Typically, value hunting among stocks that have plummeted more than 70% at any given point in their history can be dangerous. History suggests that winning stocks keep winning and that investors would be better off “watering their flowers and digging up their weeds.”

However, there are exceptions to this notion.

Take Paycom (NYSE: PAYC) and its human capital management (HCM) software-as-a-service (SaaS) solutions, for example. The stock is currently 70% off its high. In 2019, the upstart company had sales of roughly $600 million and a share price of around $170. Today, the company’s share price is the same, yet revenue has basically tripled.

This occurrence, paired with Paycom’s resilient free cash flow generation, leaves the company now trading at what could prove to be a once-in-a-decade valuation. While the market remains uncertain about the company’s growth story, here’s the case for buying and holding Paycom forever.

Why Paycom’s current growth slowdown isn’t a doomsday scenario

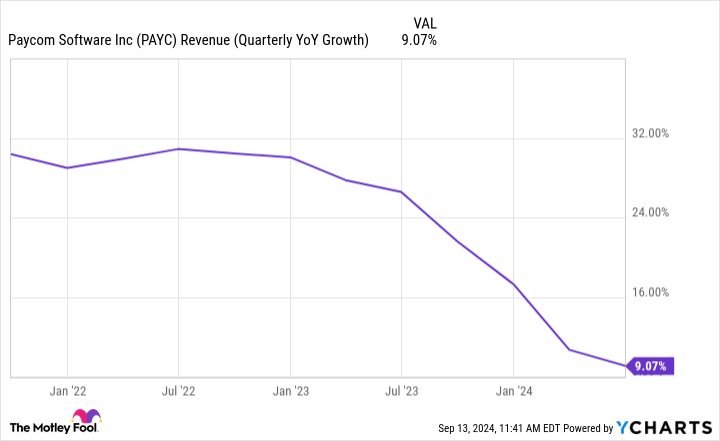

The primary reason for Paycom’s declining share price comes from its decelerating sales growth rate.

While a slowdown like this is concerning, management has argued that a decent portion of this drop stems from the introduction of its Beti payroll processing platform in late 2021. By empowering employees to manage their own payroll, Beti identifies and fixes many common errors prior to a company processing its payments, reducing the number of payroll reruns needed.

Obviously, this is fantastic for Paycom’s customers, with one client stating that it was able to cut its payroll department by half thanks to Beti’s time-saving value. However, prior to Beti, Paycom generated sales from rerunning payrolls for its customers any time there were errors. In short, the company’s successful new product is cannibalizing an existing base of sales, slowing growth.

Ultimately, investors who think in decades, not quarters, should welcome this trade-off between cannibalizing existing sales and giving customers the best products while keeping them as happy as possible. Thanks to this focus on customer satisfaction, Paycom’s Net Promoter Score (NPS) of 67 easily beats those of its payroll processing peers Paychex, Workday, and ADP, which have respective scores of -14, 31, and -10. A company’s NPS uses a -100 to 100 scale, with a score above 0 showing that more customers would recommend a product to their friends than wouldn’t. This means Paycom’s products are beloved.

Best yet for investors, there were a couple of signs in the company’s second-quarter earnings call signaling that this slowing sales growth could be coming to an end. Founder and CEO Chad Richison said that the company sold 24% more units in Q2 year over year, which is more promising than Paycom’s 9% sales growth in the quarter may indicate. In addition to these promising figures, Richison announced that “July starts are up 40% from a revenue perspective,” showing that higher sales growth could be incoming in the third quarter.

Furthermore, with Beti recently launching in Canada, Mexico, the U.K., and Ireland, Paycom could see further growth ahead as it expands to clients with global operations.

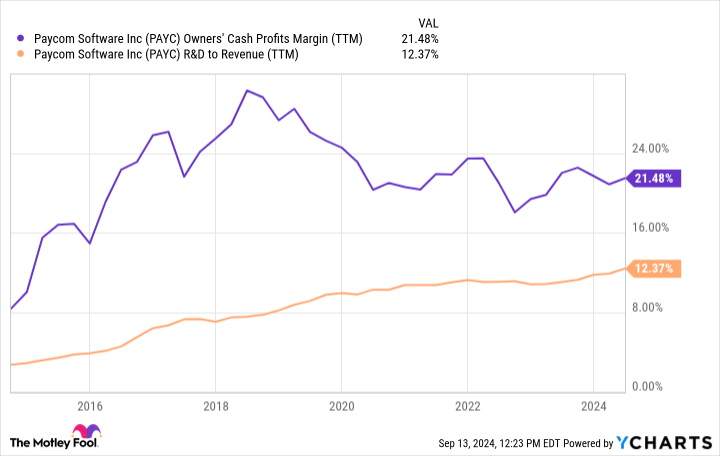

Growing cash generation despite increasing R&D spending

My favorite thing about Paycom is that it remains laser-focused on innovating and keeping its customers as happy as possible. By increasing its spending on research and development (R&D) over time, the company continues to ramp up the automation capabilities across its product suite. Despite this increased R&D spend, Paycom’s free cash flow (FCF) generation has proven to be incredibly resilient.

By delivering automated offerings like GONE, the company’s new time-off requests tool, Paycom has consistently proven that its new offerings generate enough value to offset the cost of the R&D needed to create them. Touching on the value that GONE brings to its clients, the company explained: “Each manual time-off review or approval can cost a company an average of $30.92, according to a November 2023 Ernst & Young study commissioned by Paycom.”

Maintaining its status as a genuine cash cow while increasing spending on R&D makes Paycom a strong candidate to become a top-tier compounder over the long haul.

Paycom’s potential once-in-a-decade valuation

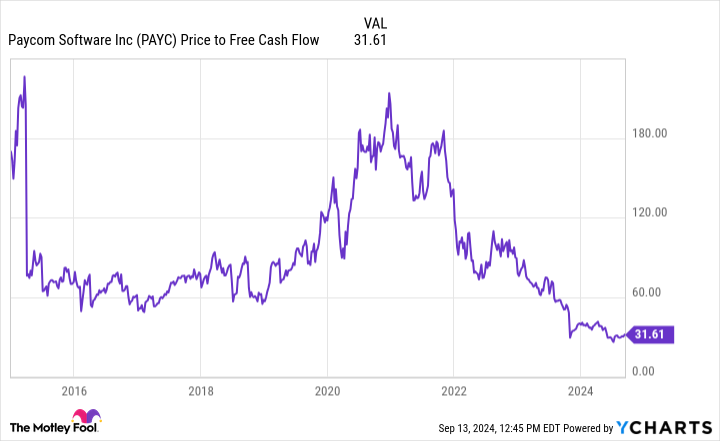

As promising as Paycom’s growth prospects and automated products look, the company continues to trade at a once-in-a-decade low price-to-FCF ratio.

Anchored by a balance sheet that’s home to $346 million in cash and $0 in long-term debt, management has begun buying back shares at these lower prices and now has a $1.5 billion share buyback plan authorized. Compared to the company’s market cap of $9.7 billion, this buyback authorization could go a long way toward helping Paycom’s share price turn around.

Last but not least, Paycom pays a 0.9% dividend, but it has yet to raise it after starting it six quarters ago. While a dividend increase would be nice for investors, management may be more focused on buying back shares at today’s prices.

Ultimately, I think Paycom’s sales growth could be poised to turn around over the next couple of years. This rebound, paired with Paycom’s history of profitably innovating its products, leaves me more than happy to pick up shares at this once-in-a-decade valuation and hold them for the long term.

Should you invest $1,000 in Paycom Software right now?

Before you buy stock in Paycom Software, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Paycom Software wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $729,857!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of September 9, 2024

Josh Kohn-Lindquist has positions in Paycom Software. The Motley Fool has positions in and recommends Paycom Software and Workday. The Motley Fool has a disclosure policy.

A Once-in-a-Decade Opportunity: 1 Super Growth Stock Down 70% to Buy and Hold Forever was originally published by The Motley Fool

Credit: Source link