There are loads of ways to generate passive income. One of the best ways to supplement portfolio growth is to seek out dividend stocks.

But when it comes to dividend income, did you know that some opportunities may be more reliable than others?

Let’s break down five companies that are established dividend payers, and assess why holding each of these stocks over a long-term time horizon can lead to massive gains for your portfolio.

1. Hercules Capital

Hercules Capital (NYSE: HTGC) is a business development company (BDC). BDCs are a reliable source of dividend income because these companies are required to pay out at least 90% of their taxable income to investors each year.

While there are many types of BDCs, Hercules primarily focuses on high-yield loans to start-ups in the technology, life sciences, and renewable energy industries. Although start-ups can be risky, Hercules has demonstrated that it employs robust due diligence processes before making an investment. Over the years, the company has worked with notable businesses including Impossible Foods, Enphase Energy, and Lyft.

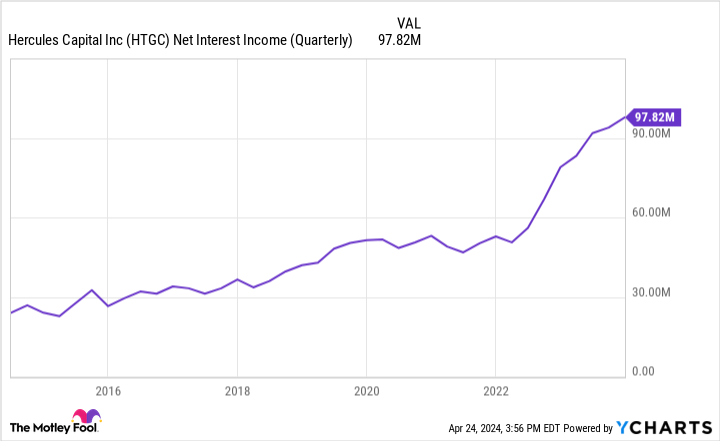

The company’s consistent rise in net interest income undermines Hercules’ strong performance and its proven ability to reward shareholders.

Over the last 10 years, Hercules stock has a total return of 275%. Not only does this emphasize the importance of reinvesting dividends, but it also highlights that Hercules has been a lucrative investment over the long run.

With its juicy dividend yield of 10.4%, now could be a great opportunity to scoop up shares in Hercules stock.

2. Ares Capital

Another prominent BDC is Ares Capital (NASDAQ: ARCC). Unlike Hercules, Ares doesn’t typically work with high-profile tech companies that have raised funds from venture capital firms.

Rather, many of the companies in Ares’ portfolio are lower middle market businesses that go overlooked by investment banks or private equity investors.

Moreover, while Hercules specializes in basic debt instruments such as term loans or revolvers (think a corporate line of credit), Ares offers more sophisticated products — including leveraged buyouts (LBOs).

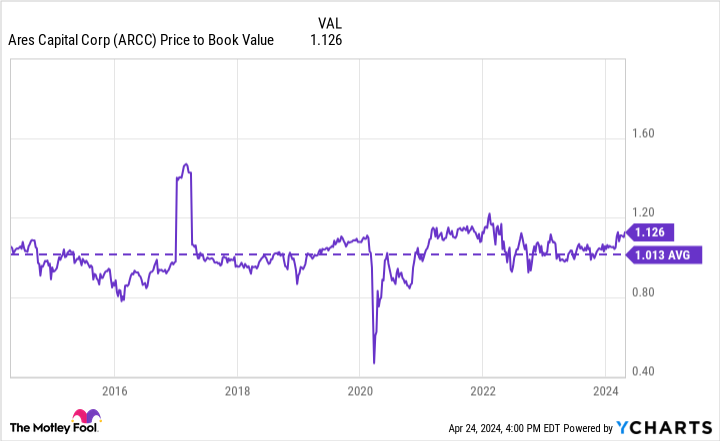

At a price-to-book (P/B) ratio of just 1.1, Ares stock is trading essentially in line with its 10-year average. Considering the company’s total return has outperformed the S&P 500 over the last three- and five-year periods, I think now looks like a great time to buy some shares in Ares at a 9.3% yield and prepare to hold for the long-run.

3. Rithm Capital

Real estate investment trusts (REITs) are another great source of dividend income.

Rithm Capital (NYSE: RITM) is a REIT that specializes in financial services including loan origination, as well as commercial real estate and single-family rentals.

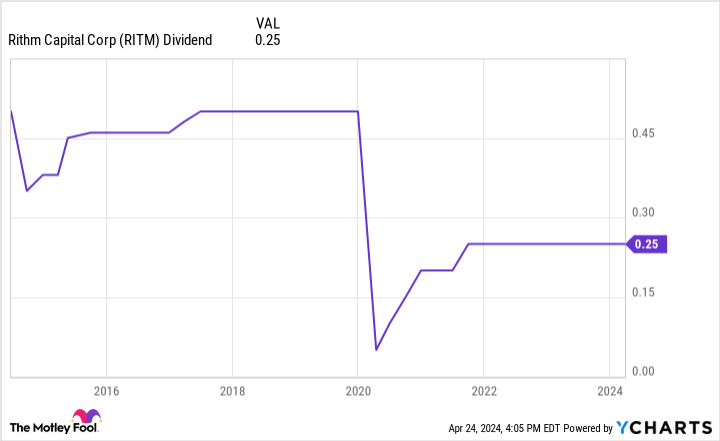

One drawback that investors may see with Rithm is the company’s exposure to broader themes in real estate. Indeed, lingering inflation and high borrowing costs have affected consumers, businesses, and even home owners or renters. For me, the biggest mark is what Federal Reserve will decide to do regarding interest rates this year.

The chart below illustrates how these macroeconomic variables can impact Rithm’s business specifically. While the dividend is lower than it was in years past, I think the bigger idea is that holding for the long-term could be a good decision.

With the stock trading at less than $11 per share, now could be a tempting time to consider buying some shares at a 9.2% yield and the possibility of a rising dividend depending on the broader macro environment.

4. Energy Transfer

Outside of financial services, investors can find lucrative sources of dividend income from the energy sector. Energy Transfer (NYSE: ET) is a master limited partnership (MLP) operating in the natural gas industry.

MLPs have an interesting operating structure because these entities pass income and losses along to their investors. This can be an attractive feature for income investors.

MLPs also tend to distribute excess profits to limited partners (LPs). These payments are known as distributions and are similar to dividends.

One risk worth pointing out is that the energy sector can experience more pronounced volatility than other sectors. For example, current geopolitical conditions in Europe and the Middle East have greatly affected legislative policy surrounding the energy industry.

However, Energy Transfer is more insulated from these risks. A common theme among MLP’s is that these companies often enter long-term fixed fee contracts with their customers. In essence, this provides Energy Transfer with far less exposure to commodity-based risk when compared to other types of energy businesses.

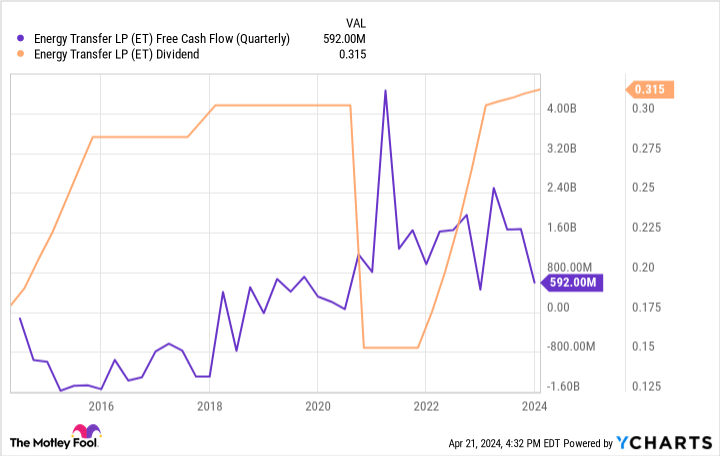

The chart below illustrates Energy Transfer’s free cash flow over the last 10 years. While it’s improved dramatically over the last decade, trends in more recent years do show that even steadier businesses such as MLP’s can experience some level of volatility.

Nevertheless, Energy Transfer has made it a point to raise its distributions to historically high levels. I think this showcases management’s decisions to prioritize shareholders.

5. Enterprise Products Partners

The last company on my list is midstream energy specialist Enterprise Products Partners (NYSE: EPD).

Earlier this year, Enterprise Products Partners announced that it was acquiring joint venture interests from Western Midstream Partners. In early April, the company also announced that it was breaking ground on a series of new natural gas plants in the Permian Basin. Among all of its projects, Enterprise Products Partners has roughly $6.5 billion of approved new business currently under construction.

What I like most about Enterprise Products Partners is the company’s ability to navigate challenging economic periods while still rewarding shareholders. Over the last 15 years, the economy has witnessed the 2008-2009 Great Recession, prolonged cratering oil prices between 2014 and 2016, and most recently the COVID-19 pandemic.

During, this time, the company’s adjusted cash flow from operations (CFFO) has rise from $1.29 per unit at the end of 2009, to $3.70 by the end of 2023. Given the company’s 7.1% yield and strong performance in the long-run, now could be an interesting time to consider buying some shares.

Should you invest $1,000 in Ares Capital right now?

Before you buy stock in Ares Capital, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Ares Capital wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $537,557!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of April 22, 2024

Adam Spatacco has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Enphase Energy. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.

Looking For Passive Income? Here Are 5 Ultra-High-Yield Dividend Stocks to Buy and Hold For a Decade was originally published by The Motley Fool

Credit: Source link