Since the turn of the century, Nike (NYSE: NKE) and Pool Corporation (NASDAQ: POOL) have delivered market-trouncing total returns of 1,560% and 7,790%, respectively. However, these traditionally robust businesses have seen their share prices decline 47% and 59% over the last few years. Facing an array of shorter-term macroeconomic issues, such as softer consumer spending, persistent inflation, and higher interest rates, these stocks have seen the market dismiss their longer-term potential.

Although both companies face very real challenges, these look to be temporary — and the shares are now available at once-in-a-decade valuations. Here is why this short-term volatility could prove to be a magnificent opportunity for patient investors who think in decades, not quarters.

1. Nike

There’s no running from it — owning shares of Nike has been a rough ride over the last few years. With its share price down 59% from its all-time highs, Nike is currently experiencing the third-largest drawdown in its history.

Only growing sales by 1% in 2024 and guiding for a mid-single-digit revenue decline for 2025, the company was unable to assuage the market’s fears, leading to a new 15% drop in a single day in June.

So what exactly makes Nike a once-in-a-decade opportunity today and throughout the second half of 2024? First, from a financial standpoint, the company’s inventory and days inventory outstanding continue to inch lower toward historical norms.

While this alone doesn’t mean a turnaround is immediately forthcoming, normal inventory levels help free up Nike to get back to its innovative roots and create the next generation of popular apparel for its devoted customers.

My second point focuses on these devoted customers. Despite the short-term challenges faced by Nike, it remains far and away the most powerful brand in the apparel industry. Ranked 21st on Kantar BrandZ’s list of The Top 100 Most Valuable Global Brands, Nike continues to hold immense mindshare among consumers. Companies included on Kantar’s list have outperformed the S&P 500 since 2003, delivering total returns of 321% versus the index’s 231%.

Furthermore, a recent study by Piper Sandler of top brands according to Gen Z shoppers shows that Nike dominates both the clothing and footwear categories, with 34% and 59% of consumers naming Nike the top brand in each niche. In both categories, the second- through fifth-highest brands combined to account for less than half of Nike’s share.

So, while Nike’s ongoing turnaround may need time to develop, this young group of shoppers highlights that the company’s future remains incredibly bright. Trading with a price-to-earnings (P/E) ratio of 20 that is at 10-year lows and a 1.9% dividend that is its highest since the Great Recession, Nike could be a contrarian pick for long-term investors right now.

That said, things could continue to get worse before they get better for Nike, so dollar-cost averaging (DCA) purchases make more sense than going all-in at today’s price.

2. Poolcorp

Pool Corporation — better known as Poolcorp — is the largest U.S. distributor of pool supplies. Its shares have declined 47% since 2022 as consumers continue to rein in spending. With the Expectations Index — a component of the Consumer Confidence Index — recording its fifth-straight quarter of a score below 80, this slowdown in consumer spending can clearly be seen.

Typically, a score below 100 shows that consumers are pessimistic about the future economy, causing them to be more cautious with their spending, especially on big-ticket items like new or refurbished pools. Hindered by this pessimism, paired with homebuyers battling persistent inflation and higher interest rates, Poolcorp felt the impact.

In the company’s most recent quarter, sales and earnings per share (EPS) declined by 7% and 21%, respectively, as new home and pool builds remained depressed. However, compared to the severity of an Experience Index of only 73 — a score typically reserved for recessionary times — these results are far from disastrous.

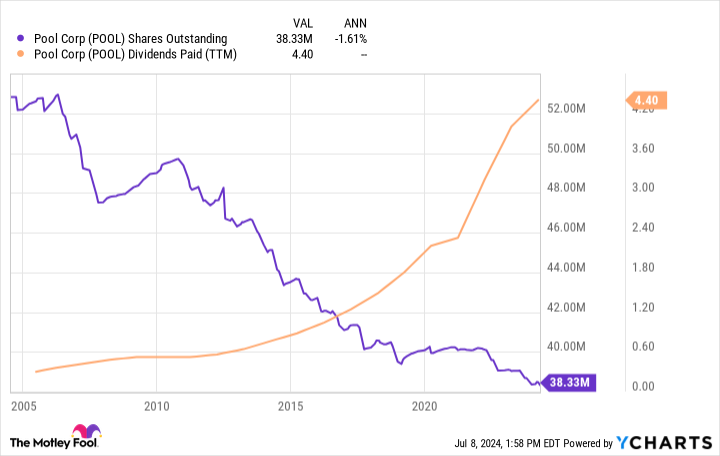

Generating 86% of its sales from non-discretionary, recurring items like maintenance (such as pool chemicals), Poolcorp demonstrates resilience in challenging times, as evidenced by the company’s continuous profitability throughout the 2008 recession. Further highlighting this resilience, Pool has a long track record of steadily lowering its share count while growing its dividend for 13 straight years despite being tied to the cyclical housing industry.

As the company continues to expand into higher-margin opportunities, such as its franchised Pinch-a-Penny retail stores and private-label pool chemicals, these cash returns to shareholders should continue growing. Best yet for investors, Pool may be trading at a once-in-a-decade valuation.

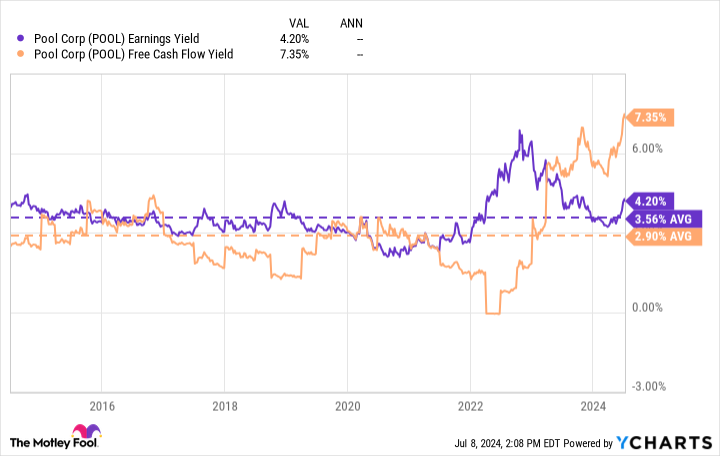

Whether using the company’s earnings yield or free-cash-flow (FCF) yield (which are the inverse of the price-to-earnings ratio and price-to-FCF ratios, so higher is “cheaper”), Poolcorp trades at a deep discount to its 10-year averages.

The cherry on top for investors? Poolcorp’s 1.5% dividend yield is the highest it has been since 2014, and it still only accounts for roughly one-third of the company’s total net income.

However, much like Nike, prospective Poolcorp investors may want to use DCA purchases on the company as it waits for a broader turnaround in consumer and homebuying confidence.

Should you invest $1,000 in Nike right now?

Before you buy stock in Nike, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nike wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $826,672!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of July 8, 2024

Josh Kohn-Lindquist has positions in Nike and Pool. The Motley Fool has positions in and recommends Nike. The Motley Fool recommends the following options: long January 2025 $47.50 calls on Nike. The Motley Fool has a disclosure policy.

A Once-in-a-Decade Opportunity: 2 Magnificent S&P 500 Dividend Stocks Down 47% and 59% to Buy in the Second Half of 2024 was originally published by The Motley Fool

Credit: Source link