Stocks aren’t lottery tickets or get-rich-quick opportunities, but there are some promising investment opportunities in the market that can be transformational forces within a portfolio. If you have enough risk tolerance, you should consider a few stocks that are in the earlier, less certain stages of their lifecycle but also have enormous potential and clear competitive advantages. Sometimes, these businesses can blossom into cash flow machines at a much larger scale in the future.

These three stocks below have a lot of potential room for growth ahead — if all goes right for them — and getting in early could fuel returns that can transform a personal financial plan.

1. Shockwave Medical

Shockwave Medical (NASDAQ: SWAV) is a medical device company that’s produced a novel treatment called Intravascular Lithotripsy (IVL) to modify calcium buildups in the cardiovascular system. IVL is adapted from an effective treatment for kidney stones involving rapid sonic pulses from a specialized catheter that can remove dangerous accumulations of calcium in blood vessels.

This approach is often favorable to more intrusive surgical interventions, and it also opens the door to treatment for patients who may not have been candidates for existing surgical procedures. Shockwave has developed an effective and promising set of products that should experience stronger demand as the senior population and prevalence of heart disease rise globally.

Shockwave has encouraging safety and efficacy data from clinical trials and a growing body of treated patients. Last year, the Centers for Medicare & Medicaid Services (CMS) created a new code for hospital reimbursement when procedures using Shockwave’s technology are used, which is a huge step for market acceptance and revenue generation. It’s still in the relatively early stages of gaining market traction and educating physicians on the system, which means there’s plenty of opportunity ahead.

The company reported 41% revenue growth in its most recent quarter,

topping analysts’ earnings forecasts by more than 30%. The company anticipates 25% growth for 2024. Such a deceleration is usually bad news for growth stocks, but Wall Street was actually forecasting slightly lower sales. Expectations were already at an attainable level, which is exactly what growth investors should want to see.

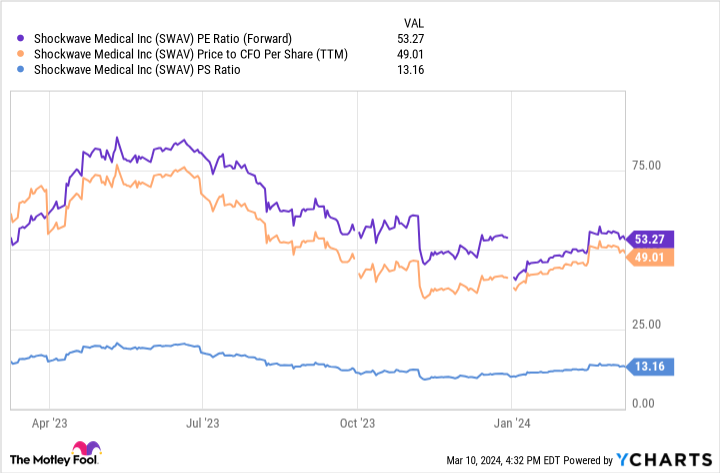

Shockwave stock looks fairly expensive, with a price-to-sales ratio over 13 and a forward price-to-earnings (P/E) ratio over 50. However, that 25% growth rate results in a PEG ratio of around 2, which means that its price fairly reflects the expected growth rate. If it doesn’t decelerate in 2024, then the stock could even be considered cheap relative to growth.

The shares have a high beta of 1.3, so be prepared for volatility in the short term. Still, high-beta stocks can outpace the market if they’re successful in the long term. This company’s market capitalization is just under $10 billion, meaning it’s on the cusp of breaking into large-cap territory. If these treatments become commonplace around the world, there’s a ton of room to the upside.

2. Workday

Workday (NASDAQ: WDAY) provides cloud-based software for organizations to manage financial functions and human capital. These AI-enhanced tools are useful for maintaining efficient operations, especially as distributed and global labor forces become more popular. Its product suite ultimately provides better visibility and insights for management while helping to keep employees happier and more productive. Workday’s platform gets high ratings from Gartner, which ranks it among the leaders in human capital management software.

Workday’s potential customers include non-profits, small and medium-sized businesses, and enterprises, so its addressable market is broad. Roughly half of the S&P 500 companies are Workday subscribers, which is encouraging. Wide adoption indicates strong significant demand and customer traction, but there are still a lot of untapped potential customers out there.

Analysts consider Workday a wide-moat stock, meaning that it has a sustainable competitive advantage. That’s driven by high switching costs and its high-quality offering of mission-critical products. Its high net dollar retention rate offers convincing statistical evidence of that moat.

Workday is forecasting 17% to 18% sales growth next year, roughly consistent with its most recent quarter. Subscriptions account for 92% of total sales, which makes cash flows highly predictable relative to other revenue models. That’s a helpful characteristic for a company that’s recently achieved profitability. Workday’s price-to-cash-flow ratio is only around 32. That’s an attractive valuation if it meets its growth targets.

At a $70 billion market value, Workday isn’t some under-the-radar company with explosive growth ahead. It’s an established company with good growth prospects and a reasonable valuation that could conceivably deliver five times your investment over the long term.

3. ServiceNow

ServiceNow (NYSE: NOW) broke onto the scene with workflow automation software for IT services, which is important for managing tech teams that are essential for every major business. The company has since expanded its offering to include tools supporting functions, including finance and customer service. ServiceNow is leaning heavily into the disruptive power of AI as its customers look to use these capabilities to usher in the next wave of tech transformation.

The company boasts strong marks from Gartner, placing it among industry leaders. Its leadership position is corroborated by excellent retention data — the company reports customer renewal rates that have consistently been 98% and higher, and it has consistently expanded customer relationships over time.

ServiceNow’s revenue grew 26% in the most recent quarter, and it expects sales to expand by just under 25% next year. It’s forecasting a roughly stable adjusted operating margin in 2024, so its cash flows should move more or less in proportion to the top line. The stock’s price-to-cash-flow ratio is about 45, and its forward P/E ratio is approaching 60. Those are both on the expensive side but reasonable when compared to the growth outlook.

There’s volatility risk inherent in stocks with this sort of valuation, but the company’s combination of competitive strength and growth potential make it a candidate to expand into one of tomorrow’s tech giants.

Should you invest $1,000 in Shockwave Medical right now?

Before you buy stock in Shockwave Medical, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Shockwave Medical wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

See the 10 stocks

*Stock Advisor returns as of March 11, 2024

Ryan Downie has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends ServiceNow, Shockwave Medical, and Workday. The Motley Fool has a disclosure policy.

3 Stocks That Could Create Lasting Generational Wealth was originally published by The Motley Fool

Credit: Source link