Student loan borrowers disproportionately experience different forms of material hardship relative to their nonborrower peers. Studies show that households with student debt have lower net worth and are more likely than their counterparts without student debt to be late on bill payments, be denied credit, experience bankruptcy, and have other financial difficulties.1 Because most borrowers take out student loans early in life, this debt uniquely affects borrowers’ abilities to build wealth and advance economically relative to other forms of debt.2

Two nationally representative longitudinal studies—Beginning Postsecondary Students (BPS) 2012/2017 and Baccalaureate and Beyond (B&B) 2008/2018, both conducted by the National Center for Education Statistics (NCES)—provide insight into the nature of the hardship that student borrowers experience, as well as trends in borrowing and repayment that help contextualize these experiences.3 The data show how incidences of hardship vary by student loan debt-to-income ratio, allowing the Center for American Progress to consider the effectiveness of using this ratio to inform federal debt relief policies. The findings detailed in this issue brief show that student loan borrowers experience financial hardship that prevents them from meeting basic living expenses, saving for emergencies, building retirement funds, buying homes, and forming families.

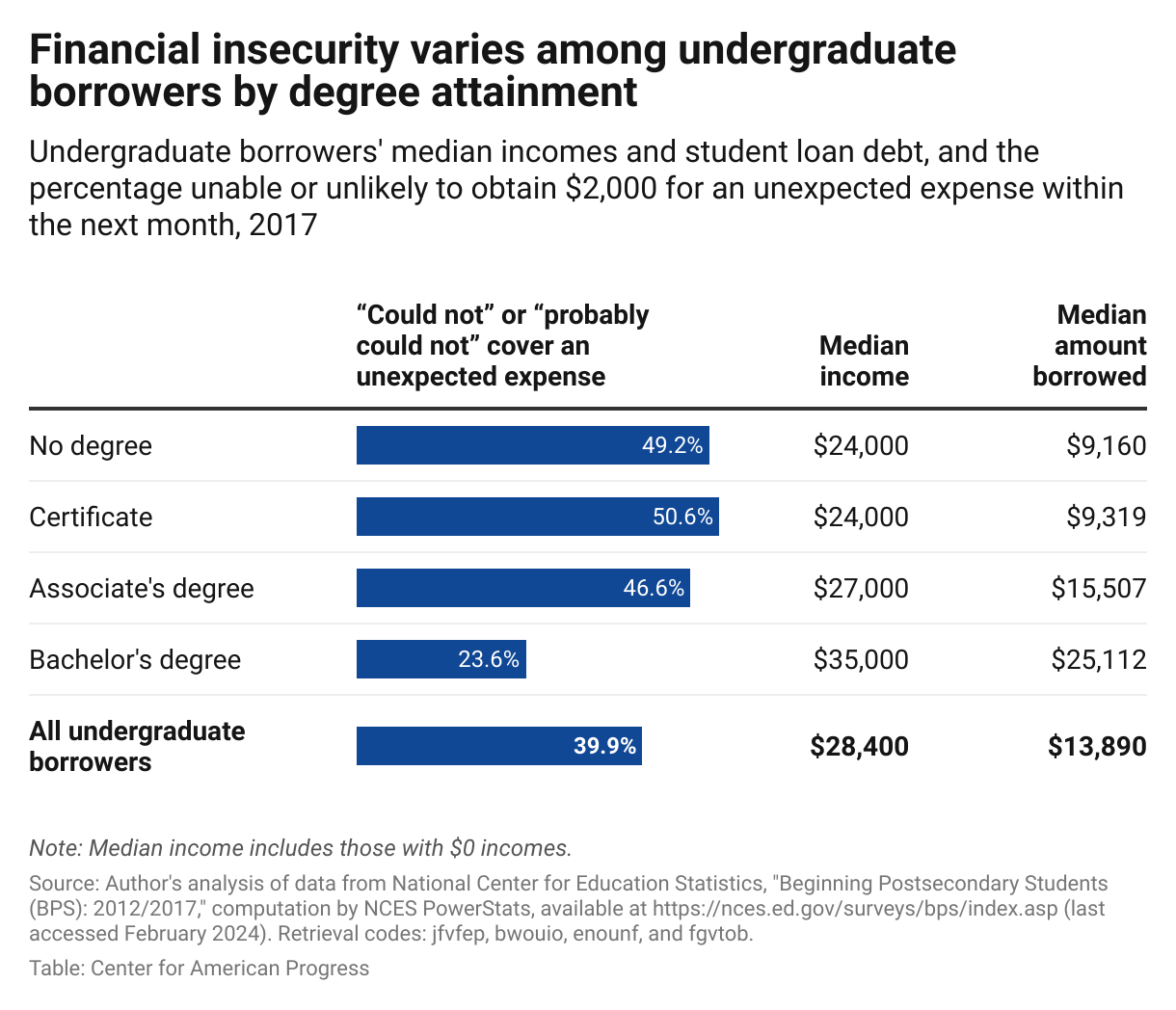

1. 6 years after beginning postsecondary education, borrowers who hold certificates and associate degrees, as well as those who did not complete their degree, experience financial hardship at about twice the rate of borrowers who hold bachelor’s degrees

Data from the 2012–2017 Beginning Postsecondary Students Longitudinal Study indicate that the proportion of undergraduate borrowers who experienced financial insecurity six years after beginning postsecondary education varied widely by degree level. In this case, financial security was measured by the inability to obtain $2,000 in the next month for an unexpected expense.4 (see Table 1)

TABLE 1

By this metric, about half of student loan borrowers with certificates and associate degrees, as well as those who did not complete their degrees, experienced this form of financial hardship, while about one-quarter of those with bachelor’s degrees did. By comparison, in the same year, about 67 percent of the general U.S. population anticipated being able to come up with $2,000 in a month to meet an unexpected expense.5

These results suggest that relief proposals should seek to deliver additional benefits or a higher level of relief to those who did not complete a degree, those who earned a certificate, or those with an associate degree relative to those with bachelor’s degrees.

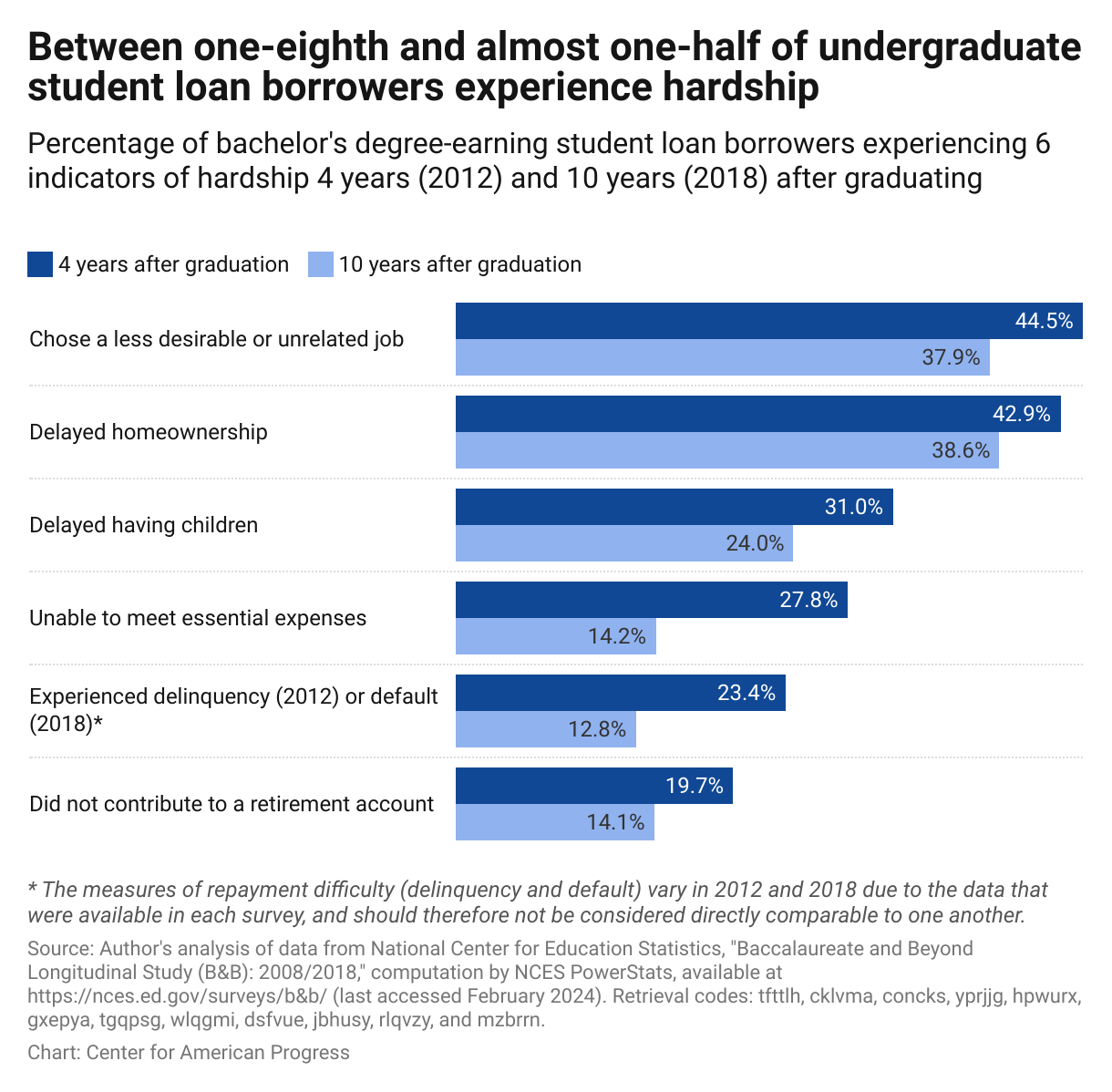

2. Undergraduate borrowers struggle early in their repayment life cycles, and default is an inadequate indicator of hardship

When undergraduate loan borrowers were asked in the 2008–2018 Baccalaureate and Beyond Longitudinal Study about various forms of financial hardship that could be attributed to their student debt, the share reporting hardship ranged from 19.7 percent to 44.5 percent, depending on the measure, four years after graduation. Six years later, these proportions decreased by between about 4 and 14 percentage points.6 (see Figure 1)

This underlines the urgency of delivering relief to student loan borrowers early in their repayment history, when most borrowers’ incomes are lowest and many struggle the most.

FIGURE 1

These results also suggest that default and delinquency, commonly used to indicate repayment difficulty, may underestimate the scope of the hardship that student loan borrowers experience. The proportions of borrowers in the 2008–2018 B&B survey who reported delaying homeownership (38.6 percent), delaying having children (24 percent), or choosing a less desirable job as “a result of [their] financial costs for undergraduate and graduate education” (37.9 percent) were between two and three times higher than those who defaulted in 2018 (12.8 percent).7

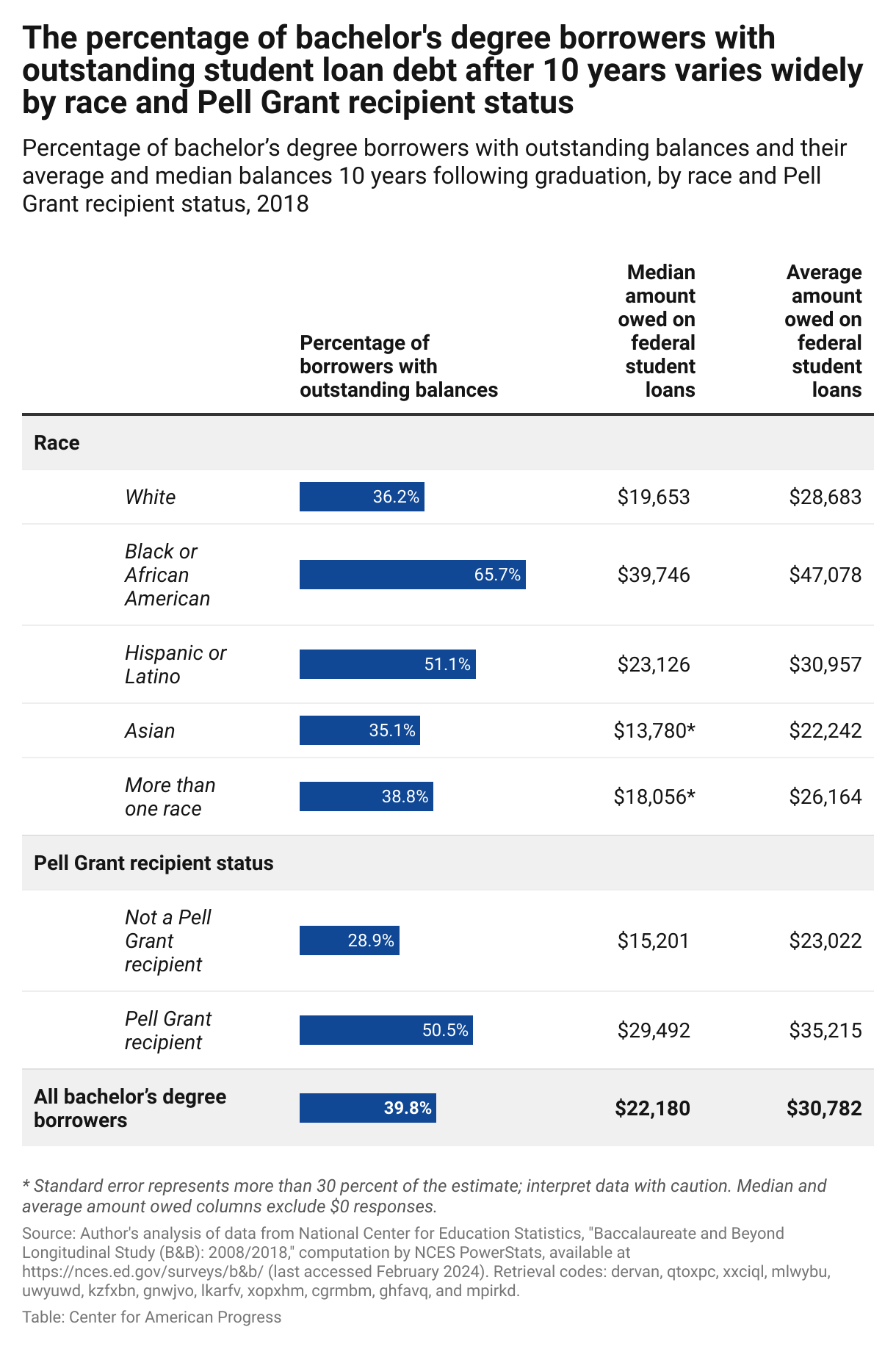

3. 10 years after graduation, 40 percent of bachelor’s degree earners still have outstanding debt, and outcomes are vastly unequal

Among the 40 percent of bachelor’s degree earners who had outstanding debt 10 years after graduation—the length of the standard repayment plan—the average remaining debt was $30,782.8 (see Table 2) And while about one-third of white borrowers had a remaining balance, about two-thirds of Black borrowers did.

TABLE 2

The data above illustrate that Black borrowers, Hispanic or Latino borrowers, and Pell Grant recipients tend to have the highest remaining balances after 10 years. The median outstanding debt for Black bachelor’s degree borrowers is more than double that of white borrowers, and the median debt for Pell Grant recipients is about twice that of non-Pell Grant recipients. These disparities point to the need to develop targeted solutions to help those who most struggle to repay their loans, as well as to the use of Pell Grant recipient status as an indicator of a higher likelihood of struggling with repayment.

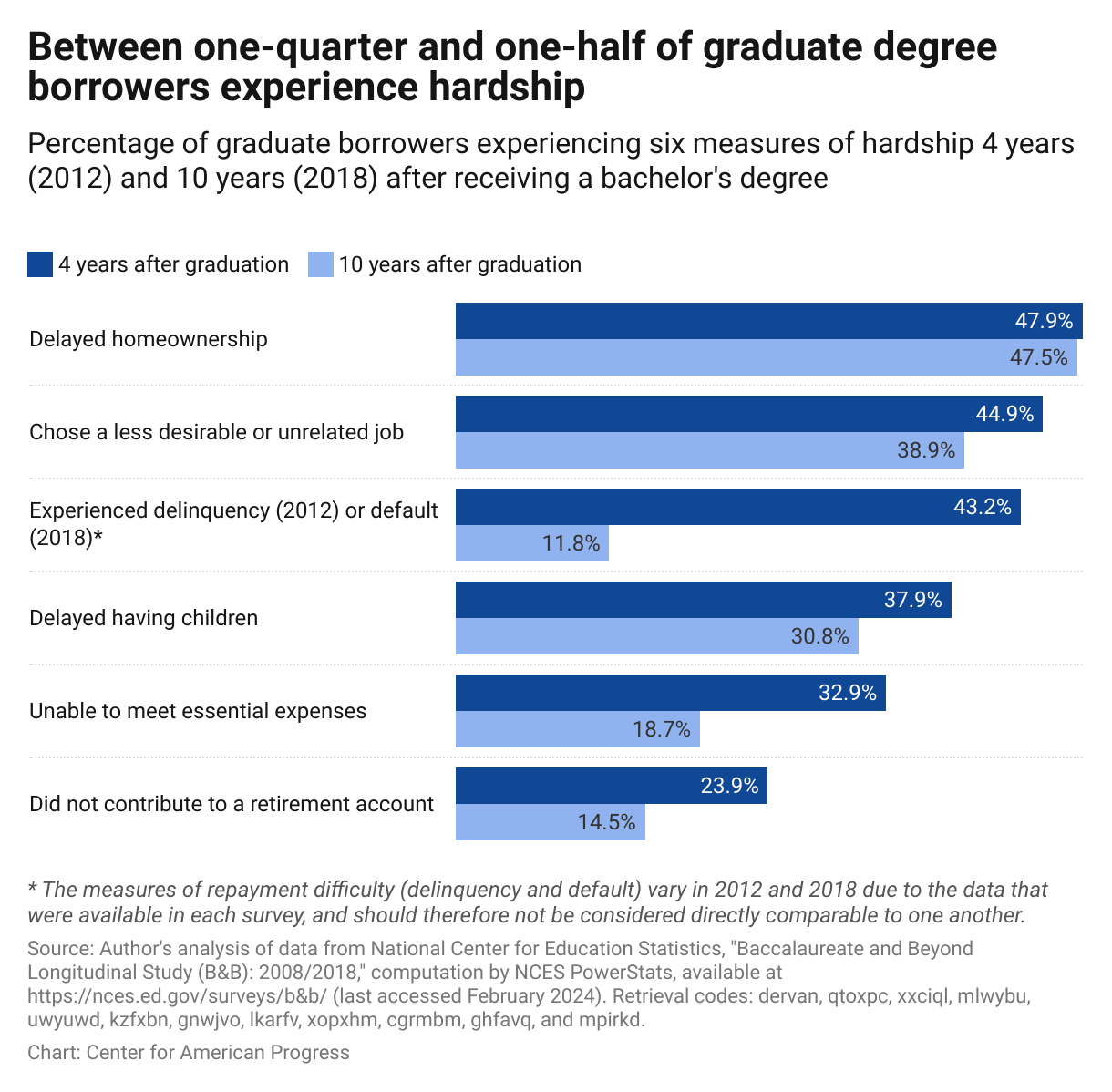

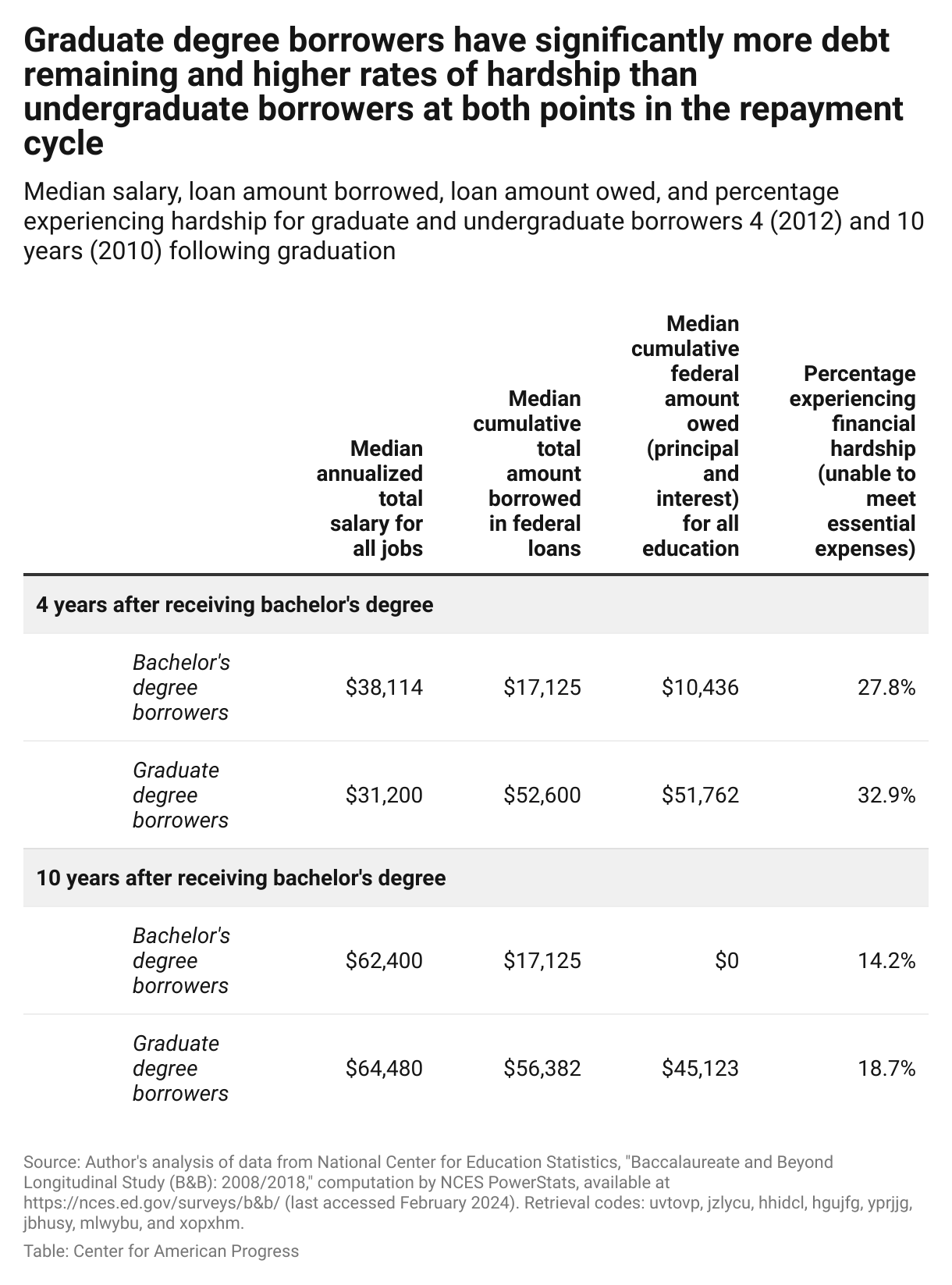

4. Higher incomes do not fully mitigate the impact of higher debt burdens on those who borrow for graduate degrees

At both points in the repayment cycle included in the B&B survey—4 and 10 years following bachelor’s degree receipt—graduate degree borrowers have higher levels of hardship, on average, than undergraduate-only borrowers on every measure except one (default 10 years after graduation). (see Figure 2)

FIGURE 2

This may be surprising to one who expects the earnings gains from graduate education to outweigh increased debt. For many borrowers—particularly those in the cohort that the B&B survey covers, who were affected by the Great Recession and rising graduate school borrowing—it appears that the higher incomes associated with graduate degrees did not, in the aggregate, outweigh the increased debt burden of graduate borrowing.9 Graduate borrowers have debt burdens more than three times higher than those of undergraduate borrowers, both 4 and 10 years after graduation, despite having similar median salaries. (see Table 3)

TABLE 3

While undergraduate borrowers made progress paying down their debts from a median of about $17,000 at graduation to a remaining balance of $10,400 four years later and close to $0 10 years later, the typical graduate borrower has paid down about 20 percent of their total debt 10 years after earning their bachelor’s degree (with about $45,000 of $56,000 remaining). This may help explain why, both 4 and 10 years after graduation, graduate borrowers have average rates of hardship—measured here as being unable to meet essential expenses at least once in the previous 12 months—that exceed those of undergraduate borrowers.

The remainder of this brief uses the inability to meet essential expenses hardship indicator to convey borrowers’ ability to meet their basic needs. It should be understood as a measure of relatively extreme hardship that suggests a floor, rather than a ceiling, at which debt relief proposals meant to address hardship should begin.

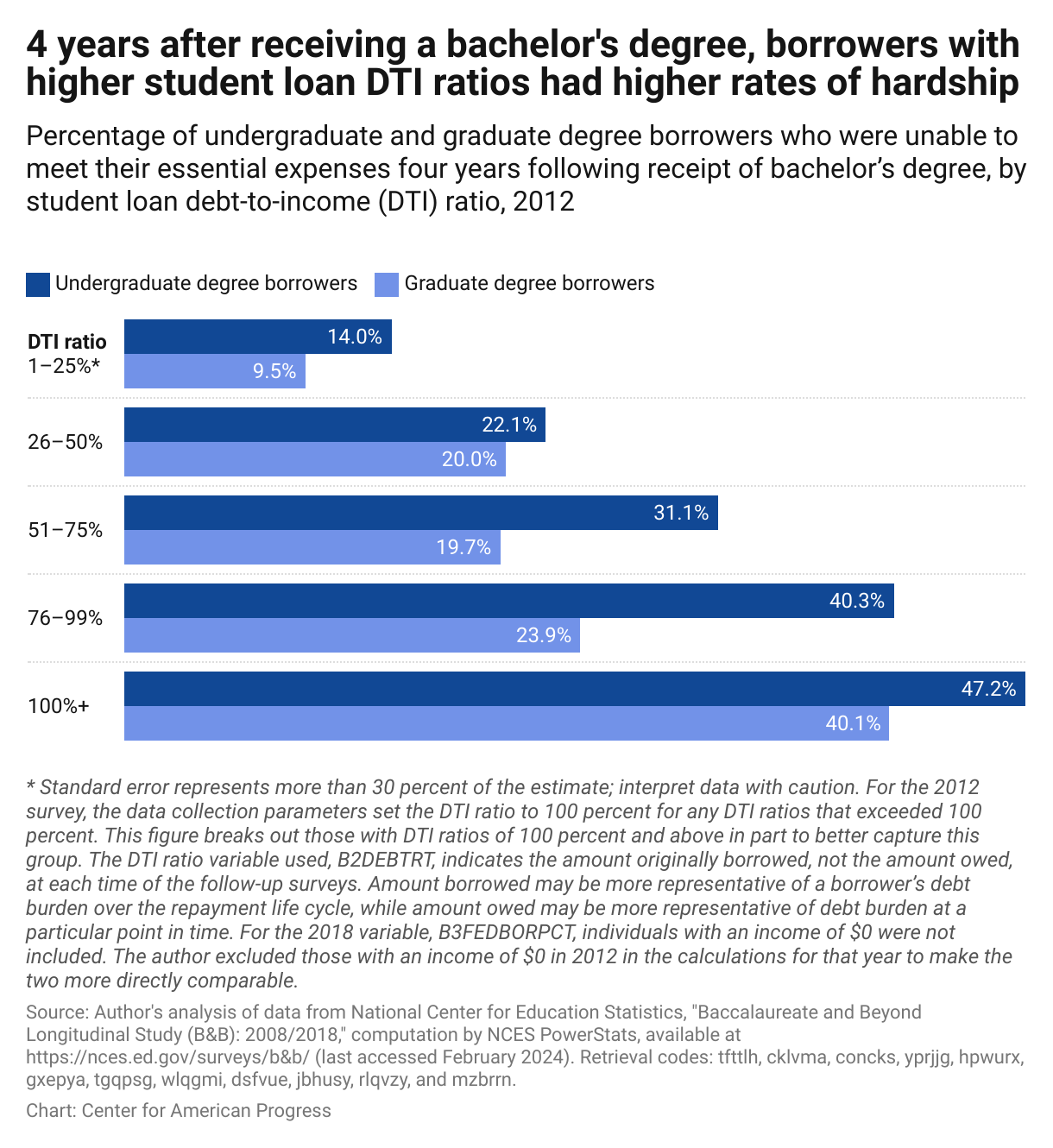

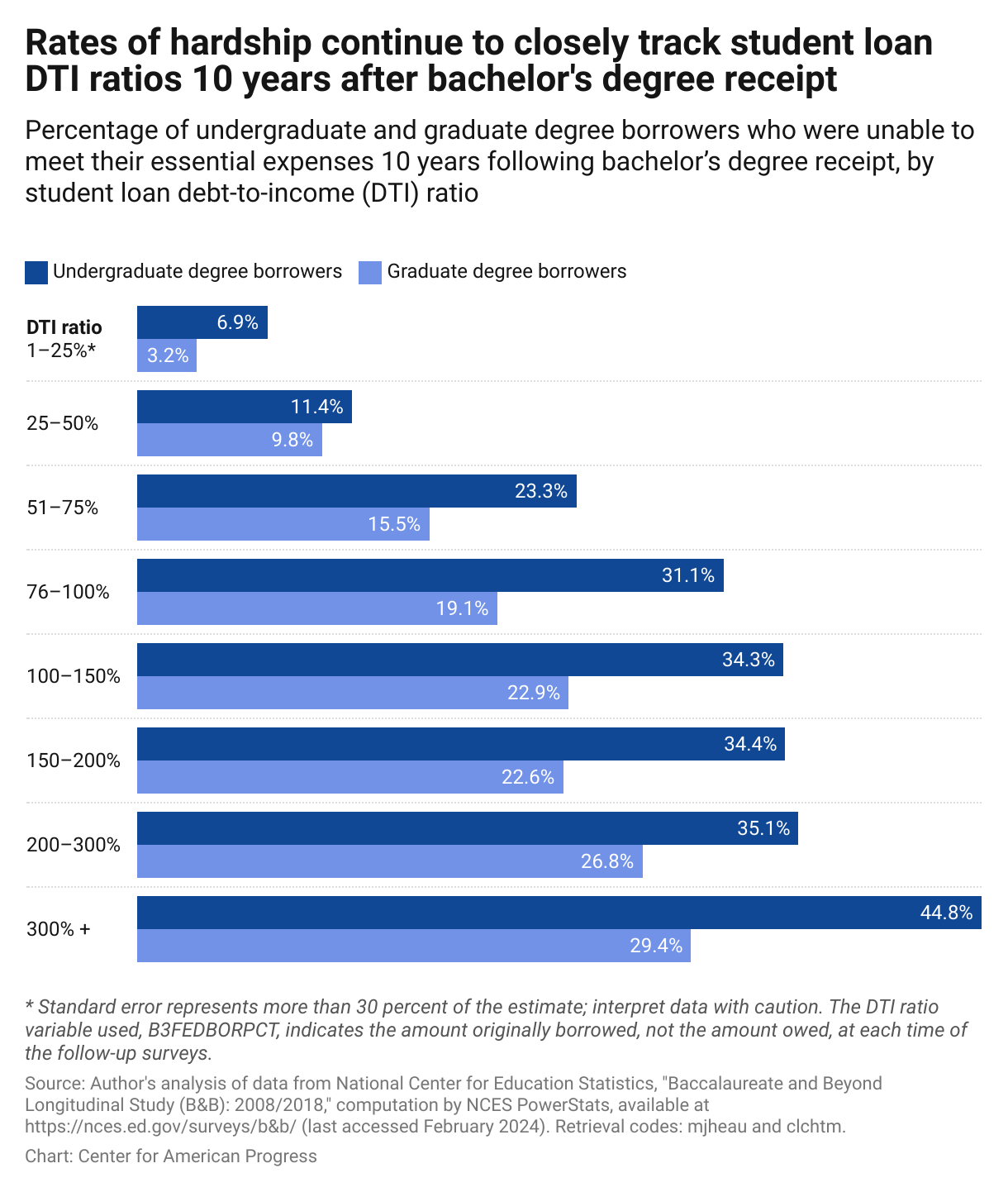

5. Undergraduate borrowers experience hardship at student loan debt-to-income ratios lower than those of graduate borrowers

Although graduate borrowers tend to have higher levels of debt and higher rates of hardship on average, undergraduate borrowers struggle more within the same student loan debt-to-income ranges. For example, four years after graduation, undergraduate borrowers with debt-to-income ratios ranging from 76 percent to 99 percent were 16 percentage points more likely to experience hardship than were graduate borrowers in the same debt-to-income range. Six years later, in 2018, undergraduate borrowers’ rates of hardship still far outstripped those of graduate borrowers in each range, with a gap ranging from 2 percentage points to 15 percentage points.

FIGURE 3

FIGURE 4

These data suggest that different debt-to-income ratio thresholds would be appropriate for graduate and undergraduate borrowers, as graduate borrowers seem able to sustain higher ratios than undergraduate borrowers. Yet while federal financial aid policy treats undergraduate and graduate education fundamentally differently, the distinction may be more fluid for borrowers due to gender and racial wage gaps. Certain demographic groups need to attain more education to reach the same level of income: For example, white men with a bachelor’s degree out-earn white, Black, and Latinx women with a graduate degree.10 Reducing distinctions between graduate and undergraduate borrowers for the purposes of debt relief, where possible, therefore may be a more equitable approach.

6. Borrowers with similar debt-to-income ratios who are enrolled in IDR plans face more hardship than those enrolled in standard repayment plans

While income-driven repayment (IDR) plans are undoubtedly an invaluable tool to help borrowers struggling with high monthly payments, the data considered in this brief suggest they do not entirely ameliorate hardship. Ten years after receiving bachelor’s degrees, undergraduate and graduate borrowers with similar debt-to-income ratios who are enrolled in IDR plans experience higher levels of hardship (as measured by the inability to meet essential expenses at least once in the past 12 months) than their peers who are enrolled in other plans:

- IDR-enrolled undergraduates who have a debt-to-income ratio of more than 50 percent face rates of hardship that are about 10 percentage points higher than those of their counterparts who are in other types of repayment plans—37.6 percent vs. 27.2 percent, respectively.11

- Graduates who are enrolled in IDR plans and have debt-to-income ratios from 50 percent to 100 percent also have rates of hardship that are about 10 percentage points higher than their counterparts in other types of plans—24.7 percent vs. 14.1 percent, respectively—and graduate borrowers with debt-to-income ratios of more than 100 percent face a gap of 5 percentage points (25.5 percent vs. 20.3 percent).12

Because IDR plans offer lower monthly payments over a longer timeline, borrowers who struggle to make standard plan payments as a result of financial hardship are likely to opt into them.

Policy recommendation

Using debt-to-income ratios to target relief may have advantages relative to debt or income alone, as they capture two different dimensions that reflect and affect a borrower’s circumstances. On one hand, debt tends to increase as family income and wealth decrease; borrowers from lower-income families generally borrow more, making student debt a fundamentally regressive education financing tool.13 Second, income is shaped by racial and gender wage gaps, meaning that it reflects systemic inequalities.14

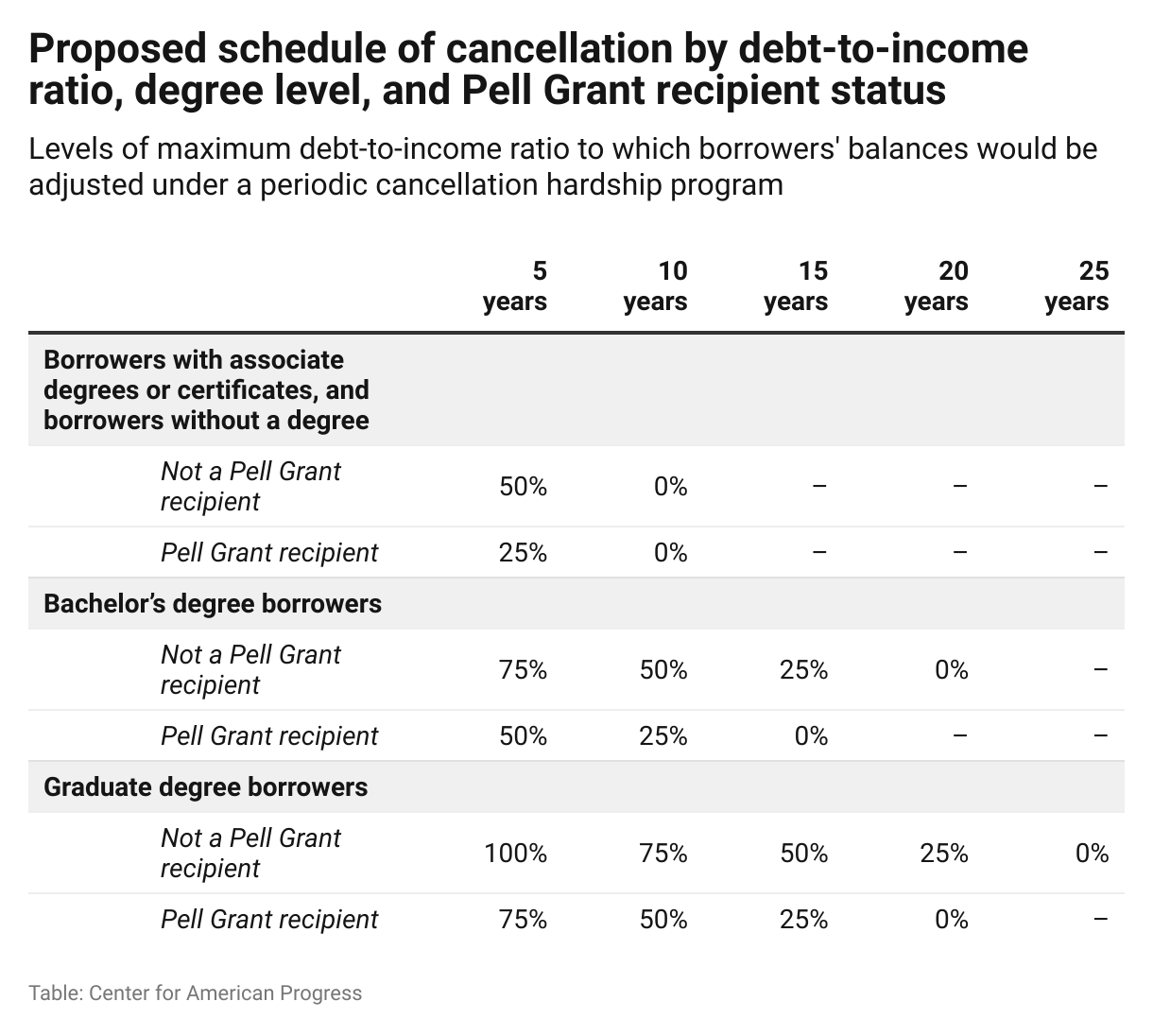

Offering periodic balance adjustments for borrowers who have persistently high debt-to-income ratios in order to bring their balances down to more affordable levels would likely help lower incidences of financial hardship among borrowers. Unlike a one-time cancellation of remaining balances after 20 or 25 years of repayment, which IDR plans promise, balance adjustments would deliver cancellation incrementally and adjust borrowers’ balances to levels that they can more reasonably afford to pay.15

TABLE 4

The U.S. Department of Education could consider using two- or three-year averages of income when adjusting balances in order to reduce the likelihood that borrowers intentionally lower their incomes in advance of an adjustment and to exclude periods of forbearance and/or deferments, especially in-school deferments.

A 2015 study estimated that a 10 percent to 15 percent monthly payment corresponds roughly with “the rule of thumb that total student loan debt at graduation should be less than the borrower’s expected annual starting salary,” which would correspond to a 100 percent debt-to-income ratio upon graduation.16 The Texas Higher Education Coordinating Board, in its strategic state plan for higher education, calls for all students to graduate with “debt that amount[s] to less than 60% of first-year wages.”17 These two thresholds for overall debt-to-income ratio upon graduation—from less than 60 percent to 100 percent of original principal to first-year salary—may be understood as general benchmarks at which the department could begin to assess reasonable debt-to-income ratios that could inform debt relief policies.

Conclusion

Experiences of material hardship are multifaceted and overlapping, and student loan debt is undoubtedly not the only factor creating hardship in borrowers’ lives. Looking at broad patterns in how borrowers with similar characteristics experience hardship relative to one another, however, can still provide policymakers information on how best to deliver debt relief to those who struggle the most. While no single factor can explain borrowers’ debt levels, incomes, and rates of hardship, these metrics nonetheless reflect the socioeconomic conditions that borrowers experience.

Furthermore, the financial resources that borrowers put toward student loan payments equate to forgone retirement contributions, savings for down payments, investments, or other wealth-building purposes. Funds that may otherwise have delivered a positive return for borrowers over the course of their adulthoods are instead used to service debts acquired early in life.

Proposed regulations to deliver debt relief to targeted groups of borrowers, as well as the actions underway to deliver relief, will have an immense impact on the borrowers who have been most poorly served by the federal financial aid system.18

Credit: Source link