Nvidia (NASDAQ: NVDA) is the hottest company on the planet right now — and it’s not even close. Indeed, the chip specialist is at the heart of the artificial intelligence (AI) revolution, and investors can’t seem to get enough.

Just days ago, Nvidia’s market cap rocketed past $3.3 trillion and briefly overtook Microsoft as the most valuable company in the world. With shares up roughly 150% so far this year, could Nvidia stock possibly keep going?

One Wall Street analyst thinks so. Hans Mosesmann of Rosenblatt Securities just raised his price target for Nvidia from $140 to $200. As of market close on June 21, a $200 price target implies 59% upside to Nvidia’s current price. To put this into perspective, Mosesmann is calling for Nvidia’s market cap to reach $5 trillion.

Let’s break down Nvidia’s rapid rise to become one of the world’s largest companies, and assess why now could be as good a time as ever to join the party.

Nvidia’s path to $3 trillion

The chart shows the change in Nvidia’s market cap so far in 2024. Roughly six months into the year, the company has added nearly $2 trillion in value. Not only is this unprecedented, but it’s arguably warranted.

For Nvidia’s first quarter of fiscal 2025 (ended April 30), the company reported a 262% increase year over year in revenue. Nvidia’s largest source of business comes from data centers, which grew 427% year over year during the first quarter — reaching $22.6 billion.

What’s even better is that Nvidia isn’t just witnessing outsize revenue acceleration. The company’s gross margin expanded nearly 14 basis points year over year during the first quarter. The combination of increasing revenue and rising profit margins has fueled Nvidia’s operating income and cash flow.

For the quarter ended April 30, Nvidia’s free cash flow grew 465% year over year to $14.9 billion.

Clearly, the company is not struggling to generate growth in any part of its business. Let’s take a look at how Nvidia is reinvesting its profits, and what it could spell for the company’s future.

Could Nvidia stock keeping climbing higher?

Today, Nvidia is primarily a data center and chip business. While I suspect both of these services will remain important for Nvidia, there are some important details to discuss.

Namely, Nvidia is far from the only company competing in data center services or the semiconductor space. Companies including Vertiv have also been major beneficiaries of the AI boom, and have seen their own data center businesses take off. Furthermore, Nvidia faces some stiff competition from Intel and Advanced Micro Devices in the graphics processing units (GPU) arena.

Where Nvidia might have an edge is when it comes to innovation. Right now, Nvidia’s most popular GPUs are its H100 and A100 chips. However, the company recently released a new line of semiconductors called Blackwell.

When speaking about Blackwell during Nvidia’s most recent earnings call, management said, “Demand for H200 and Blackwell is well ahead of supply, and we expect demand may exceed supply well into next year.”

Although this is encouraging, Nvidia is not resting on its laurels. Earlier this month, Nvidia’s management previewed its next line of chips, dubbed Rubin. The pace at which Nvidia is innovating is undeniably impressive.

Essentially, the company has already created a success to its already popular H100 and A100 line, and then swiftly doubled down in research and development efforts to build an even more superior product to Blackwell.

If that weren’t enough to impress you, consider that Nvidia is also investing in the area of AI-powered robotics, as well as enterprise software. Earlier this year the company invested in Figure AI, a humanoid robot that is competing with Tesla‘s Optimus.

Furthermore, Nvidia is also an investor in Databricks — one of the world’s most valuable software start-ups.

Is now a good time to invest in Nvidia stock?

When it comes to investing in Nvidia, there are two schools of thought. First, one could argue that the stock has risen too dramatically, too quickly. Behind this rationale, investors would argue that the potential of Blackwell, Rubin, and some of Nvidia’s other initiatives in software and robotics are already priced into the stock.

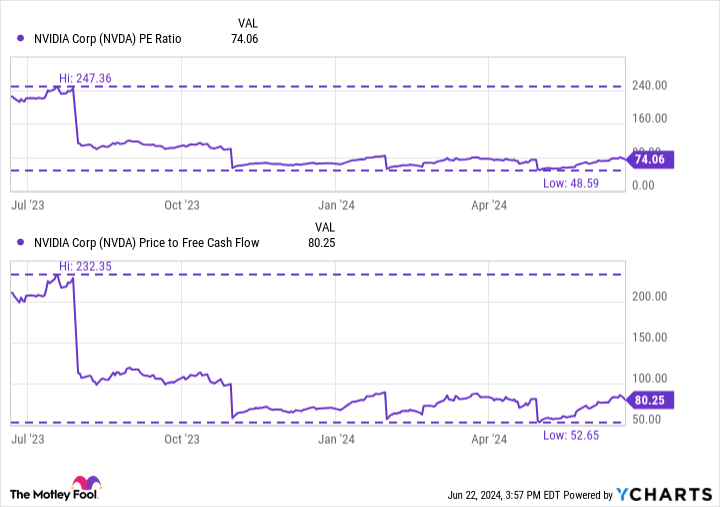

On the other hand, a closer look at valuation multiples might suggest otherwise.

The charts reflect Nvidia’s price-to-earnings (P/E) and price-to-free cash flow multiples over the last year. Notice anything interesting?

Despite Nvidia’s surging share price, its profitability valuation multiples are actually lower now than they were a year ago. This happens because Nvidia’s earnings and cash flow are accelerating at faster rates compared to the rise in the value of the company. This means that shares of Nvidia are technically less expensive today than they were this time last year.

Considering all the projects Nvidia is touching, I’m hard-pressed to see the company falling behind in the AI race. Moreover, considering shares look reasonably valued at the moment, I think Nvidia is a no-brainer — whether it reaches a $5 trillion milestone or not.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $774,526!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of June 24, 2024

Adam Spatacco has positions in Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Advanced Micro Devices, Microsoft, Nvidia, and Tesla. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short August 2024 $35 calls on Intel, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

A Once-in-a-Generation Investment Opportunity: Nvidia Is Now Worth Over $3 Trillion, and 1 Wall Street Analyst Thinks The Stock Can Soar Another 59% was originally published by The Motley Fool

Credit: Source link