Cathie Wood has developed a strong following among investors for anticipating digital trends that accelerated early in the pandemic. The Ark Invest chief often takes a contrarian position on stocks, and the exchange-traded funds (ETFs) she manages tend to focus on companies that are creating and spreading disruptive technology.

She has been a fan of e-commerce platform operator Shopify (NYSE: SHOP) for a long time, but over the past year, she has been cutting her ETFs’ stakes in it. However, Shopify’s stock price plunged this month, and Ark Invest is scooping up shares again. Should you follow her lead?

Why is Shopify stock dropping?

Shopify announced its first-quarter results on May 8. Investors weren’t happy, to say the least. The stock is down 26% since the earnings release.

There wasn’t anything terrible in the report. Revenue increased 23% year over year, and management’s outlook for second-quarter sales is in line with Wall Street’s expectations, even though it’s calling for a slowdown in top-line growth. In Q1, operating income turned positive at $86 million after a $193 million loss in the prior-year period, and adjusted earnings per share came in at $0.20, beating Wall Street’s consensus expectation of $0.17.

One area that stood out was gross margin guidance. Shopify’s gross margin expanded from 47.5% in Q1 2023 to 51.4% last quarter, but management expects it to tighten by about 50 basis points to around 50.9% in the second quarter.

So what gives? Most likely, there is intense pressure on Shopify to perform, given its sky-high valuation. Gone are the days when investors were comfortable with paying astronomical valuations for growth stocks. In this market, investors are being much more careful about valuations. Shopify stock was trading at a price-to-sales ratio of 16 earlier this year, and it was still above 13 before the Q1 report. Those are high sales multiples, and it didn’t take much being off in the quarterly report to erode the market’s willingness to keep supporting them.

Plus, Spotify is still not profitable on a GAAP (generally accepted accounting principles) basis. A rich valuation combined with less-than-stellar results is a fair setup for a fall.

Why is Wood getting enthusiastic again?

Shopify is still reliable for double-digit percentage sales growth every quarter, and its profitability is improving steadily. Free cash flow tripled year over year to $232 million in Q1. Among the things that are dragging on its profitability now is the sale of its logistics business, which is still reflected in its financials. However, that sale was the right move to get the company back on track, and the positive results from it will begin to show up soon.

Management sees a huge market opportunity for the company, which will allow it to keep up its growth. That should lead to profitability at scale — something it has already achieved for a time early in the pandemic, when its business accelerated sharply. It has a roadmap to get there, and a whole bunch of growth drivers to help.

One of those is its move into physical commerce. Offline gross merchandise volume increased 32% year over year in the first quarter, outpacing overall growth of 23%. Another is business-to-business commerce — that segment experienced a 130% increase in gross merchandise volume in Q1.

In general, management sees tremendous opportunities for the company from a network effect at scale. As it grows, its clients sign up for more services and demonstrate greater payment volume. Its gross payments volume metric represents the share of sales on its platform processed through Shopify Payments, and that accounted for 60% of sales in Q1, up from 56% a year prior. Merchant solutions revenue, mostly associated with gross payments volume, accounted for 74% of the company’s total revenue in the quarter.

Is Shopify stock really a bargain?

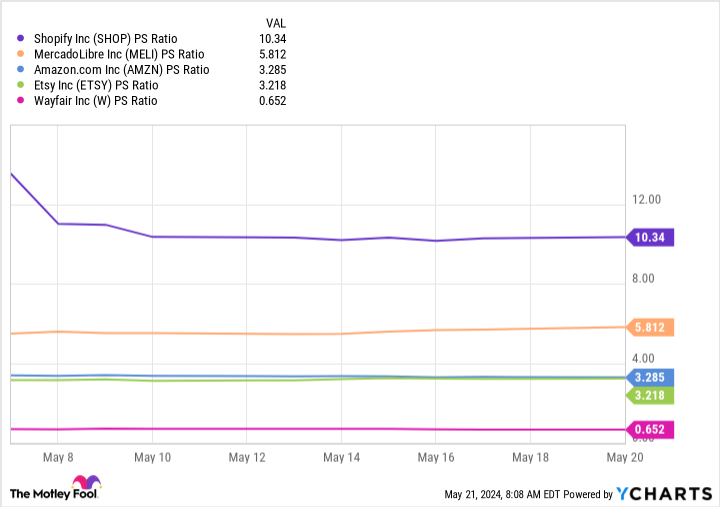

Shopify now trades at a price-to-sales ratio of about 10, a valuation that still has a lot of upbeat expectations baked into it. Compare it to other e-commerce stocks like Amazon, Wayfair, MercadoLibre, and Etsy. Even after that sharp price drop, Shopify still looks like an expensive market darling.

The stakes are high for Shopify, and the company has little margin for error. Even Wood’s position in it is much smaller than 13 months ago. In sum, there are things to be excited about here, but the stock is not a buy at this price.

Should you invest $1,000 in Shopify right now?

Before you buy stock in Shopify, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Shopify wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $652,342!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of May 13, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Jennifer Saibil has positions in MercadoLibre. The Motley Fool has positions in and recommends Amazon, Etsy, MercadoLibre, and Shopify. The Motley Fool recommends Wayfair. The Motley Fool has a disclosure policy.

Cathie Wood Goes Bargain Hunting: 1 Stock She Just Bought was originally published by The Motley Fool

Credit: Source link