oil sands to ports throughout the continent.

Enbridge’s business also includes natural gas utilities and renewable energy production. That diversification has helped it endure hard times and continue putting money in shareholder pockets. The company has raised its dividend for 28 consecutive years.

While not a master limited partnership, Enbridge still offers a generous dividend. The stock yields 7.5% at the current share price. The company’s ability to raise its dividend through COVID and the financial crisis in 2008-2009 should give investors confidence in the payout.

Enbridge also has an investment-grade credit rating and a manageable 66% dividend payout ratio, so the dividend is fundamentally rock-solid.

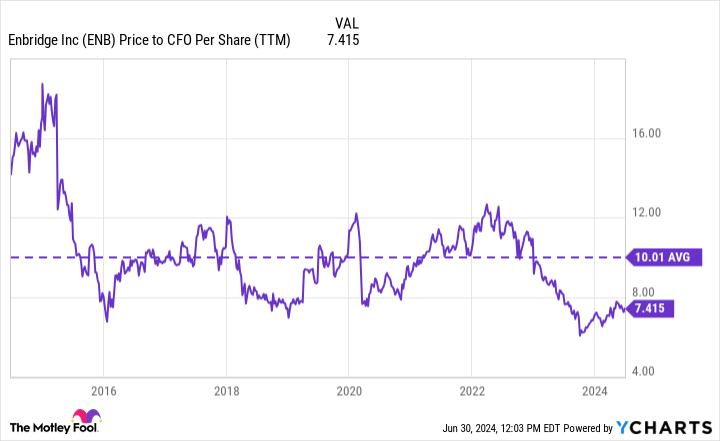

Enbridge stock hasn’t followed Energy Transfer higher; it’s down slightly over the past 12 months. The good news is that shares remain on sale. Enbridge has traded at an average of 10 times its operating cash flow over the past decade. It trades well below that today at 7.4 times.

North America figures to remain a key energy exporter, which should keep enough flowing through Enbridge’s pipes to drive long-term growth. Analysts believe the company’s distributable cash flow will grow by over 6% next year. It seems likely the share price will eventually follow. Investors can collect a hefty dividend in the meantime.

Should you invest $1,000 in Energy Transfer right now?

Before you buy stock in Energy Transfer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Energy Transfer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $751,670!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of July 2, 2024

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Enbridge. The Motley Fool has a disclosure policy.

2 Dividend Stocks to Buy Hand Over Fist in July was originally published by The Motley Fool

Credit: Source link