For investors looking at the artificial intelligence (AI) sector, 2024 is shaping up to be a landmark year. So it’s high time to set your portfolio up for the new year, and you don’t have to do it alone.

Three Motley Fool contributors put their heads together to present their best AI investments for the new year.

In the resulting discussion, you’ll find three standout AI stocks with market-beating prospects in 2024 and beyond. International Business Machines (NYSE: IBM) made a strategic pivot toward AI and cloud computing. Nvidia (NASDAQ: NVDA) is a trailblazer in specialized hardware and generative AI systems. ASML Holdings (NASDAQ: ASML) forms the backbone of AI chip manufacturing.

These companies not only represent the pinnacle of innovation in AI but also offer unique investment opportunities.

Don’t underestimate this AI pioneer’s ability to shine

Nicholas Rossolillo (Nvidia): It may sound like a “too-easy” pick, or even one that’s overhyped, but after Nvidia’s last earnings update, there could be plenty of room for the generative AI system pioneer to climb higher during the new year. How so?

During the third-quarter fiscal 2024 earnings call (for the period ended in October 2023), revenue soared 206% higher than the year prior to $18.1 billion, driven by the data center segment (where most of the generative AI chip and system sales are registered). Astoundingly, another sequential increase is expected in the fourth quarter with management predicting $20 billion in sales.

But here’s where things get interesting and where the debate comes in (as Anders, Billy, and I wrote about a couple of months ago): CEO Jensen Huang and the top team have been clear that they expect their data center sales (80% of total revenue last quarter) to continue rising in calendar year 2024 as more supply of its AI chips comes to market to meet insatiable demand. The market seems to have wrapped its head around this, with Wall Street analysts’ consensus for next year’s revenue pegged at nearly $91 billion, which implies a more than 50% increase.

But semiconductor sales tend to be cyclical. Periods of surging revenue are often followed by a slump. All eyes are now on what will happen in 2025. But for the record, on the last earnings call, Huang said he “absolutely believe[s] that data center can grow through 2025.”

The jury is, of course, still out on this. At some point, I expect the world to take a breather on building new AI computing infrastructure. Perhaps that will finally arrive in 2025, or maybe it will delay until 2026 or later.

But if Huang is correct, and that the roughly $1 trillion global AI data-center opportunity continues to expand unabated over the next couple of years, Nvidia looks like a reasonably valued semiconductor stock. Shares trade for 25 times next year’s (calendar year 2024) expected earnings per share. I have no plan on selling any of my position in Nvidia just yet as another busy year gets rolling.

It’s time to dive into Big Blue’s AI ocean

Anders Bylund (IBM): The IBM you see today is miles apart from the one-stop-IT-shop from the turn of the millennium. In a prescient yet painful strategy shift that started in 2012 and never really ended, Big Blue refocused its massive assets on the high-growth “strategic imperatives” of cloud computing, data security, analytics, and AI.

The watsonx.ai platform is a development platform custom-built for enterprise-scale businesses in search of machine learning and generative AI tools. It includes generative AI support in the app-writing experience and the option to generate apps in a drag-and-drop graphical interface rather than manual coding, and it relies on IBM’s many decades of AI research.

And the company isn’t resting on its digital laurels. The company has $11 billion of cash equivalents and generated $10.3 billion of free cash flow over the last four quarters. And those funds are aimed squarely at the AI opportunity right now.

For instance, IBM recently committed to training 2 million AI experts in the next three years, collaborating with universities around the world. It also started a $500 million investment fund focused on innovative AI start-ups.

As a result, IBM is poised to make up for its strategy-shifting pain with robust gains in the years to come. Trading at just 2.4 times trailing sales and 12.3 times free cash flow, IBM’s stock looks like a no-brainer buy today.

Yet, market makers seem to have forgotten about the giant shadow IBM casts over the AI opportunity. The stock has only gained 16% in 2023, falling behind the S&P 500 index’s 25% increase.

I don’t mean to throw market-beating performers like Nvidia under the bus, and I own that stock myself. However, the chip designer’s shares are changing hands at 27 times sales or 70 times free cash flow. If you’re looking for a strong AI investment at the threshold of 2024, IBM combines fantastic growth prospects and an unbeatable AI history with bargain-bin share prices.

This essential AI stock lagged peers this year but could soar in 2024

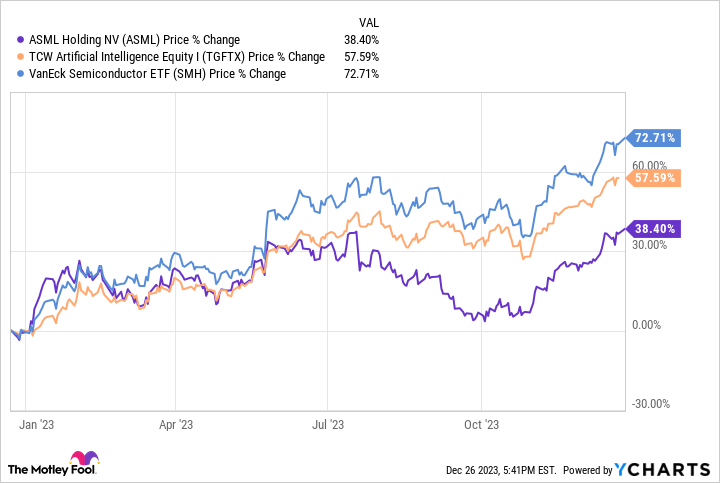

Billy Duberstein (ASML Holdings): A lot of artificial intelligence stocks have gone up a lot this year, so there aren’t that many bargains left. However, ASML Holdings, at least by comparison, underperformed a lot of AI stocks, rising “only” 38% despite its machines being essential to the AI chipmaking process. In addition, the stock remains about 15% below its all-time high set back in late 2021, whereas many other semiconductor and AI stocks are now above those prior highs.

ASML data by YCharts.

There are several reasons for this year’s underperformance. First, ASML is a European stock, so the relative performance of each market may have some effect. Second, ASML traded at a relatively higher valuation than other semiconductor-equipment companies coming into the year. So, there wasn’t as much ground to “make up” after the 2022 sector plunge. Even now, ASML trades at 35 times earnings.

In addition, ASML management already said the company won’t see much growth in 2024. This may be surprising, since most other semiconductor companies had a weak 2023 and now project a recovery year in 2024. However, ASML’s growth has been a little different. During the pandemic, ASML’s extreme ultraviolet (EUV) and deep ultraviolet (DUV) lithography machines were in such high demand and are so complicated and expensive to build that the production bottleneck stretched into this year. So, whereas many other semiconductor-equipment companies saw revenues decline in 2023, ASML will actually see 2023 revenue growth of about 30%. Only next year in 2024 will it endure the post-pandemic downturn effect.

However, as chip stocks tend to look ahead about a year, ASML could outperform some of its peers going into 2025. That’s a year management has predicted will be a big growth year, as several new leading-edge fabs come online using ASML’s latest EUV machines. In fact, ASML just shipped the first parts of its first high-numerical aperture (NA) EUV machine, the latest and most advanced model of EUV, to Intel. The high-NA machine is absolutely massive and will have to be shipped in 250 separate crates! Even though the first batch is being shipped now, production with them probably won’t happen until late 2025.

While ASML stock isn’t cheap, it has a monopoly on EUV technology needed to make chips below 7nm, which the industry just surpassed a couple of years ago. Last year’s leading-edge chips, such as the Nvidia H100, were manufactured on the 5nm node, and 2023 saw the production of the first 3nm chips.

But the first 2nm chips will be made in 2025, which is the node in which both Samsung and Intel hope to catch up to foundry leader Taiwan Semiconductor Manufacturing in leading-edge logic chips. That intense competition for the 2nm node means all of these companies will be buying lots of ASML’s machines to make those dreams a reality.

And the story doesn’t end there, as all major dynamic random access memory (DRAM) manufacturers will also begin using EUV to make DRAM chips going forward. While Samsung began using EUV two years ago, 2025 will also see Micron begin to use EUV for the first time in its memory production as the last memory holdout to use the complex process.

Generative AI will depend heavily on leading-edge processors and high-bandwidth memory, so look for ASML to perhaps outperform its peers in 2024 after lagging in 2023.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

See the 10 stocks

*Stock Advisor returns as of December 18, 2023

Anders Bylund has positions in Intel, International Business Machines, Micron Technology, and Nvidia. Billy Duberstein has positions in ASML, Micron Technology, and Taiwan Semiconductor Manufacturing. Nicholas Rossolillo has positions in ASML, Micron Technology, and Nvidia. The Motley Fool has positions in and recommends ASML, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and International Business Machines and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, and short February 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

3 Great AI Stocks to Own in 2024 was originally published by The Motley Fool

Credit: Source link